Most founders can tell you their MRR off the top of their head. Ask them for their precise runway number - the method used to calculate it, which burn figure it's based on, and the trailing period applied - and the answer gets murkier fast.

That gap is not a character flaw. It is a systems problem. The startup runway calculation looks deceptively simple: divide cash by burn. But the number that actually matters to an investor, to a board, and to your own decision-making is several layers deeper than that. Use the wrong burn input, pick the wrong trailing period, or skip scenario modeling, and you end up with a number that feels like financial clarity but is actually false confidence.

At Fiscallion, we work with founders from Seed through Series D - across SaaS, marketplaces, platforms, and tech-enabled services - and the runway calculation comes up in nearly every first conversation. Not because founders haven't run the math, but because they've run it in a way that makes it unreliable when it matters most: in a board meeting, in a fundraising process, or at 2am when growth has stalled and you need to know exactly how long you have.

This guide covers the full picture: the formulas, the decisions behind them, the benchmarks investors use, and the modeling layer that turns a static number into an actual decision tool.

Key takeaways

- Runway is not one number - it is a method. Gross burn and net burn produce materially different results, and investors know which one you are using.

- A 3-month trailing average is the default for a reason: it smooths volatility without obscuring recent trends.

- The "when to start fundraising" calculation is as important as the runway number itself - most founders start too late.

- Scenario modeling (base, downside, extension) converts your runway calculation from a snapshot into a strategic instrument.

- Investors at Series A and beyond expect you to present net runway with a defined trailing period and a stated burn composition - not a single headline number.

- Reporting runway without specifying these inputs creates avoidable credibility risk in investor conversations.

What we'll cover

- The two burn rate definitions and why they produce different runway numbers

- The baseline runway formula and its three calculation variants

- How to apply a trailing average correctly

- Runway benchmarks by funding stage

- Scenario modeling: base, downside, and extension cases

- The fundraising trigger calculation

- The five most common runway calculation mistakes

- How to present runway to investors and your board

The two burn rate definitions you need to separate before calculating anything

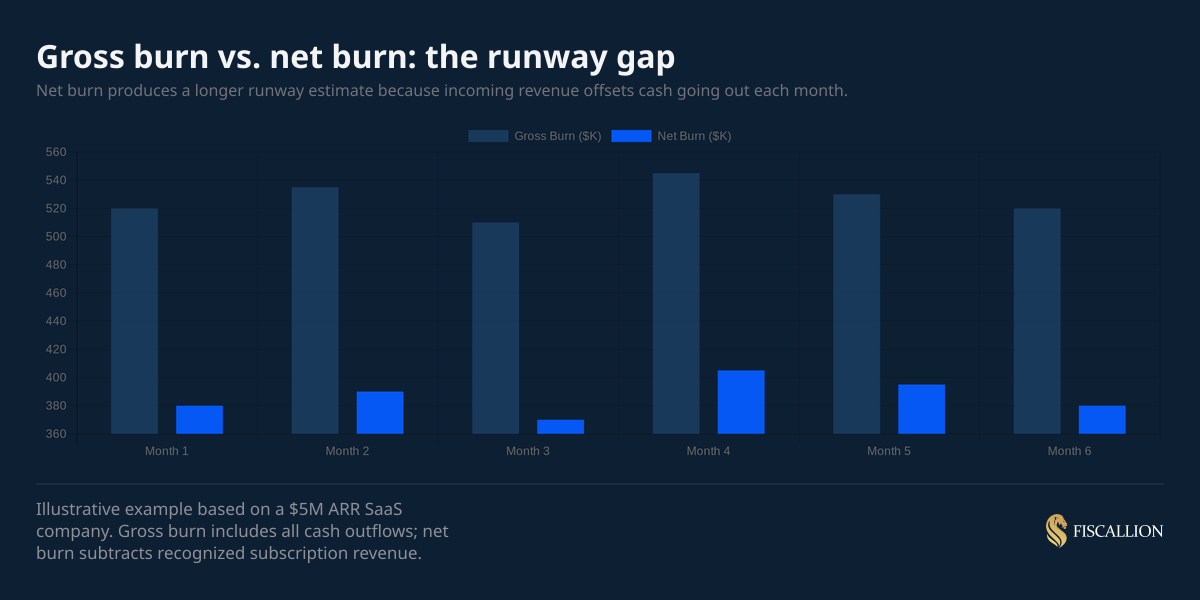

Before you divide anything, you need to decide which burn number you are dividing with. This is not a minor technicality. At a $500K/month gross burn with $140K in monthly subscription revenue, the difference between gross and net runway is roughly 3-4 months - the same gap that can determine whether you raise from a position of strength or desperation.

Gross burn rate is the total cash your company spends in a given month - payroll, rent, software, contractors, debt service, everything. It does not offset any revenue. It answers the question: how much cash goes out the door each month, regardless of what comes in?

Net burn rate is the cash your company actually consumes after accounting for revenue received. It is the difference between total cash outflows and total cash inflows during the same period. Net burn is what drives the bank balance down. It is the number that determines how long the cash lasts.

As Y Combinator partner Tim Brady puts it in YC's startup library, "burn rate is a measurement of cash flow, not profit and loss" - a distinction that catches founders out more often than it should.

Net runway is the standard for investor conversations. Gross runway has its uses - primarily for stress-testing scenarios where revenue is at risk - but leading with gross burn in a board context when the board assumes net burn creates a 2-4 month discrepancy in the headline number every time. We covered this in detail in our SaaS board reporting framework.

The right presentation is always explicit: "Net runway is 16 months on a 3-month trailing net burn average of $310K/month. Gross burn is $480K/month. The $170K difference is subscription revenue recognized in the period."

That single sentence removes the ambiguity. Without it, the investor or board member will make their own assumption about which burn figure you used - and they will often assume the more conservative one.

The baseline startup runway formula

The core formula is:

Runway (months) = Cash balance / Monthly net burn rate

If you have $2.4M in the bank and your net burn is $150K/month, your runway is 16 months. That is the headline.

But the formula immediately raises a question: which monthly burn rate figure do you use? There are three valid approaches, and each has a context where it makes sense.

Method 1: Last month's burn rate

Runway = Current cash / Last month's net burn

The fastest calculation. Use it for a quick real-time check when you need an approximate read.

The limitation: a single month can be materially distorted by timing - a large one-time payment, a delayed payroll run, an early vendor invoice. If last month is not representative, the runway number will not be either.

Method 2: 3-month trailing average (recommended default)

Runway = Current cash / Average net burn over the last 3 months

This is the industry standard for a reason. Three months is long enough to smooth out one-off events and short enough to reflect recent operational changes. It is what most investors and boards will implicitly assume you are using when you say "18 months of runway."

If you say "18 months" without specifying the period, a sophisticated investor will ask. Use the 3-month trailing average and state it explicitly.

Method 3: Forward-looking burn rate (from financial model)

Runway = Current cash / Projected monthly net burn (next 3-6 months)

This is the most analytically correct approach for planning purposes, and it is what a CFO-level financial model produces. Instead of dividing by historical burn, you divide by what you expect burn to be given your current headcount plan, committed contracts, and pipeline.

The risk: if the forward model is optimistic, the runway number is optimistic. Forward-looking runway is only as good as the assumptions behind it. Always validate it against the trailing average. If the forward model produces a runway that is more than 20% longer than the trailing-average calculation, challenge your assumptions.

The most common cause of that divergence is a lumpy expense event that is known but not yet reflected in the trailing average — typically an annual contract renewal, a planned hiring wave, or a one-time payment like a tax settlement or a vendor true-up. The trailing average looks fine because those costs have not landed yet.

The forward model is correct.

The founder presents the trailing average in the board meeting because it is the number they are used to looking at, and the board asks why the forward runway is materially shorter. The reconciliation that works is a simple bridge: trailing average burn, plus identified step-up items with amounts and timing, equals forward burn rate. It takes one slide and three line items.

What it does is demonstrate that the founder knows exactly why the numbers diverge and has already thought about each item. The alternative — presenting the trailing average without the bridge and waiting for the board to ask — looks like the founder has not done the analysis, even if they have.

How to calculate monthly net burn rate correctly

The formula for monthly net burn is:

Monthly net burn = Total cash outflows - Total cash inflows (for the same month)

Or equivalently:

Monthly net burn = Opening cash balance - Closing cash balance (adjusting for any new investment received)

The second version is cleaner because it is derived directly from your bank statement - no classification decisions required. If your bank balance started the month at $2.1M, ended at $1.85M, and you received no new investment or debt, your net burn was $250K.

Important: "total cash inflows" means cash actually received - not revenue recognized. Accrued revenue that has not been collected does not reduce your burn. Annual contracts where cash was received upfront in a prior month do not reduce this month's burn, even though they contribute to this month's MRR. Cash basis is the only correct basis for burn rate and runway calculations.

Building the 3-month trailing average

With $1,620,000 remaining and a $260K/month average net burn:

Runway = $1,620,000 / $260,000 = 6.2 months

That is a 6-month runway on a 3-month trailing basis. That is the number you take to the board and to investors - and that specific context goes with it.

Runway benchmarks by funding stage

How long your runway should be depends heavily on where you are in your company's lifecycle. The benchmarks below reflect current investor expectations in 2025-2026, where fundraising cycles have extended and investors expect founders to operate with a larger safety buffer than was typical in 2020-2021.

A few notes on these benchmarks:

Pre-seed and seed: Milestones are still being proven. Hiring and go-to-market experiments consume cash at uneven rates. The Series A timeline has extended significantly - Carta's analysis of 3,365 US startups found that 39% of companies now take 3+ years to get from seed to Series A, up from just 18-21% in 2018-2019. The conventional wisdom of "raise 18-24 months of runway" is no longer sufficient for most seed-stage companies.

Series A: This is the stage where runway discipline matters most in investor conversations. A Series A investor expects to see 18+ months of net runway post-raise, modeled explicitly. Presenting 12 months of runway without a clear path to profitability or the next milestone is a red flag. Per Carta's data published on SaaStr, the median time from Series A to Series B has now reached 2.5 years - which means post-Series A runway planning needs to account for a substantially longer inter-round period than founders typically model.

Series B and beyond: At this stage, burn multiple becomes as important as raw runway. A company with 24 months of runway burning at 3x net burn multiple is not in the same position as one burning at 1.2x. The number needs context. (More on burn multiple in the section below.)

Scenario modeling: from a static number to a decision instrument

A single runway calculation is a snapshot. It tells you where you are today, under the assumptions that currently hold. That is useful, but not sufficient for planning.

Scenario modeling converts your runway calculation into a decision instrument by asking: what happens to my runway if key assumptions change?

At a minimum, build three scenarios:

Base case

Your current operating plan - the financial model you are running the business against. Hire the people planned, spend the budget allocated, hit the revenue targets projected. Calculated on a forward-looking basis against your current headcount plan and pipeline.

Downside case

Revenue at 70-80% of plan, hiring plan delayed by one quarter, key contract at risk. This scenario answers: if things do not go as planned, how much time do we have? This is what your investors are mentally stress-testing when they review your deck.

Extension case

What specific levers could extend runway by 3-6 months without structurally impairing the business? Identify them by name: a hiring pause on two open roles, a vendor contract renegotiation, accelerating payment collection on outstanding invoices, a bridge from an existing investor. Each action should have a number attached to it.

The extension case matters because runway extension decisions often have to be made quickly and under pressure. If you have pre-modeled what a 3-month extension looks like and what it costs, you can execute it in days rather than weeks.

One company hit the nine-month threshold mid-year in a difficult fundraising environment.

The pre-modeled extension plan had two components: a 20% reduction in non-headcount operating expenses, and a pause on two planned hires that had not started yet. Both were modeled as reversible within 90 days if the raise closed. They executed both. The expense cuts were straightforward. The hire pause was harder — one of the candidates had already verbally accepted and had to be told the start date was being pushed. That candidate withdrew and took another offer.

When the raise closed four months later, the role had to be re-recruited from scratch, adding roughly three months to the original timeline for that function to be staffed.

Scenario modeling template

The extension case shows that $50K/month in identified cost reductions (hiring freeze + vendor renegotiation) restores 3 months of runway even under the downside revenue scenario. That is actionable.

The fundraising trigger calculation: when runway math actually matters

The most important number in runway planning is not your current runway. It is the date you need to start your fundraising process.

The calculation:

Fundraising start date = Today's date - (current runway - fundraising duration - runway buffer at close)

Working through it:

- Current runway: 18 months

- Typical fundraising duration: 4-6 months for a Series A (longer for Series B+)

- Minimum runway you want to have remaining at close: 3 months (so you are not negotiating from zero leverage)

Start fundraising when you have: 4-6 months (raise) + 3 months (buffer) = 7-9 months of runway remaining

Which means: with 18 months of current runway, you should start your fundraising process in roughly 9-11 months. Not 13 months. Not "when we hit our next milestone." Nine months from now, so that you reach your investors with a full 9 months of runway still on the clock rather than 4.

This calculation has a direct impact on hiring decisions too. If you know you need to be in fundraising mode in 9 months, a new hire that takes 4 months to onboard and contributes to burn immediately needs to clear the milestone bar before you start the process - not after.

At Fiscallion, this is one of the first things we build when working with venture-backed startups on their financial model: a fundraising timeline that works backwards from current runway, so the "when to start" decision is a calculated date, not a gut call.

The five most common runway calculation mistakes

In the course of working with early-to-mid stage founders across SaaS and tech-enabled businesses, we see the same five errors repeat across companies at Series A through Series C. Each one is fixable, but each one also creates real credibility risk if it surfaces in an investor conversation unprepared.

Mistake 1: Using recognized revenue instead of received cash

Revenue recognition and cash receipt are not the same thing. If you sign a $120K annual contract in March and recognize $10K/month, only the cash receipt in March (the upfront payment) actually reduces your burn in March. Subsequent monthly recognition has no cash impact.

Runway is a cash metric. Build it from bank statements, not P&L.

Mistake 2: Including uncommitted pipeline revenue

Some founders include expected revenue from pipeline deals in their runway calculation. "We have 14 months, but if we close the two deals in late-stage, it extends to 18."

That is a forecast, not a runway number. Investors understand the nuance, and they will ask which version they are looking at. Keep the runway number clean - only cash received counts. Model the pipeline upside separately in your scenario analysis.

Mistake 3: Using a single month's burn rate as the baseline

Last month may have been unusually high or unusually low. A $60K one-time payment to a contractor, a delayed payroll cycle, a vendor invoice that hit early - any of these can distort a single month by 15-25%. Always use the 3-month trailing average as your stated baseline.

Mistake 4: Not accounting for committed future headcount

Your current burn rate reflects your current team. If you have three offers out that will close in the next 60 days, your burn rate will step up - often by 15-20% in a fast-hiring period. The forward-looking runway should include committed headcount, not just the people currently on payroll.

This is the headcount plan discipline we described in the SaaS board reporting framework: approved roles, in-process roles, and modeled roles all produce different burn forecasts. Know which version your runway number uses.

Mistake 5: Setting it and forgetting it

Runway is a monthly metric, not a quarterly one. Cash and burn can shift materially within a four-week window - a revenue slowdown, an unexpected engineering contractor engagement, a delayed customer payment. Set a recurring weekly check that takes five minutes: current cash balance, last week's spend rate, pipeline receipts expected this month. That cadence means you are never surprised by a runway calculation.

How to present runway to investors and your board

Runway is one of those metrics where how you say it matters as much as what you say. A confident, precise presentation signals financial literacy. A vague or inconsistent one signals the opposite.

What to say:

"Net runway is 17 months on a 3-month trailing net burn average of $295K/month. Gross burn is $460K/month. The $165K delta is primarily subscription revenue. Our base case financial model shows 19 months at planned headcount. Downside scenario at 75% of revenue is 13 months."

What not to say:

"We have about 16-18 months of runway."

The first version says: this founder knows their numbers, has a defined methodology, and has modeled the scenarios. The second version says: this founder is estimating.

At the Seed stage, the first version may not come naturally. That is understandable. But by Series A, any investor will expect you to present with this specificity. If you are not there yet, the path forward is straightforward: lock down your definitions, install the 3-month trailing average as your standing calculation, build your scenario models, and report on them consistently.

For SaaS startups and bootstrapped companies alike, the infrastructure is the same - what changes is how investor-facing the outputs need to be and how frequently the model needs to be updated. The same applies for marketplaces and platforms and tech-enabled services businesses, where revenue timing and cash conversion cycles introduce additional complexity into the burn calculation.

Board decision rules for runway thresholds

Once you have a reliable runway calculation, attach decision rules to it. This converts runway from a reported number into an action trigger. The examples below are starting points - your specific thresholds should reflect your cost structure, investor commitments, and growth trajectory.

Having these rules written down before you need them eliminates the most expensive aspect of a runway crisis: the decision latency. When conditions are already stressed, the last thing you need is a two-week deliberation about what to do.

A note on burn multiple: the runway metric Series B investors actually use

Raw runway tells you how long your cash lasts. The burn multiple tells investors how efficiently you are buying that growth. At Series B and beyond, sophisticated investors increasingly evaluate both numbers together.

The burn multiple, introduced by David Sacks, is defined as:

Burn Multiple = Net Burn / Net New ARR

It answers: how much is the company burning to generate each incremental dollar of ARR? A burn multiple of 1x means you are spending $1 of net burn for every $1 of new ARR added. A 3x burn multiple means you are spending $3 to generate $1. The lower the multiple, the more efficiently you are growing.

Sacks's framework provides useful benchmarks: under 1x is excellent, 1-1.5x is good, 1.5-2x is acceptable, and anything above 2x warrants scrutiny - especially past Series A. The burn multiple is particularly powerful because it simultaneously reflects gross margin problems, sales efficiency issues, churn, and leadership discipline. If something is structurally wrong with the business, the burn multiple will catch it even when headline growth looks healthy.

The practical implication for runway planning: a company with 24 months of runway burning at a 3x multiple has a different investor conversation than one with 18 months of runway at a 1.2x multiple. The second company is in a demonstrably stronger position, even with less cash on the clock.

Building the financial infrastructure behind the number

The calculation itself is arithmetic. The hard part is building the financial infrastructure that makes the calculation reliable, current, and defensible.

The components you need:

1. A reconciled cash balance, updated weekly. Not the accounting balance. The actual bank balance, net of any outstanding checks or scheduled transfers. This is the numerator in your runway calculation and it needs to be accurate.

2. A rolling burn model with a 3-month trailing tab. Automate this in your financial model. Each month, the trailing average updates automatically based on actual bank movements. Anyone on your leadership team can pull the runway number at any time without a finance cycle.

3. A headcount plan with three columns. Approved roles (offer accepted and start date confirmed), in-process roles (active search, no offer yet), and modeled roles (in the plan but no open req). Each column produces a different burn forecast. Know which one you are using.

4. A scenario model with at least two cases. Base and downside, with the extension levers explicitly identified. This does not need to be complex - it needs to be maintained. A simple, updated model outperforms a sophisticated but stale one every time.

5. A written definition that everyone agrees on. Before your next board meeting: write one sentence that defines your runway calculation method, and share it with your Finance lead and your board chair. "Our runway is calculated as current cash balance divided by 3-month trailing net burn. Net burn excludes any uncommitted pipeline revenue." That is it. Thirty words that eliminate a category of board meeting friction.

This is the infrastructure Fiscallion builds for every client engagement - whether they are a pre-revenue Seed company or a $30M ARR SaaS business heading into a Series C. The math is not the hard part. The hard part is operationalizing it so the number is trustworthy and current every single week.

Conclusion

Startup runway calculation is not a formula you run once. It is an operating discipline - a number that needs a defined method, a clean data source, a regular update cadence, and scenario context before it earns the right to drive your most important decisions.

The founders who navigate fundraising, cash crunches, and hiring decisions with the most confidence are not the ones with the most runway. They are the ones who know their runway number precisely, understand what it assumes, and have already modeled what happens when those assumptions change.

If you can say: "Net runway is 16 months on a 3-month trailing average of $290K net burn. Our downside scenario puts it at 11 months. We have identified $55K/month in extension levers that restore 3 months under the downside case. We plan to start our Series A process in month 7" - you are operating with CFO-level financial clarity.

That is the standard. It is achievable at any stage, and it is the difference between a number that lives in a spreadsheet tab and one that actually runs the company.

If you are not there yet and want a direct read on where your runway model stands, Fiscallion's CFO Advisory works with founders at exactly this stage - turning financial fog into a structured, defensible number that holds up in any room.

Read more: How to Calculate Your Fully Burdened Labor Rate and Stop Undercharging for Your Team’s Time