Product-led growth is not a marketing tactic bolted onto a free trial. It is a different unit economics model, and treating it like a top-of-funnel decision instead of an FP&A decision is why so many "PLG" companies burn cash without knowing why.

The decision this article helps you make: whether your product can carry acquisition on its own, what that does to your CAC payback and headcount plan, and where the model breaks if you don't add a sales layer at the right revenue point. You'll leave with the calculation, the benchmark ranges by GTM motion, and the specific traps that show up in board decks when PLG is reported as a growth story instead of an economics model.

Key takeaways

- Product-led growth (PLG) is a go-to-market motion where the product itself, not a sales rep, drives acquisition, activation, and expansion. The economics are what make it work or fail, not the self-serve signup flow.

- PLG motions post median CAC payback of roughly 6-12 months versus 15-24+ months for sales-led motion, but that speed comes with materially higher logo churn that a single blended metric will hide.

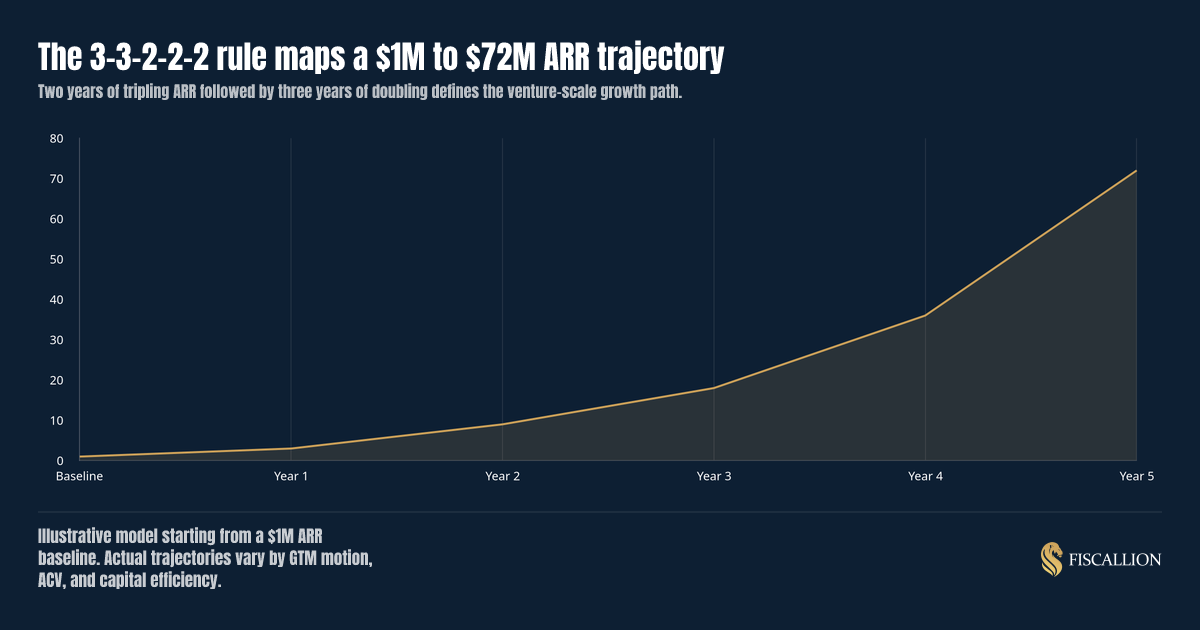

- The 3-3-2-2-2 rule (triple ARR two years, then double it three years) is the venture-scale trajectory investors benchmark against. PLG changes how you hit it, not whether the target applies to you.

- PLG vs SLG is not a permanent choice. Most durable SaaS companies at $5M-$50M ARR run a hybrid: self-serve at the bottom of the market, sales-assisted above an ACV threshold you should define explicitly, not by instinct.

- PLG is not a trend to grow out of. It is a permanent category of go-to-market motion, but it demands its own forecasting model, its own churn cohort view, and its own headcount trigger points.

What we'll cover

- What product-led growth actually means as a financial model, not a marketing label

- How to calculate the metrics that determine whether your PLG motion is working

- How to interpret PLG benchmarks without fooling yourself

- What to do next: the decisions PLG forces onto your operating plan

- Common mistakes and the replacement moves

- A practical framework you can put in front of your board

- FAQs: the 3-3-2-2-2 rule, PLG examples, PLG vs SLG, and whether PLG is just a trend

What product-led growth actually means for your model

Product-led growth is a go-to-market motion in which the product, not a salesperson, is the primary driver of acquisition, activation, conversion, and expansion. The term was coined by OpenView in 2016. Users sign up, get value inside the product, and upgrade because the product itself creates the moment of need.

That's the marketing definition. Here's the finance definition, which is the one that actually matters at $5M-$50M ARR: PLG is a decision to shift acquisition cost out of sales and marketing headcount and into product investment, support infrastructure, and lower average contract value. You are trading ACV for volume and trading sales cycle length for conversion rate.

That trade-off shows up directly in your model:

- Sales and marketing expense as a percentage of revenue typically runs lower in PLG companies, because you're not paying a rep to close every deal.

- Gross margin can run tighter in the early funnel, because free and low-tier users consume infrastructure and support before they convert.

- Revenue per account is lower, which means you need volume and expansion to hit the same ARR target a sales-led company reaches with fewer, larger accounts.

None of that is good or bad on its own. It's a different shape of P&L — one that changes your operating leverage profile — and your forecasting model needs to reflect that shape, not a generic SaaS template borrowed from an enterprise sales-led peer group. This is the same discipline we lay out in FP&A for startups: the decision-grade framework for $5-50M ARR: the model has to match how the business actually generates revenue, not a template.

How to calculate the metrics that determine whether PLG is working

Four numbers tell you whether a PLG motion is economically sound. Track all four together. Any one in isolation will mislead you.

1. CAC payback period (gross-margin adjusted)

CAC payback = Customer acquisition cost / (New customer ARR x Gross margin / 12)

For a self-serve motion, "acquisition cost" should include the fully loaded cost of the free tier: infrastructure, support headcount servicing free users, and any paid acquisition spend that feeds the top of funnel. Founders routinely undercount this because "the product sells itself" doesn't mean the product is free to run — OpenView's CAC payback research makes the same point about loading true acquisition costs into the denominator, not just paid spend.

2. Product qualified lead (PQL) to paid conversion rate

PQL to paid conversion = Accounts that hit your defined usage/value threshold and convert to paid / Total accounts that hit that threshold

Define the PQL threshold with intent, not just enthusiasm: a specific usage event, seat count, or feature adoption pattern that correlates with willingness to pay. OpenView's research shows PQLs convert at 15-30% — far higher than MQLs — but only when the threshold is defined by actual product behavior, not guesswork. If you can't state the threshold in one sentence, you don't have a PQL definition. You have a hope.

3. Net revenue retention and gross revenue retention, tracked separately

NRR = (Starting ARR + expansion - contraction - churn) / Starting ARR

GRR = (Starting ARR - contraction - churn) / Starting ARR

PLG motions can post strong NRR while GRR quietly deteriorates, because expansion from a shrinking base of surviving accounts masks a high churn rate. SaaS Capital's 2025 retention benchmarks show that NRR and GRR diverge most sharply at lower ACVs — exactly where PLG motions tend to operate. We walk through why both numbers need to sit side by side on the same slide in NRR vs GRR in SaaS: what each metric measures and how to use both.

4. Time to value and activation rate

Activation rate = Users who reach your defined "aha moment" / Total signups

This isn't a product metric you hand off to the product team and forget. Time to value drives your CAC payback directly: the longer it takes a user to find value, the more free-tier cost you carry before any revenue shows up, and the lower your conversion rate holds steady.

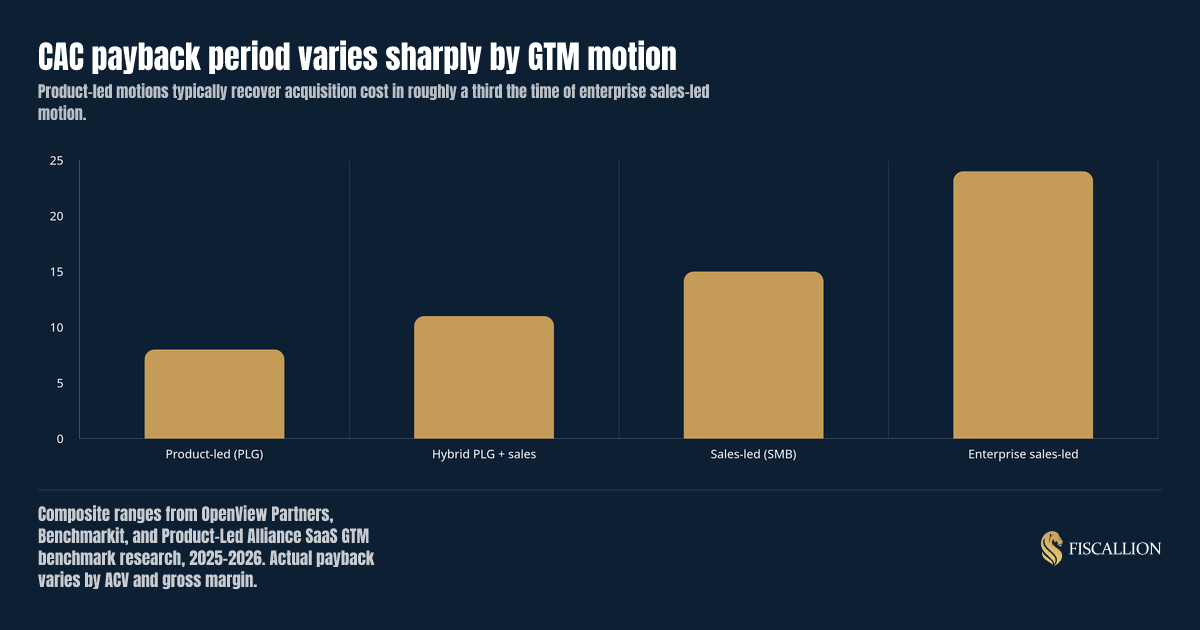

Here's how CAC payback compares across GTM motions, based on composite ranges from OpenView Partners, Benchmarkit, and Product-Led Alliance SaaS benchmark research:

How to interpret your PLG numbers without fooling your board

A fast CAC payback number in isolation is not evidence of a healthy PLG motion. It's evidence of a fast payback number. Interpretation requires the pair.

| PLG signal | Looks healthy alone | What it actually means paired with churn/GRR |

|---|---|---|

| CAC payback under 8 months | Efficient acquisition | Only sound if GRR holds above roughly 85-90%; otherwise you're recycling acquisition spend on accounts that won't stay |

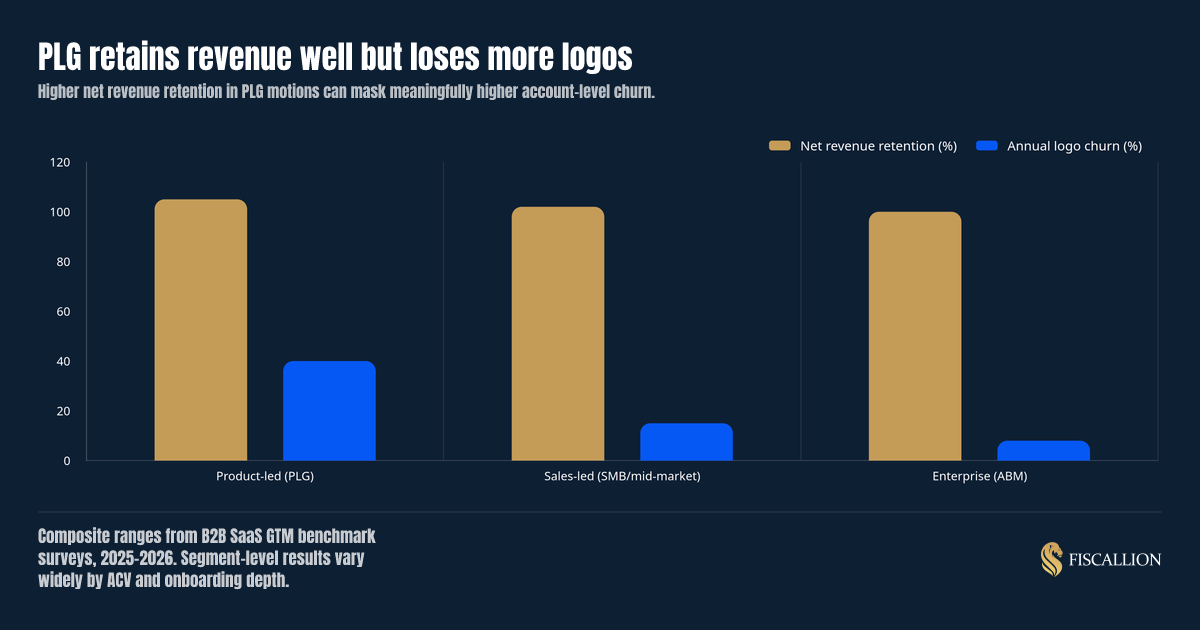

| NRR above 105% | Strong expansion | Can mask 30-50% annual logo churn common in self-serve SMB motion; check GRR separately |

| High signup volume | Strong top of funnel | Meaningless without a PQL conversion rate; vanity signups without activation drive support cost, not revenue |

| Low ACV | Broad addressable market | Requires very high volume to hit ARR targets; forces a scale-or-fail dynamic that sales-led motion doesn't have |

The chart below shows why this pairing matters. PLG motions frequently post better net revenue retention than sales-led peers, but with meaningfully higher account-level churn sitting underneath it.

If your board deck shows NRR without GRR, you are one slide away from a growth story that quietly stops being true. ChartMogul's SaaS Retention Report analyzed 2,100+ SaaS businesses and found that companies with net retention above 100% grow 1.5-3x faster than those below 60% — but only when the underlying GRR holds. That's the exact gap we flag when we audit reporting packages: reporting that shows numbers but doesn't tell the board what decision to make next.

What to do next: the decisions PLG forces onto your operating plan

PLG is not a set-and-forget motion. It creates specific, recurring decision points that a sales-led model doesn't force in the same way.

- Set an explicit ACV threshold for adding sales-assisted motion. Decide the account size, usage pattern, or expansion signal that triggers a human touch. Without this threshold, you either under-serve accounts that would pay more with help, or you overstaff sales too early against a self-serve base that doesn't need it.

- Model headcount against activation rate, not signup volume. Support and customer success headcount in PLG scales with active accounts and usage complexity, not raw signups. Hiring against top-of-funnel vanity numbers is one of the more common headcount planning mistakes we see at this stage.

- Separate free-tier cost from paid-tier cost of goods sold in your gross margin calculation. If you're blending them, your reported gross margin overstates the true economics of your paid base. This connects directly to the contribution margin in SaaS work: know what each cohort actually contributes before you decide how hard to push growth.

- Build a cohort-level CAC payback view, not a blended one. A blended number across free-to-paid conversions, expansion upgrades, and sales-assisted upsells tells you nothing actionable. Segment by acquisition channel and starting plan tier.

- Revisit the runway model whenever activation rate shifts by more than a few points. Activation rate is the single input most likely to move your CAC payback and your burn multiple at the same time, and most forecasts don't treat it as a first-class assumption.

The 3-3-2-2-2 rule (covered in detail below) still applies as your board's growth reference point, whether you run PLG, sales-led, or hybrid. What changes is the mechanism, not the target.

For a deeper breakdown of how ARR growth benchmarks shift by stage and how the 3-3-2-2-2 trajectory holds up against real private SaaS data, see our full ARR growth rate benchmark analysis.

Common mistakes and the replacement moves

Mistake: treating "self-serve" as "free to acquire." Free-tier infrastructure, support tickets, and onboarding automation all cost money. If you're not loading that cost into CAC, your payback period is fiction.

Replacement move: build a fully loaded CAC that includes infrastructure and support cost attributable to free and trial users, not just paid acquisition spend.

Mistake: reporting NRR without GRR on the same page. A single expansion-inflated retention number hides account-level churn until it shows up in a slower quarter.

Replacement move: put GRR next to NRR on every board slide where retention appears. If the gap between them is widening, that's the leading indicator, not the trailing one.

Mistake: hiring a sales team the moment growth slows, without a defined ACV or usage trigger. This is a headcount decision made from anxiety, not a model.

Replacement move: define the specific account signal (usage threshold, seat count, inbound request pattern) that justifies adding sales-assisted motion, and hire against that signal, not against a missed quarter.

Mistake: using a single blended CAC payback number across all channels and tiers. It averages away the actual signal you need.

Replacement move: segment CAC payback by channel and starting plan. A 6-month blended number can hide a 20-month payback on your highest-cost paid acquisition channel.

Mistake: assuming PLG means you don't need a forecasting discipline. Some founders treat self-serve motion as inherently more predictable because it's automated. Automation is not the same as predictability.

Replacement move: build activation rate, PQL conversion, and expansion rate into your rolling forecast as first-class assumptions you revisit monthly, the same way you'd revisit a sales pipeline.

A practical asset: the PLG metrics scorecard

Use this scorecard structure in your next board update or internal metrics review. It forces the pairing that a single-metric dashboard won't.

| Metric | This quarter | Last quarter | Trend | Trigger for action |

|---|---|---|---|---|

| CAC payback (fully loaded, cohort-level) | Rising two quarters in a row | |||

| PQL to paid conversion rate | Below your defined threshold for two cohorts | |||

| NRR | Any decline quarter over quarter | |||

| GRR | Below 85% for self-serve, below 90% for sales-assisted | |||

| Activation rate | Below your defined "aha moment" benchmark | |||

| Blended vs cohort CAC payback delta | Delta wider than 3 months |

If you want this built into your actual forecast model instead of a static table, that's the exercise worth running before your next board meeting.

Frequently asked questions

What is the 3-3-2-2-2 rule of SaaS?

The 3-3-2-2-2 rule is a five-year ARR growth benchmark: starting from a meaningful base, typically around $1M ARR, a company triples annual revenue for two consecutive years, then doubles it for three consecutive years. Run the full sequence and you land near $72M ARR by year five ($1M to $3M to $9M to $18M to $36M to $72M).

It's a variation on the earlier T2D3 framework (triple, triple, double, double, double), which assumed a higher $2M ARR starting base and was popularized by Neeraj Agrawal at Battery Ventures to describe the trajectory of companies like Salesforce and Zendesk. The 3-3-2-2-2 version is slightly more forgiving on the starting point but sets the same expectation: venture-scale growth compounds hard in years one and two, then moderates into a still-aggressive doubling pace.

For a PLG company, this rule matters differently than it does for a sales-led one. Hitting a tripling year through self-serve acquisition alone requires either a very large addressable market or a viral, network-effect product. Most PLG companies that hit this trajectory add a sales-assisted layer somewhere between year two and year three, once average account value and expansion revenue can carry growth that pure self-serve volume can't sustain alone. Missing the rule by a year or two isn't disqualifying. What matters to your board is the trend and the reason for the gap, which is why we treat this as a benchmark to stress-test your model against, not a target to force.

What is an example of product-led growth?

Slack, Calendly, Notion, Figma, and Dropbox are commonly cited PLG examples, and each illustrates a different mechanism inside the same broader motion.

- Slack let teams sign up and start using the product with zero sales contact, and grew through built-in virality: every teammate invited into a workspace became a new potential paid seat.

- Calendly used a generous free tier to get individual users hooked on a specific workflow (scheduling), then expanded revenue through team and business tiers once usage crossed a threshold that made the paid features worth it.

- Figma combined a genuinely collaborative, browser-based product with a freemium model, so the product's core value (real-time collaboration) created the upgrade trigger naturally, without a sales conversation.

What all three share is not "no sales team ever." It's that the product creates the initial value and the initial upgrade signal, before any human sales involvement. The finance detail that matters for your model: each of these companies added sales-assisted or enterprise sales motion once ACV and account complexity justified it. PLG got them to product-market fit and early scale efficiently. It did not replace the need for a monetization strategy at the high end of their customer base.

What is PLG vs SLG?

PLG (product-led growth) and SLG (sales-led growth) are the two dominant SaaS go-to-market motions, and the difference sits in what drives acquisition, qualification, and conversion.

| Dimension | Product-led growth (PLG) | Sales-led growth (SLG) |

|---|---|---|

| Primary acquisition driver | Free trial or freemium product experience | Sales team outreach, demos, and negotiation |

| Lead qualification | Product usage data (PQLs) | Marketing and sales qualification (MQLs/SQLs) |

| Typical sales cycle | Days to a few weeks | Weeks to several months |

| Typical CAC payback | Roughly 6-12 months | Roughly 15-24+ months, longer at enterprise ACV |

| Typical ACV | Lower, often under $15K | Higher, often $25K to $250K+ |

| Headcount model | Product, support, and success-heavy | Sales-heavy, with SDR/AE ratios to manage |

| Retention pattern | Often stronger NRR, weaker GRR | Often stronger GRR, more moderate NRR |

| Best fit | Broad market, fast time to value, low configuration | Complex products, enterprise buyers, long evaluation cycles |

Neither model is inherently superior, and the framing of PLG vs SLG as a binary choice is where most founders go wrong. The decision that actually matters is where in your customer base the product can close the deal on its own, and where it can't. Most companies at $5M-$50M ARR run both simultaneously: self-serve below a defined ACV threshold, sales-assisted above it. The financial planning question isn't "which model are we," it's "where's the line, and does our forecast reflect two different unit economics profiles operating inside the same P&L."

Is PLG just a trend?

No, and treating it as a passing trend is itself a decision mistake. PLG is a durable, permanent category of go-to-market motion, not a fad that fades once venture funding tightens.

What has shifted is the naive version of PLG, the idea that a good enough product removes the need for monetization discipline, pricing structure, or eventual sales investment. That version was always going to break at scale, and it has, at plenty of companies that assumed self-serve growth would carry them indefinitely without ever defining an upgrade path for larger accounts.

The durable version of PLG that's still standing is narrower and more disciplined: use the product to drive efficient acquisition and activation at the low end of the market, track cohort-level unit economics honestly, and add sales-assisted motion deliberately once account complexity or ACV justifies it. That's not a trend. That's a GTM motion with its own forecasting requirements, the same way sales-led growth has its own pipeline math, quota planning, and SaaS magic number benchmarks.

The mistake to watch for isn't PLG fading out. It's founders holding onto a pure self-serve narrative for board reporting purposes after the operating reality has already shifted to a hybrid model. If your sales-assisted revenue is growing faster than your self-serve revenue, your board deck should say so, regardless of which motion built your brand.

Conclusion

Product-led growth is a legitimate, durable go-to-market motion, and it comes with its own economics, not a shortcut around economics. The founders who get the most out of it treat CAC payback, PQL conversion, NRR, and GRR as a paired system they check every quarter, not a highlight reel for the board deck.

The 3-3-2-2-2 rule still sets the growth bar whether you're self-serve, sales-led, or hybrid. What changes is the mechanism you use to get there, and the specific decision points, ACV thresholds, activation benchmarks, headcount triggers, that a PLG motion forces onto your operating plan earlier than a sales-led one does.

If your board deck reports PLG metrics without answering what to do next when they move, that's a forecasting and metrics-definition gap, not a reporting problem. Audit your metrics definitions and forecasting model before your next board cycle so the numbers you present are the ones that actually drive the next decision.