Your ARR multiple is not an output of a negotiation. It is a direct function of a small set of operating metrics you can influence today, months before any transaction. Most founders only engage with those metrics when a term sheet is already on the table.

This article breaks down how SaaS valuation multiples are set in 2026, which inputs matter most, how the Rule of 40 and Rule of 50 affect investor pricing, and what specific moves shift your multiple up before you need it to matter.

What you'll learn

- How ARR multiples are constructed and what separates a 3x company from a 10x company

- Why private company multiples differ from public comps - and by how much

- The five decisions you can make now to move your multiple before your next raise

What a SaaS valuation multiple actually measures

The formula is simple. Enterprise value equals ARR multiplied by a multiple. The complexity is entirely in what determines that multiple.

When an investor pays 6x ARR for your company, they are making a specific bet: that the combination of your growth trajectory, revenue durability, and margin efficiency will generate returns that justify that price. Your job - whether you're fundraising, running a Series B, or preparing for an eventual exit - is to produce evidence that the bet is well-founded.

Three inputs do most of the work:

- Growth rate - how fast ARR is expanding year over year

- Net revenue retention (NRR) - how much revenue is retained and expanded from the existing customer base

- Margin efficiency - how much of each revenue dollar the business converts to profit, often summarized in a Rule of 40 or Rule of 50 score

Every other factor - contract structure, customer concentration, category, team - adjusts the number upward or downward at the margins. These three drive the base.

2026 benchmarks: ARR multiples by growth rate

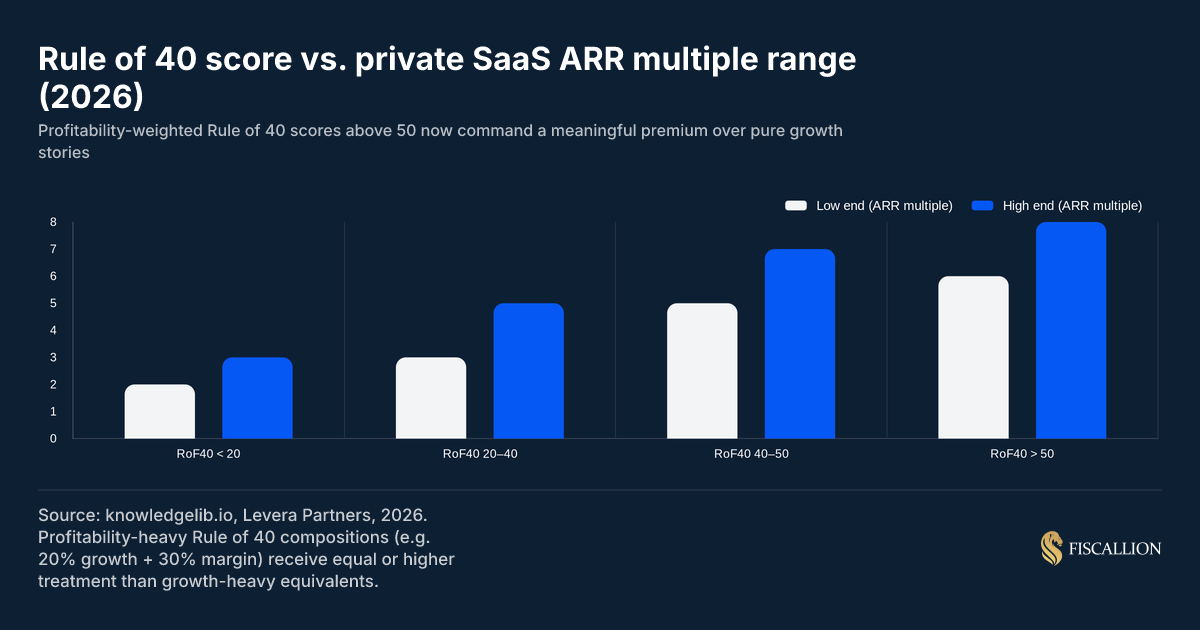

As of early 2026, the median public SaaS company trades at approximately 6-7x EV/revenue. According to SaaS Capital's 2025 SaaS Capital Index, the public SaaS median stood at exactly 7.0x run-rate ARR at the start of 2025 - down roughly 60% from the 2021 peak but stable in the 6-7x band that last held in 2015-2016. The top quartile - companies with Rule of 40 scores above 50 and NRR above 120% - reaches 13-14x. The bottom quartile, where growth is below 10% and margins are deeply negative, sits at 1-2x.

Private companies carry a 20-30% illiquidity discount relative to public comparables, plus a size discount for smaller businesses. SaaS Capital's data puts the private SaaS median at 4.8x for bootstrapped companies and 5.3x for equity-backed companies. The realistic ranges for private SaaS companies in 2026:

And by growth rate:

The range within each tier is large. A company growing at 35% can trade anywhere from 4x to 9x depending on NRR, gross margin, and Rule of 40 score. Growth gets you into the right tier. The other metrics determine where you land within it.

The 10x rule in SaaS: what it means and when it applies

The "10x rule" in SaaS refers to a loose valuation shorthand used in the venture market: high-growth SaaS businesses - typically those growing at 100% or more annually - can command approximately 10x ARR or higher. In practice this was more commonly applied in the 2019-2021 bull market when capital was cheap and revenue multiples for fast-growing public companies reached 20-30x.

The rule still applies in a narrower form today. A private company growing at 100%+ with strong unit economics, NRR above 115%, and a Rule of 40 score above 50 can realistically achieve 10-14x ARR in a growth equity or late-stage financing context.

The key constraint: the 10x threshold requires efficient growth, not just fast growth. A company doubling ARR with a burn multiple above 2x - meaning it spends more than $2 to generate $1 of net new ARR - is unlikely to reach 10x in 2026 conditions regardless of the growth rate. Capital efficiency has become a pre-condition, not an afterthought.

For the $5M-$50M ARR companies Fiscallion works with, the actionable version of the 10x rule is this: if you're growing above 60-80% with NRR above 115% and gross margins above 75%, you are in the range where a 7-10x outcome is realistic at your next financing. That is the profile to aim for, not the top-line growth rate in isolation.

What is the Rule of 40 in SaaS valuation?

The Rule of 40 is the most-used composite efficiency metric in SaaS. The formula:

Rule of 40 score = Revenue growth rate (%) + Profit margin (%)

A score of 40 or above signals that a company is either growing fast enough to justify its burn, or profitable enough to justify slower growth - or some combination of both. McKinsey's analysis of more than 200 software companies found that businesses exceeded Rule of 40 performance only 16% of the time - and that top-quartile SaaS companies generate nearly three times the EV/revenue multiples of those in the bottom quartile. Hitting 40 consistently is a genuine differentiator, not a low bar.

Which profit margin to use

The definition of "profit margin" in the Rule of 40 formula varies, and the choice matters when comparing companies:

- EBITDA margin - most common for later-stage and public market analysis. Strips out interest, taxes, depreciation, and amortization.

- Free cash flow (FCF) margin - increasingly preferred by growth equity investors because it captures actual cash generation and is harder to smooth with accounting choices. McKinsey's research specifically flags LTM FCF percentage as the metric most correlated with value multiples for mid-to-large SaaS companies.

- Operating income margin (EBIT) - useful for GAAP-consistent comparisons.

For early-stage companies where both EBITDA and FCF are significantly negative, the formula still applies. A company burning at a -40% margin needs 80%+ ARR growth to hit the threshold.

Rule of 40 benchmarks by stage

The median public SaaS company scores around 35-40. Real examples from SaaS Capital's index: Veeva Systems has historically run at 45-55 by combining 15-20% growth with 30%+ EBITDA margins. Datadog posted scores above 60 during its 2020-2022 growth phase by running 60%+ ARR growth.

What the Rule of 40 does not capture

The Rule of 40 does not measure capital efficiency. A company that raised $300M to post a Rule of 40 score of 43 is telling a fundamentally different story than one that reached the same score on $30M raised. Always pair the Rule of 40 with burn multiple and ARR per dollar raised to get the full picture.

It also looks backward. For a $10M ARR company planning its Series B, forward NRR and pipeline coverage are more predictive than trailing Rule of 40 score. Use it as one input to the investor narrative, not as a substitute for full FP&A context.

What is the Rule of 50 for SaaS companies?

The Rule of 50 raises the efficiency bar: revenue growth rate (%) plus FCF margin (%) must equal or exceed 50. It reflects the shift that began in 2023 and has solidified through 2025-2026 - investors now weight efficient growth more heavily than raw top-line speed. The Bessemer Venture Partners Cloud 100 Benchmarks Report consistently shows the highest-valued cloud companies outperforming on exactly this combination of growth efficiency and FCF margin.

Standard Rule of 50 formula:

Rule of 50 = Revenue growth rate (%) + FCF margin (%) ≥ 50

A weighted version has gained traction in later-stage diligence:

(Growth rate × 1.33) + (FCF margin × 0.67) ≥ 50

The weighting still favors growth slightly, but demands that burn is controlled. If your growth is strong but cash burn is uncontrolled, the weighted score surfaces the problem quickly.

Rule of 50 vs. Rule of 40: what changed

The Rule of 40 was calibrated for an era when capital was cheap and growth could be "purchased." Under that logic, a company burning aggressively to grow at 60% made the math work. The Rule of 50 reflects the post-2022 reality: growth still matters, but investors increasingly price in how growth is achieved.

What a Rule of 50 score actually requires

Reaching 50 consistently requires three things to be working simultaneously:

- NRR above 115-120% - expansion from existing customers reduces the cost of growth and lifts FCF margin without additional S&M spend.

- CAC payback under 12-18 months - efficient acquisition means more of the revenue dollar flows to margin, not just to filling the funnel.

- Controlled headcount scaling - G&A costs flat relative to revenue as ARR scales. The efficiency ratio to track: ARR per full-time employee.

For a company at $15M ARR with 35% growth and -5% FCF margin, the Rule of 50 gap is 20 points. Closing it requires either accelerating growth (expensive) or improving margin (operationally difficult at scale). Most companies that successfully bridge the gap do it through NRR - by improving retention and expansion rather than pouring more into new acquisition.

What is a good CAGR for SaaS?

For private SaaS companies in the $5M-$50M ARR range, a good compound annual growth rate (CAGR) depends heavily on stage:

As a general benchmark: 20-50% CAGR is considered healthy for most Series A to Series C SaaS companies. Growth above 50% is strong. Growth above 100% at $10M+ ARR is exceptional and warrants a different valuation conversation.

The important nuance: CAGR quality matters as much as the rate. A company growing at 45% through unsustainable channel spend, heavy discounting, or a one-time cohort of churny customers is not in the same position as one growing at 35% with NRR at 115% and improving gross margins. Investors have become considerably better at distinguishing these profiles since 2022. McKinsey's own research found that just 1.6% of 200 software companies sustained revenue growth of 30% or higher consistently over a decade - which puts aggressive growth targets in their proper context.

The T2D3 framework - triple, triple, double, double, double - describes the growth trajectory associated with the fastest-growing SaaS companies from $1M to $100M ARR. Originally published by Battery Ventures, it describes the growth path to a billion-dollar company. Most companies in the $5M-$50M range are at some point in the T2D3 arc and should benchmark against those growth expectations when approaching institutional capital.

How NRR moves your multiple - more than growth does

Net revenue retention is the single most underestimated valuation input for companies below $50M ARR. Here is the formula:

NRR = (Starting ARR + Expansion - Churn - Contraction) / Starting ARR × 100

The valuation mechanics:

- NRR above 120%: adds 1-2x to your ARR multiple

- NRR 110-120%: adds 0.5-1x

- NRR 100-110%: neutral

- NRR below 100%: subtracts 1-2x, and triggers investor concern about product-market fit durability

McKinsey's November 2025 research on B2B SaaS companies found that top-quartile-valued B2B SaaS companies achieve NRR of 113% versus 98% for their bottom-quartile peers - and that the top-quartile by valuation multiple (median EV/revenue of 24x) showed stronger NRR performance than the bottom quartile (5x) across every market condition between 2019 and 2024. An earlier McKinsey analysis of 40 public B2B SaaS companies found that those with NRR above 120% had a median EV/revenue of 21x compared with 9x for those below that mark. The mechanism is clear: a 120% NRR business doubles its existing customer base every five years without acquiring a single new customer. New acquisition then compounds on an already-growing base.

For a deeper look at what these benchmarks mean by ARR stage and how to interpret your own NRR number, see our net revenue retention benchmarks guide for SaaS companies.

One important constraint: high NRR only commands a premium when paired with positive new ARR growth. A company with 130% NRR but declining net-new acquisition is signaling customer base dependency, not durable expansion. Investors read that pattern as a warning signal, not a strength.

Gross margin: the floor that determines what multiple is possible

Gross margin is not a valuation input on its own - it is more like a pre-condition. A company with gross margins below 60-65% will struggle to command meaningful ARR multiples regardless of growth, because the underlying unit economics cannot support the cost structure of a premium business.

For pure-play SaaS with minimal services revenue, gross margins above 75% are expected. Above 80% is the range where investors have meaningful confidence in the path to operating leverage. The Bessemer Venture Partners Cloud 100 Benchmarks Report consistently shows the top cloud companies maintaining gross margins in the 75-85% range as a baseline condition for premium valuations. Companies delivering professional services as a meaningful portion of revenue typically see gross margins in the 55-70% range, which places structural downward pressure on the multiple.

The relationship to valuation multiples:

The practical FP&A task for founders approaching a raise: know your gross margin by segment, not just overall. Infrastructure costs, implementation labor, and support headcount often hide in COGS in ways that obscure the margin profile for different customer tiers. Getting that breakdown clean before a fundraise avoids painful diligence surprises.

Public vs. private multiples: the gap founders misread

The single most common valuation mistake at the $5M-$50M ARR stage is applying public SaaS multiples to a private company without adjustment.

If the public SaaS median is 7x EV/revenue and your $8M ARR company is growing at 40%, the instinct is to value the company at 7-8x ARR, or $56-64M. That estimate will almost certainly be wrong by 30-50%.

Anchoring a capital raise strictly to the valuation multiples of high-flying public SaaS giants completely ignores the operational layer and liquidity risks that institutional investors bake into early-stage pricing.

Private companies carry a 20-30% illiquidity discount versus public comparables. They also carry a size discount that scales inversely with ARR. The realistic private market translation:

- Public median at 7x → private equivalent for a $5-20M ARR company: 4-5.5x

- Public top quartile at 13x → private equivalent for the same range: 7-9x

SaaS Capital's 2025 analysis confirms this precisely: the private SaaS median sits at 4.8x ARR for bootstrapped companies and 5.3x for equity-backed companies, versus a public median of 7.0x. Their framework - built on more than a decade of data from over 1,500 private B2B SaaS companies annually - models private valuations using three inputs: public market multiples, ARR growth rate, and NRR.

The implications for board and investor conversations: if you are presenting a valuation story to your board or a prospective lead investor, build the case from private comparables first, then reference public comps as an upside ceiling. Starting from public multiples and working down looks unsophisticated and frequently anchors the negotiation in the wrong place.

Five decisions that move your multiple before you need it

These are ordered by impact, not ease. Each maps to a specific owner and a specific time horizon.

1. Fix your NRR calculation first (owner: founder + head of CS)

If you do not have a clean, auditable NRR calculation by cohort, start here. Investors will recalculate it in diligence and any gap between your claimed NRR and their verified number destroys credibility faster than a weak number does.

- Build a cohort table that tracks starting ARR, expansions, contractions, and churn for each customer group by quarter

- Ensure your definition of expansion excludes new products sold to new business units that should technically be new ARR

- Reconcile NRR to your billing system, not just to a spreadsheet

2. Raise your Rule of 40 score with a specific lever (owner: founder + FP&A)

Do not try to improve the Rule of 40 score abstractly. Identify whether your gap is growth-side or margin-side, then target the specific input with the highest impact per dollar of effort.

- If growth is the gap: model the CAC payback impact of reallocating S&M budget from low-performing channels to your top two acquisition sources

- If margin is the gap: identify the three largest variable cost lines in COGS and S&M, and set explicit targets with owners for each quarter

- Do not cut R&D to hit a Rule of 40 score. Investors look at growth in R&D relative to ARR as a forward-looking signal - hollowing it out for a trailing metric read is a trade you will regret in diligence

3. Segment your gross margin by product and customer tier (owner: head of finance)

Overall gross margin hides the story. The gross margin on your self-serve product is probably 82%. The gross margin on your enterprise tier - factoring in implementation, dedicated CSM time, and custom support SLAs - might be 58%. Presenting blended gross margin without this breakdown leaves money on the table in a valuation conversation.

Build a gross margin waterfall that shows: infrastructure costs by product, implementation labor, support costs by tier, and the resulting gross margin per segment. This is the kind of CFO-level analysis that signals operational maturity to investors.

4. Clean up your ARR definition before the conversation starts (owner: founder)

ARR is not self-defining. Common definitional problems that compress multiples in diligence:

- Including professional services or one-time setup fees in ARR

- Counting contracts that have not yet gone live or have a cancellation clause as ARR

- Not adjusting for exchange rate movements in multi-currency businesses

- Including free trials or pilots in the ARR total

If your ARR number cannot survive a clean definition test, fix the definition before the raise. A smaller, cleaner ARR number at the right multiple is a better story than a larger, contested number that triggers a haircut.

5. Build a forward-looking model that shows the trajectory (owner: founder + FP&A)

Investors are not buying your trailing performance. They are buying their estimate of your forward performance. A company at $12M ARR growing at 35% with a credible model showing the path to $20M ARR at improving gross margin and improving NRR is a fundamentally different investment case than the same company presenting only historical data.

The model does not need to be complex. It needs to be specific and owned. Who owns the revenue forecast inputs? Who owns the headcount plan that feeds into margin? Who owns the NRR assumption? If the answer to any of those questions is "we'll figure it out before the deck," that is a signal to investors that your finance function is not operating at the level the growth stage requires.

Common mistakes and what to do instead

Valuation multiples get negotiated. The inputs that determine them get built (or neglected) months before any negotiation starts. These are the five patterns that compress multiples in diligence, and what to do instead.

Mistake: Applying public multiples to a private company

- What actually happens: the investor applies a 20-30% illiquidity discount plus a size discount and arrives at a very different number

- Fix: Build your valuation narrative from private comparables in your ARR range, then use public comps as an upside reference, not a baseline

Mistake: Reporting a single NRR number without cohort context

- What actually happens: the investor recalculates it in diligence, finds the actual cohort-level retention is lower, and loses confidence in the team's metrics literacy

- Fix: Own the cohort table. Present NRR by customer age, by segment, and with the gross retention separated from expansion so the components are transparent

Mistake: Optimizing the Rule of 40 score through cost-cutting rather than growth improvement

- What actually happens: R&D and CS headcount shrinks; future-period growth slows; the Rule of 40 score temporarily improves but the trajectory signal worsens

- Fix: Pair the Rule of 40 score with a burn multiple and a forward NRR assumption so investors can see how the efficiency is being achieved

Mistake: Treating valuation as a fundraising-only question

- What actually happens: the metrics that determine the multiple are not actively tracked between rounds, which means there is no intervention point when they deteriorate

- Fix: Review your Rule of 40 score, NRR, and gross margin by segment at every monthly business review. These are operating metrics that determine capital outcomes - they belong in the monthly cadence, not just in board decks

Treating core unit economics as data points meant only for fundraising decks can mask slow-moving operational decay that destroys enterprise value long before term sheets are drawn up.

Mistake: Conflating ARR growth rate with CAGR when presenting to investors

- What actually happens: investors build a longer-term DCF using your implied CAGR; if your most recent quarter annualizes to a rate significantly different from your trailing twelve-month CAGR, the discrepancy surfaces uncomfortable questions

- Fix: Present growth in three time horizons: trailing three months annualized, trailing twelve months, and the prior fiscal year. That sequence tells a story about acceleration or deceleration that a single CAGR number hides

Valuation multiple readiness checklist

Most valuation problems surface in diligence because the inputs were never clean to begin with. Use this checklist before any board conversation, fundraise, or investor update where your company's value is on the table.

ARR definition

- ARR excludes professional services, one-time fees, and uncancellable-contract caveats

- ARR is reconciled to billing system, not to a spreadsheet

- Multi-currency ARR is calculated at a consistent exchange rate (end-of-period or average)

NRR

- NRR is calculated by cohort, not just as a blended total

- Gross retention is separated from net retention

- Expansion ARR is segmented by type (upsell, cross-sell, seat expansion, price increase)

- NRR is reconcilable to an auditable transaction log

Rule of 40 / Rule of 50

- The profit margin input is defined (EBITDA, FCF, or operating income) and used consistently

- The score is calculated on trailing twelve months and most recent quarter

- You can explain the gap to 40 or 50 with specific, owned action items

Gross margin

- Gross margin is segmented by product and customer tier

- Infrastructure costs are assigned by product, not allocated as a blended rate

- Implementation and onboarding labor is in COGS, not in S&M

Growth trajectory

- Three-period growth rate is available: last quarter annualized, trailing twelve months, prior fiscal year

- The model includes a 12-18 month forward view with owned assumptions by input

- CAC payback period is calculated by acquisition channel and customer segment

Capital efficiency

- Burn multiple is calculated (net burn / net new ARR)

- ARR per full-time employee is tracked and trended quarterly

- Total capital raised vs. current ARR is contextualized for investor positioning

The multiple follows the metrics. Fix the inputs first

A SaaS valuation multiple is a compressed expression of what investors believe your business will generate in future cash flows. Growth rate sets the tier. NRR determines durability. Gross margin sets the ceiling for what the unit economics can ultimately support. And the Rule of 40 or Rule of 50 score tells investors whether the combination is being built responsibly.

The companies that command 7-12x ARR in private markets in 2026 are not doing so because of a single exceptional quarter. They are doing so because their NRR is clean and growing, their gross margin is segmented and defensible, their Rule of 40 score is above 45 with a credible trajectory toward 50, and their forward model is specific and owned.

Most companies at $5M-$30M ARR do not have a valuation problem. They have a metrics definition and FP&A problem - the inputs are not clean, the assumptions are not owned, and the story that emerges in diligence is weaker than the actual business warrants.

Fix the inputs. Book a working session with the Fiscallion team to audit your metrics definitions, clean up your NRR calculation, and build the forward model that supports the multiple your business deserves.