Cash collected and revenue recognized are not the same number. Most SaaS finance models treat them as close enough until a board meeting, a fundraise, or an audit makes the gap impossible to ignore.

Revenue recognition in SaaS is where accounting and FP&A intersect most directly. Get it right and your income statement, ARR bridge, and deferred revenue balance tell a coherent story. Get it wrong and you will either overstate your current financial position or build forecasts on cash numbers that have nothing to do with what you have earned.

This article covers the mechanics of ASC 606 for SaaS, the five-step recognition model, the most common recognition methods, and how the benchmarks your board cares about — the Rule of 40, the 3-3-2-2-2 rule — connect back to how you recognize revenue. It also answers the question founders ask at every stage transition: is SaaS capitalized or expensed?

Key takeaways

- Revenue is recognized when you satisfy a performance obligation, not when cash arrives. Annual prepays create deferred revenue, not recognized revenue, until the service is delivered.

- The five-step ASC 606 model applies to every contract, including upgrades, downgrades, bundled onboarding fees, and mid-term modifications.

- Rule of 40 and the 3-3-2-2-2 growth benchmark are both affected by how you recognize revenue - a billing mix shift from monthly to annual can distort both metrics without any change to underlying business performance.

- SaaS development costs follow a three-phase model: preliminary work is expensed, application development is capitalized, post-implementation is expensed. Sales commissions over one year must also be capitalized under ASC 340.

What we'll cover

- What revenue recognition means for SaaS and why cash timing creates FP&A risk

- The five-step ASC 606 model applied to SaaS contracts

- The four most common recognition methods and when each applies

- Common recognition traps in SaaS contracts

- What the Rule of 40 actually measures - and what revenue recognition has to do with it

- The 3-3-2-2-2 rule: what it demands from your finance model

- Is SaaS capitalized or expensed? The answer depends on which cost you mean

- The top 8 SaaS revenue recognition tools compared

- Actions ordered by impact and common mistakes to replace

Revenue recognition is a timing problem, not just a compliance requirement

In a single-transaction business, revenue recognition is straightforward. You sell something, you ship it, you record the revenue. SaaS complicates this because you collect cash at one point in time and deliver value over a different, often longer, period.

A customer who pays $36,000 upfront for a three-year subscription does not generate $36,000 in revenue at signing. Under US GAAP, you recognize $1,000 per month as you deliver the service. The $36,000 sits on your balance sheet as a liability — deferred revenue — until earned.

This is not a technicality. It affects three decisions you make constantly:

- Runway forecasting. Your cash balance includes future service obligations. If you use raw cash to calculate runway, you are overstating your true financial position, particularly when annual billing is a significant proportion of ARR.

- Board reporting. Recognized revenue, ARR, and billings can all move in different directions at the same time. Presenting one without the others leaves your board unable to assess revenue quality.

- Valuation. Acquirers and investors typically apply a haircut to deferred revenue because it represents an obligation, not an asset. A large, fast-growing deferred balance from customers with strong renewal rates is a positive signal. The same balance from contracts with early-stage churn risk is a liability in every sense. For a deeper look at how deferred balances affect SaaS valuation multiples, the mechanics are covered in detail there.

The underlying problem at most $5M–$50M ARR companies is not that founders do not understand the accounting. It is that no one has connected the recognition schedule to the cash model, the ARR bridge, and the board deck in a single coherent framework.

The five-step ASC 606 model for SaaS

ASC 606, effective for private companies since 2018, establishes a single five-step framework for recognizing revenue across all industries. For SaaS, each step has specific implications.

Step 1: Identify the contract

A contract is any enforceable agreement - an order form, a click-through acceptance, a renewal, or an amendment. Mid-term changes such as upgrades or downgrades are contract modifications. ASC 606 requires you to evaluate whether a modification creates a new contract or alters the existing one.

The practical implication: every change to a customer's subscription has a revenue recognition consequence. If your sales and finance teams do not have a documented process for handling contract modifications, you will accumulate recognition errors at scale.

Step 2: Identify the performance obligations

For a standard SaaS subscription, the primary obligation is continuous access to the platform over the contract term. But any add-on that provides standalone value — onboarding, professional services, dedicated support — is a separate performance obligation with its own recognition schedule.

The failure mode here is treating everything as a single obligation. If you bundle a $10,000 implementation fee with a $50,000 annual subscription and recognize the whole contract ratably, you are likely misallocating the transaction price and overstating near-term subscription revenue.

Step 3: Determine the transaction price

The transaction price is the total consideration you expect to receive: base subscription fees, usage charges, discounts, credits, and any variable amounts tied to consumption. For usage-based or hybrid pricing, you cannot recognize variable revenue upfront under ASC 606 — it must be recognized in the period the usage occurs.

Step 4: Allocate the price to obligations

When a contract includes multiple performance obligations, you allocate the total price based on the standalone selling price (SSP) of each component. SSP is what you would charge if you sold each element separately.

Most SaaS companies arrive at this step with either a single SSP for everything or no documented policy at all. Both create audit exposure. Before your Series B process, have a documented SSP policy for every element you bundle. KPMG's Revenue Recognition Handbook provides detailed worked examples of SSP allocation that are worth reviewing if you are building this policy for the first time.

Step 5: Recognize revenue as obligations are satisfied

For subscriptions, revenue is recognized over time because the customer receives value continuously. This is typically straight-line over the contract term. For one-time deliverables like implementation milestones, revenue is recognized at the point of completion. For usage-based fees, revenue is recognized in the period usage occurs.

The four recognition methods and when each applies

The straight-line method is the default for SaaS subscriptions. Usage-based recognition is increasingly common as hybrid pricing models grow. The key mistake in usage-based recognition is treating total contract value as recognized revenue before usage is confirmed - a pattern that inflates near-term recognized revenue and creates restatement risk.

Recognition traps that show up at every funding round

Minor drafting choices in your sales agreements routinely trigger major compliance failures when technical accounting standards are applied to your contracts.

Non-refundable upfront fees

If you charge a setup or onboarding fee that does not represent a distinct standalone deliverable, that fee must be recognized over the subscription term, not at contract start. Many early-stage SaaS companies recognize these fees immediately, which overstates month-one revenue and understates the deferred balance.

Termination clauses and cancel-anytime contracts

If your contract allows the customer to cancel at any time with a pro-rata refund, the noncancelable portion is what governs the recognition schedule under ASC 606. A monthly cancel-anytime subscription is effectively a one-month contract for recognition purposes — even if most customers stay for years. This directly limits how much deferred revenue you can legitimately carry.

Multi-year contracts with variable pricing

Annual step-up pricing, volume discount structures, and ramp deals require careful allocation across periods. The most common error is recognizing revenue based on the amount invoiced in a given year rather than the total contract value allocated across the entire term.

Improperly scheduling upfront implementation fees or tracking multi-year escalators on a simple cash-received basis represents an immediate red flag for institutional investors during due diligence. When these non-compliant practices are uncovered, the resulting forced revenue restatements can instantly deflate a company's trailing-twelve-month metrics and severely damage valuation leverage.

Contract modifications mid-period

An upgrade in month four of a 12-month contract is not simply an add-on. ASC 606 requires you to evaluate whether it creates a new contract or modifies the existing one. If it modifies the existing contract, you may need to reallocate the remaining transaction price and adjust the recognition schedule retroactively. EY's Financial Reporting Developments guide on ASC 606 covers the modification analysis framework in detail.

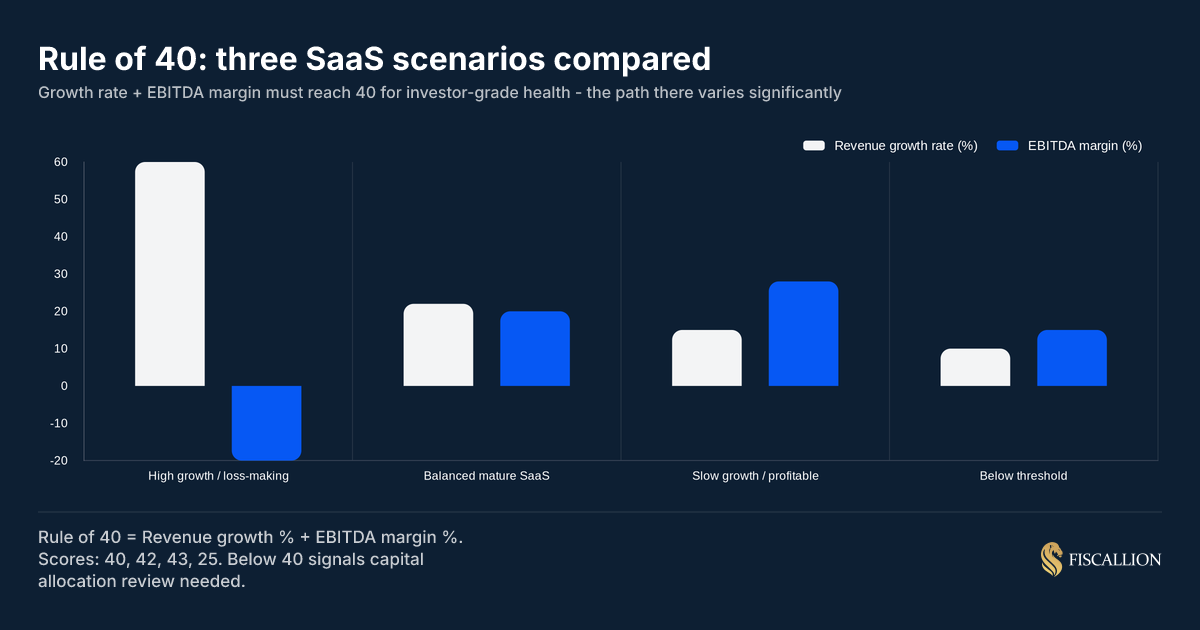

What is the Rule of 40 for SaaS?

The Rule of 40 is a single-number test of whether your SaaS business is balancing growth and profitability at an investor-grade rate. For a deeper breakdown of the formula variants and how to use it as a diagnostic rather than a headline number, see the Rule of 40 in SaaS: formula, benchmarks, and how to use it as a founder.

Formula: Revenue growth rate (%) + EBITDA margin (%) ≥ 40

A company growing at 60% ARR with a -20% EBITDA margin scores 40. A company growing at 22% with a 20% EBITDA margin also scores 42. Both pass, but they reflect completely different capital strategies, risk profiles, and operational decisions.

A BCG analysis of 107 private B2B SaaS companies found that only 9% of companies under $30M ARR exceeded a Rule of 40 score. That figure rises to 26% for companies above $80M ARR. The gap reflects higher relative sales and marketing expense, higher R&D as a percentage of revenue, and lower gross margins at smaller scale. A separate McKinsey analysis of more than 200 software companies found that businesses exceeded Rule of 40 performance only 16% of the time — and that top-quartile SaaS companies generate nearly three times the EV/revenue multiples of those in the bottom quartile.

What revenue recognition has to do with your Rule of 40 score

Revenue recognition affects both inputs:

- Revenue growth rate. If you shift customers from monthly to annual billing, recognized revenue may lag ARR growth during the transition period. The deferred balance grows, but the income statement does not yet reflect the full picture. This can make your YoY revenue growth rate look lower than ARR growth for a quarter or two.

- EBITDA margin. Capitalized software development costs and capitalized contract acquisition costs (commissions under ASC 340) reduce current-period GAAP expenses. If your finance team is expensing all development labor and commissions immediately, your EBITDA margin is artificially low compared to a company that capitalizes correctly.

The practical consequence: before benchmarking your Rule of 40 against industry comps, confirm that your EBITDA inputs reflect correct capitalization treatment and that your revenue growth rate is based on recognized revenue under ASC 606, not billings or ARR.

What is the 3-3-2-2-2 rule of SaaS?

The 3-3-2-2-2 rule is a revenue growth benchmark for venture-backed SaaS companies. Starting from approximately $1M ARR, the model calls for tripling revenue in years one and two, then doubling it in years three through five.

The rule evolved from the older T2D3 framework, which started at a higher ARR base and assumed more upfront capital. The 3-3-2-2-2 model reflects the post-2022 investor shift toward capital efficiency and measured growth over burn-funded velocity.

What this benchmark demands from your finance model

The 3-3-2-2-2 trajectory is not a marketing narrative for your pitch deck. Each year's target creates downstream pressure on specific financial decisions:

CAC payback period. At 3x growth, you are adding more new customers than you have ever had in a single year. If CAC payback is 18 months, you are consuming significant cash before those customers contribute margin. The 3-3-2-2-2 pace typically requires CAC payback to compress toward 12 months or below by year two of tripling. OpenView's benchmark data confirms that 12 months is considered best-in-class CAC payback across most go-to-market motions, and that top-quartile McKinsey SaaS companies recover CAC in under 16 months while bottom-quartile players take nearly four years.

Headcount model. Tripling ARR does not mean tripling headcount. If your costs grow proportionally with revenue, your Rule of 40 collapses before you reach the doubling years. Companies that hit 3x efficiently do it through GTM improvements, pricing expansion, and product improvements - not by hiring at the same rate.

Billing mix and deferred revenue. As you close more annual contracts to support growth targets, your deferred revenue balance grows. If you are funding operations partly on the float from annual prepays, model the cash impact of even a 5-10% softening in renewal rates. That scenario changes your runway calculation materially.

When the 3-3-2-2-2 rule does not apply

This benchmark is designed for venture-backed SaaS with institutional exit ambitions. It is the wrong reference point if:

- You are bootstrapped or operating under a profitability mandate

- You serve a niche vertical with a defined market ceiling

- Each customer requires significant implementation effort, which limits GTM scalability

In those cases, what matters is whether your growth rate supports margin improvement and competitive retention, not whether it matches a VC-era template.

Is SaaS capitalized or expensed?

The question has two distinct answers depending on which costs you mean. The accounting treatment is different for the software costs you incur to build your product versus what your customers incur to implement it.

Your own software development costs (ASC 350-40)

Under ASC 350-40, the costs you incur to build your platform are treated differently across three project phases:

The decision impact: if your engineering team is building new features, a portion of those salaries may qualify for capitalization. This reduces your GAAP operating expenses now but creates an amortization charge across future periods. It directly affects your EBITDA margin and your Rule of 40 score. In 2025, FASB issued ASU 2025-06, which updated how certain internal-use software costs are staged and capitalized. If your capitalization policy predates those changes, it warrants a review — Deloitte's Heads Up on the amendments provides a practical breakdown of what changed and what stays the same.

Sales commission capitalization (ASC 340)

Commissions paid to close contracts with terms longer than one year must be capitalized and amortized over the expected customer benefit period under ASC 340. Expensing all commissions at close is not GAAP-compliant if you have multi-year contracts.

This matters because the correction often moves in your favor — capitalizing commissions previously expensed typically improves EBITDA margin for the trailing twelve months. But if it surfaces during a Series B diligence process, it raises questions about what else may need restating, which adds time and negotiating friction to a raise regardless of the outcome. For context on how this flows through to your overall valuation position, see how commission capitalization affects SaaS valuation multiples and investor scrutiny during diligence.

Even when an accounting adjustment technically works in a startup’s favor by shifting past expenses off the income statement and boosting paper profitability, sophisticated investors rarely celebrate the surprise change. Instead, an unprompted mid-diligence correction signals a fundamental lack of financial maturity, prompting buyers to dig deeper into the corporate ledger for hidden liabilities.

What customers incur to implement your product (also ASC 350-40)

When enterprise customers implement your SaaS product, they follow the same three-phase model to determine which implementation costs they can capitalize on their own balance sheets. Understanding this matters for your sales process: if your pricing structure or contract terms make your product's implementation costs harder to capitalize, larger buyers may resist adoption or renegotiate price.

The top 8 SaaS revenue recognition tools

Once your contract volume grows beyond what a spreadsheet can handle reliably, purpose-built software becomes necessary. The right tool depends on your contract complexity, billing model, integration requirements, and company stage.

How to choose between them

At the $5M–$30M ARR stage, the most common mistake is choosing a tool based on brand familiarity rather than contract complexity and integration fit. A few questions to guide the decision:

- Does your billing happen in Stripe, Recurly, or a custom system? Native integrations reduce the manual data entry that creates recognition errors.

- Do you have multi-element contracts, bundled onboarding, or variable pricing components? Those require allocation logic that not every tool handles correctly.

- Is your accounting in QuickBooks, Xero, or an ERP? Your recognition tool needs to post journal entries to your GL automatically, or you are recreating the spreadsheet problem in a different format.

- Are you approaching a Series B or preparing for audit? Audit-ready trails and documented allocation policies matter more than dashboard aesthetics at that stage.

For most SaaS companies between $5M and $30M ARR, Maxio or Chargebee RevRec will cover the core use case without the implementation overhead of Zuora or Workday. If you are already inside the NetSuite or Salesforce ecosystem, the native modules are the lower-friction path.

Actions ordered by decision impact

These are the moves that change your financial model, your board reporting quality, and your fundraising readiness — ordered by the size of the decision they affect.

1. Build or reconcile your deferred revenue waterfall (owner: head of finance or controller)

Create a monthly schedule: opening balance, new deferred from billings, revenue recognized, closing balance. Reconcile it against your ARR bridge every quarter. If the deferred balance is not moving in the direction your ARR bridge predicts, something is misaligned in your billing system, recognition schedule, or contract terms.

2. Audit your commission expensing under ASC 340 (owner: controller or external accountant)

If you have contracts longer than 12 months and are expensing all commissions at close, your income statement is non-compliant. Correct this before a raise. The correction typically improves EBITDA margin for the trailing twelve months — but surfacing it mid-diligence is harder than addressing it proactively.

3. Document your standalone selling prices for bundled contracts (owner: finance + legal)

If you bundle implementation, training, or support with a subscription and cannot produce documented SSPs for each element, you have an allocation problem. Auditors and diligence teams will ask. Define SSPs now and apply them consistently.

4. Review your software capitalization policy for the 2025 ASC 350-40 amendments (owner: controller)

FASB's ASU 2025-06 amends how certain cloud-enabled software costs are staged, which changes what engineering labor qualifies for capitalization. If your policy was written before these changes, review it now. PwC's viewpoint coverage of the update is a practical starting point.

5. Stress-test your Rule of 40 inputs (owner: CEO + finance)

Before your next board meeting, confirm that your revenue growth rate is based on recognized revenue under ASC 606 and that your EBITDA margin reflects correct capitalization treatment. If you benchmark against industry data using inconsistent inputs, the comparison is meaningless.

6. Include billings, deferred balance, and recognized revenue in every board report (owner: CEO + finance)

Your board should see all three numbers, not just ARR. The difference between billings and recognized revenue tells the story of how contracted revenue converts to income. The deferred balance tells the story of how much near-term recognized revenue is already locked in.

7. Model the cash impact of billing mix changes before offering discounts for annual plans (owner: CEO + finance)

Annual prepay improves cash but increases your service obligation. Before deciding what discount to offer, build a 12-month cash bridge that shows the break-even discount rate and the cash impact at each renewal cohort. A 20% annual discount may look attractive until you model what happens when 12% of that cohort does not renew.

Common mistakes and the replacement moves

Mistake: reporting billings as revenue

Billings and recognized revenue are different numbers. If your monthly update to the board says "we did $400K in revenue" and that number is actually billings, you are reporting a number that does not appear anywhere on a GAAP income statement. Replace this with a side-by-side table: billings, recognized revenue, and the change in deferred balance.

Mistake: using cash balance to calculate runway without adjusting for deferred obligations

Cash in the bank includes prepaid customer payments that still have a service obligation attached. If a customer who prepaid $120,000 churns at month three, you owe a refund. Your runway model should subtract the refund exposure embedded in your deferred balance, adjusted for your expected annual churn rate.

Mistake: recognizing all upfront fees immediately

Setup, onboarding, and implementation fees bundled into a subscription contract are not automatically recognizable at contract close. If the deliverable does not have standalone value, the fee must be recognized over the subscription term. Recognizing it immediately overstates month-one revenue and understates your deferred balance.

Mistake: treating contract modifications as new sales

When a customer upgrades mid-contract, your CRM treats it as expansion revenue and flags it as a win. Your accounting team needs to treat it as a contract modification under ASC 606 and evaluate whether to adjust the remaining recognition schedule. The two systems can diverge significantly over a quarter, which creates confusion in ARR bridges and board reports.

Mistake: not tracking deferred revenue by cohort

A growing deferred balance looks healthy. But it only stays healthy if the underlying contracts renew. Deferred revenue from customers who have not engaged with the product since onboarding is renewal risk, not future revenue. Segment your deferred balance by product adoption tier, contract size, or renewal timing. This gives you a more accurate picture of what your income statement will actually look like in months four through nine.

Revenue recognition tool selection checklist

Use this before evaluating any tool. If you cannot answer these questions, your evaluation criteria are not defined.

REVENUE RECOGNITION TOOL SELECTION CHECKLIST CONTRACT PROFILE

[ ] Contract volume per month: ___________

[ ] Do you have multi-element contracts (subscription + onboarding/services)? Y / N

[ ] Do you have usage-based or variable pricing components? Y / N

[ ] Do you have multi-year contracts? Y / N

[ ] Do you have international contracts or multi-currency? Y / N BILLING SYSTEM

[ ] Current billing system: ___________

[ ] Does the rev-rec tool have a native integration with your billing system? Y / N

[ ] Is the integration real-time or batch/nightly? ___________ GL INTEGRATION

[ ] Current accounting system / ERP: ___________

[ ] Does the tool post journal entries automatically? Y / N

[ ] Does it support your chart of accounts structure? Y / N COMPLIANCE REQUIREMENTS

[ ] Are you currently or will you soon be audited? Y / N

[ ] Do you need IFRS 15 in addition to ASC 606? Y / N

[ ] Do you have documented SSPs for all performance obligations? Y / N STAGE AND SCALE

[ ] Current ARR: ___________

[ ] Target ARR in 18 months: ___________

[ ] Does the tool scale to that ARR without forcing an upgrade or migration? Y / N COST AND IMPLEMENTATION

[ ] Estimated monthly / annual cost: ___________

[ ] Estimated implementation time (weeks): ___________

[ ] Data migration required? Y / N

[ ] Training budget allocated? Y / N

Revenue recognition is an operational reality, not just compliance

Revenue recognition in SaaS is not an accounting problem you hand off to a controller and revisit at audit time. It is a FP&A problem that affects every number your board sees, every fundraising conversation you have, and every hiring or runway decision you make with imprecise inputs.

The companies that handle this well are the ones where a decision-owner - whether that is a founder, head of finance, or fractional CFO - connects the recognition schedule to the ARR bridge, the deferred revenue waterfall, and the cash model in a single coherent framework. That connection is what makes financial reporting actionable rather than retrospective.

If your current setup treats recognized revenue, billings, and ARR as interchangeable, start with the deferred revenue waterfall. Get the reconciliation right. Then work backwards: commission capitalization, software cost allocation, SSP documentation. In that order.

Fiscallion works with Series A to Series C SaaS companies to build the FP&A infrastructure that makes these numbers legible from a single model. If your recognition schedule and your cash model are not speaking the same language yet, audit your metrics definitions and forecasting model.

Frequently asked questions

What is the 3-3-2-2-2 rule of SaaS?

The 3-3-2-2-2 rule is a revenue growth benchmark for venture-backed SaaS companies. Starting from approximately $1M ARR, the model calls for tripling revenue in years one and two, then doubling it in years three through five — mapping a path to roughly $72M ARR over five years.

It evolved from the older T2D3 framework as a more capital-efficient alternative suited to post-2022 investor expectations. T2D3 assumed a higher starting ARR base and heavy upfront capital; the 3-3-2-2-2 model is more accessible for companies at $1M–$5M ARR and places greater weight on sustainable retention and margin discipline rather than burn-funded speed.

The benchmark is most relevant for companies planning institutional raises or large exits. If you are bootstrapped, serving a niche with a defined market ceiling, or running a high-services-delivery model, the 3-3-2-2-2 trajectory is the wrong reference point. What matters in those cases is whether your growth rate supports margin improvement and retention quality — not whether it matches a VC-era framework.

The practical use case for this rule is planning and pressure-testing: it gives you a target to reverse-engineer, which clarifies when to hire, how aggressive your GTM budget needs to be, and what CAC payback threshold is required to stay cash-efficient at each growth multiple.

What is the best tool for SaaS revenue recognition?

There is no single best tool. The right choice depends on your contract complexity, billing system, integration requirements, and company stage. The eight platforms that cover the majority of SaaS use cases are: Maxio (SaaS-native, strong at subscription analytics), Chargebee RevRec (ideal if you already use Chargebee for billing), Zuora Revenue (enterprise and complex multi-element contracts), Sage Intacct (fast month-end close), NetSuite RevRec (multi-entity or ERP-native teams), Salesforce Revenue Cloud (Salesforce-native organizations), Workday Financial (US GAAP + IFRS 15 dual-standard needs), and Stripe Billing (usage-based or developer-built pricing models). For most SaaS companies between $5M and $30M ARR, Maxio or Chargebee RevRec will cover the core use case without the implementation overhead of enterprise platforms.

Is SaaS capitalized or expensed?

It depends on which costs you are asking about. For your own software development under ASC 350-40, costs in the preliminary project phase (planning, feasibility) are expensed. Costs in the application development phase (writing code, integration testing, QA) are capitalized and amortized over the useful life, typically 2–5 years. Costs in the post-implementation phase (bug fixes, hosting, maintenance) are expensed. Sales commissions on contracts with terms longer than one year must be capitalized and amortized under ASC 340 — expensing them at close is not GAAP-compliant. FASB's 2025 amendments to ASC 350-40 (ASU 2025-06) changed how certain cloud-enabled software costs are staged — if your capitalization policy predates those changes, it warrants review.

What is the Rule of 40 for SaaS?

The Rule of 40 is a financial health benchmark that adds your annual revenue growth rate to your EBITDA margin. A combined score of 40 or above is considered investor-grade. The formula is: Revenue growth rate (%) + EBITDA margin (%) ≥ 40. A company growing at 50% with a -10% EBITDA margin scores 40. A company growing at 20% with a 22% EBITDA margin also scores 42. The metric is designed to acknowledge the growth-profitability trade-off inherent in SaaS: early-stage companies that are burning to grow can pass the Rule of 40 with high growth rates compensating for negative margins; mature companies rely more on profitability. BCG's 2025 analysis of 107 private B2B SaaS companies found that only 9% of companies under $30M ARR exceed the Rule of 40 threshold. Use it as a directional diagnostic alongside NRR, gross margin, and CAC payback — not as a standalone pass/fail. The inputs matter: confirm your growth rate is based on recognized revenue under ASC 606 and that your EBITDA margin reflects correct capitalization treatment before benchmarking against any external data.