Between incorporation and Series B, the gap between the ownership percentage a founder expects and the number on the actual cap table is almost always larger than they modeled. SAFEs, option pool expansions, bridge notes, and pro-rata rights compound quietly — and by the time a term sheet arrives, the math has already moved.

This article explains how equity dilution actually works in a startup, how to calculate it correctly, what each dilution event costs you in real terms, and the decisions that determine whether you're a well-capitalized founder or a largely diluted one by the time you exit.

Key takeaways

- Every share issuance — priced round, SAFE conversion, option pool expansion, or bridge note — dilutes your ownership percentage. Most of these events happen at the same time during a fundraise, and their combined effect is almost always larger than founders expect.

- The option pool shuffle is still the single most common dilution trap. Expanding the pool pre-money before a priced round dilutes only founders and early shareholders, not the new investor — despite being framed as a neutral term-sheet item.

- Anti-dilution provisions exist on investor shares, not yours. The protection most founders think they have does not apply to their common stock in a down round — it applies to preferred shareholders. Your protection comes from valuation and round structure, not from legal clauses.

- The compound effect of raising at low valuations across multiple rounds is more damaging to founder ownership than any single round. Modeling three to five pre-money scenarios before each raise is the most important FP&A task ahead of every fundraise.

What equity dilution actually is

Equity dilution occurs when a company issues new shares, reducing the ownership percentage of every existing shareholder whose holdings remain fixed. Your total number of shares does not change. The denominator — the total number of shares outstanding — does.

If you own 4,000,000 shares in a company with 10,000,000 total shares outstanding, you own 40%. If the company issues 2,500,000 new shares to investors, you now own 4,000,000 out of 12,500,000 shares — that is 32%. You lost 8 percentage points of ownership without selling a single share.

The mechanics are simple. The decision-making around them is not.

Dilution is not inherently harmful. A smaller percentage of a much larger, well-capitalized business is usually worth more in absolute terms than a larger percentage of an undercapitalized one. The question is whether the dilution you accepted was necessary, properly priced, and consistent with your long-run ownership target at exit.

The three events that dilute your cap table

Most dilution events fall into one of three categories:

Each event is predictable. None should surprise you if you model before you negotiate.

How to calculate your post-round ownership

The basic dilution formula

The formula is straightforward:

Post-round ownership % = Your shares / (Existing shares + New shares issued)

The inputs matter more than the formula. "New shares issued" is not just the shares issued to the new investor. It includes:

- Shares issued to convert SAFEs and convertible notes

- New option pool shares added as part of the round

- Warrant shares issued to venture debt lenders (if applicable)

- Any other share issuances tied to the close

Founders frequently apply the formula to only the investor tranche, which is why they get surprised by the actual post-close cap table.

A worked example: Series A with SAFE conversion and option pool expansion

Start position:

- Founder owns 5,000,000 shares

- Early employee pool: 1,000,000 shares

- Total shares outstanding: 6,000,000

Pre-Series A events:

- Two SAFEs totaling $1.5M convert at an $8M cap → 1,125,000 new shares

- Investor requires option pool expansion from current 1,000,000 to 1,800,000 shares pre-money → 800,000 new shares before pricing the round

Post-SAFE and pool expansion:

- Total shares: 6,000,000 + 1,125,000 + 800,000 = 7,925,000

- Founder shares: still 5,000,000

- Founder ownership before new investor: 63.1%

Series A investment:

- $7M at $20M pre-money valuation

- Price per share: $20M / 7,925,000 = $2.52

- New investor shares: $7M / $2.52 = 2,778,000 shares

Post-Series A total shares: 7,925,000 + 2,778,000 = 10,703,000

Founder's final ownership: 5,000,000 / 10,703,000 = 46.7%

If the founder had only modeled the investor tranche without accounting for SAFE conversion and pool expansion, they would have expected closer to 55% post-round. The 8-percentage-point gap is not negligible.

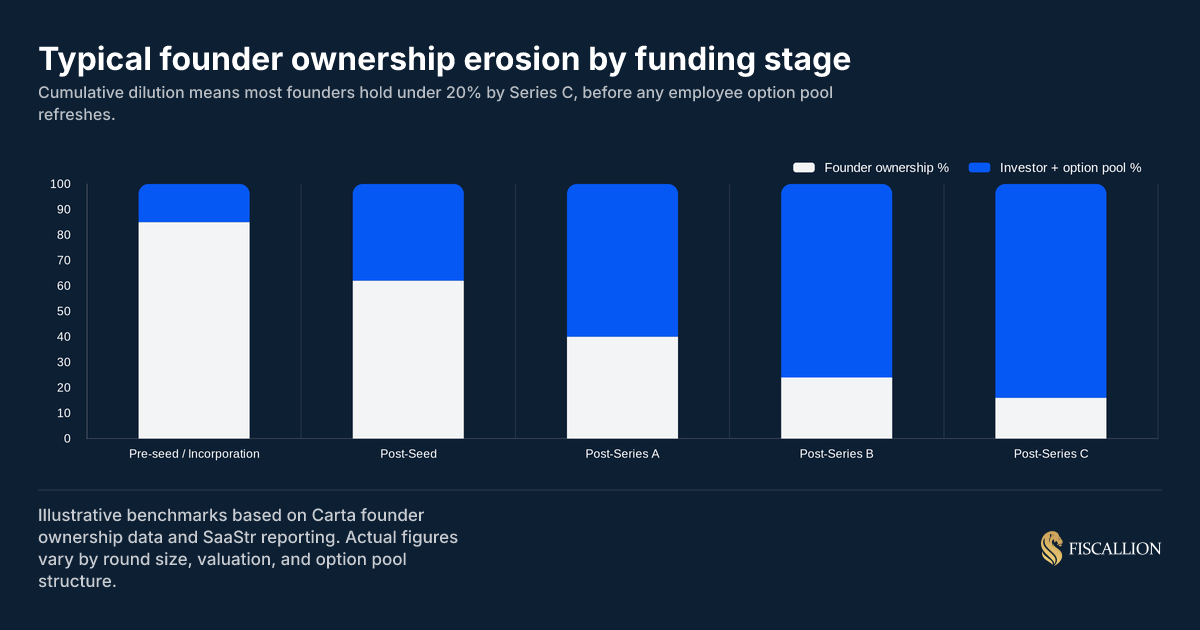

The compounding reality: ownership across multiple rounds

Most discussions about dilution focus on a single round. The more important analysis is the cumulative path from seed through Series C.

Carta's 2025 Founder Ownership Report, based on data across thousands of rounds, consistently shows the following benchmarks:

These are collective founder team numbers. If you have two co-founders splitting equity, each person's stake is half of those figures by Series B.

The compounding works against you at each stage because dilution is multiplicative, not additive. A 20% dilution round followed by a 20% dilution round does not produce 40% total dilution. It produces:

1.0 × (1 - 0.20) × (1 - 0.20) = 64% remaining — or 36% cumulative dilution

Run that model through seed, Series A, Series B, and Series C and you understand why founders who take outside capital from the earliest stages typically hold 12–18% by the time a meaningful exit occurs. This does not make fundraising wrong. It makes the valuation at each stage, and the amount raised, extremely consequential decisions that deserve FP&A treatment — not just term-sheet negotiation.

The option pool shuffle: the most expensive term-sheet item most founders miss

When a Series A investor asks you to expand the employee option pool to 15–20% as part of the round, they are almost always asking for this expansion to happen pre-money. The distinction is material.

The term was first named and explained in detail by Venture Hacks — their original breakdown of the option pool shuffle remains the clearest illustration of the mechanics and why this is a transfer of value from founder to investor dressed up as a neutral condition.

Pre-money option pool expansion means the new shares are added to the cap table before the investor's price-per-share is calculated. This lowers the effective price per share, which means the investor's $7M buys more ownership than the headline pre-money valuation implies. All the dilution from the new pool falls on existing shareholders — primarily founders — not on the new investor.

Post-money option pool expansion means the pool is added after the round closes. In this structure, the dilution is shared proportionally across all shareholders, including the new investor.

The financial difference between these two approaches is often 3–7 percentage points of founder ownership per round. Over a two to three round funding path, that difference can represent millions of dollars in exit proceeds.

The replacement move: counter any pre-money pool expansion request with a post-money structure, or negotiate the pool size down to what is realistically needed for the next 18 months of hiring — not a four-year phantom headcount plan.

If your hiring plan for the next 18 months requires 20 offers and each grant averages 0.15% of the company, the pool you need is approximately 3%, not 15–20%. Investors will argue for a larger pool because it is accretive to them. You negotiate with your actual hiring model, not a defensive posture.

How SAFEs affect dilution — and why post-money SAFEs changed the math

SAFEs (Simple Agreement for Future Equity) are now the dominant instrument for pre-seed and seed fundraising. In Q1 2025, SAFEs comprised 90% of all pre-seed rounds on Carta. Understanding the dilution mechanics of each type is not optional if you are raising.

Y Combinator, which introduced the SAFE in 2013 and revised it to the post-money format in 2018, publishes a detailed primer on post-money SAFE mechanics that is worth reading before you issue your first instrument — or your fifth.

Pre-money SAFEs: floating dilution until conversion

With a pre-money SAFE, the investor's ownership percentage remains uncertain until conversion at a priced round. The conversion price is calculated based on company capitalization before any of the SAFE investments are factored in. This means all SAFE investors in the same cohort end up diluting each other, in addition to diluting the founders.

The ambiguity creates a specific risk: you may have issued three to five pre-money SAFEs to angels and funds, each with different caps and discounts, and not know your actual fully diluted ownership until a Series A term sheet forces a cap-table reconciliation. That reconciliation often surfaces more dilution than founders modeled.

Post-money SAFEs: investor certainty at founder's expense

With a post-money SAFE — now the industry standard — the investor's ownership percentage is locked in relative to other SAFEs from the moment of investment. Two SAFE investors in the same post-money round do not dilute each other. They both dilute the founders.

The math is cleaner, but the outcome for founders is more direct. Each post-money SAFE you issue reduces your ownership immediately and proportionally. Issue $3M of post-money SAFEs on a $10M cap, and you have sold 30% of the company before a priced round starts.

The decision rule: model your SAFE stack before you issue each instrument. Know your total SAFE commitments as a percentage of your target post-money cap before you accept a new check — not after.

Anti-dilution provisions: what they protect and who they protect

Anti-dilution provisions are commonly misunderstood. They are a protection for preferred stock investors, not for founders. Understanding them matters because they affect your cap table in a down round — and because being on the wrong side of them is expensive.

The NVCA model term sheet sets the baseline standard for anti-dilution language in institutional venture rounds. Knowing what the baseline looks like makes it easier to identify when a proposed term deviates from market norms.

Broad-based weighted average (the standard, founder-friendly structure)

In a down round, the conversion price for preferred shares adjusts downward using a formula that accounts for the size of both the new issuance and the diluted total share count. The adjustment is moderate because it incorporates both the new shares and all existing shares into the calculation.

Formula (simplified):

New conversion price = Old conversion price × (A + B) / (A + C)

Where:

- A = shares outstanding before the new round

- B = new shares that would be issued at the old price for the new investment

- C = actual new shares issued at the new (lower) price

This approach distributes the down-round impact across the cap table instead of concentrating it on the founders. It is the standard in most institutional term sheets and the appropriate baseline for negotiation.

Narrow-based weighted average (less common, more investor-favorable)

Uses a smaller denominator — typically only the fully diluted preferred shares, not the entire cap table. This produces a larger downward adjustment to the conversion price, which benefits investors more than the broad-based version. Push back if this appears in a term sheet.

Full ratchet (highly investor-favorable, rarely acceptable)

In a full ratchet structure, preferred shares convert at the price of any new lower-priced issuance — regardless of the number of shares in the new round. A single share sold at a lower price triggers a full reset for all previous preferred investors.

In practice, full ratchet provisions can reduce founder ownership to near zero in a down round. They are rare in standard term sheets, but they do appear. If you see one, it should be a negotiation priority. Viridian Lawyers' breakdown of full ratchet vs. weighted average anti-dilution clauses covers the practical implications clearly for founders who want to go deeper on the mechanics.

What this means for you as a founder

None of these provisions protect your common stock. In a down round, your shares experience the full dilution of the new share issuance, plus any additional shares generated by the anti-dilution adjustments for preferred holders. Your protection is upstream: raise at the right valuation, with the right amount of capital, before you reach a position where a down round is the only option.

Dilution from venture debt: the warrants problem

Venture debt is often described as non-dilutive capital. This is partly accurate and partly misleading. The debt principal itself does not require issuing new shares. However, most venture debt facilities attach warrant coverage — typically 15–30% of the loan amount in equity value — at the time of issuance.

A $5M venture debt facility with 20% warrant coverage and a strike price equal to the current 409A fair market value grants the lender the right to purchase $1M of equity at today's price. If the company's value increases significantly before the warrants are exercised, the actual dilutive cost is higher than the headline percentage suggests.

Lighter Capital's analysis of venture debt warrants and Silicon Valley Bank's overview of when venture debt is the right instrument are both worth reviewing before modeling the trade-off. As a16z notes in their guide to startup debt, typical warrant coverage on term loans runs 20–100 basis points of fully diluted ownership — though lender-facing terms are often quoted as a percentage of loan principal, which lands between 1–5%.

This is a reason to model the fully diluted warrant impact against the cost of equivalent equity capital before taking on a venture debt facility. Sometimes the trade is clearly correct — debt buys runway to a higher valuation, making the warrant cost economically small. Sometimes the math favors raising equity at current terms instead. The decision requires explicit modeling, not a heuristic that debt is always cheaper than equity dilution.

On venture debt mechanics and when the trade works, Fiscallion has a detailed analysis in our venture debt for startups guide.

How liquidation preferences interact with dilution

Ownership percentage and economic outcome are not the same thing in a venture-backed company. Liquidation preferences can mean that a founder's 18% stake at exit produces far less than 18% of exit proceeds, depending on the structure of each preferred round.

1x non-participating preferred (standard)

Preferred investors receive either their liquidation preference (investment amount back) or their as-converted ownership percentage of the total proceeds — whichever is greater. In a strong exit above a certain threshold, preferred converts to common and everyone participates pro-rata.

Participating preferred (investor-favorable)

Preferred investors receive their liquidation preference first, then also participate pro-rata in the remaining proceeds as if converted to common stock. In a mid-range exit, this structure can leave founders with a much smaller slice than their ownership percentage implies.

Multiple liquidation preferences (uncommon in seed/A, more common in late-stage distress rounds)

A 2x or 3x liquidation preference means preferred must receive two or three times their investment before common stockholders see any proceeds. In a $150M exit for a company that raised $80M in preferred, a 2x preference means preferred investors receive $160M before common — there are no proceeds left.

This is why your dilution model needs to include a waterfall analysis at multiple exit scenarios, not just a cap table showing ownership percentages.

Evaluating liquidation terms as standalone concessions often blindsides founders to how severely cumulative preferences extract value from common equity.

Ownership percentages tell you one number. Exit proceeds at three different valuation scenarios tell you the actual trade-off you are making. 409A valuations and how they interact with liquidation preferences and option grants are covered in depth in Fiscallion's 409A valuation guide for startups.

The decisions that preserve founder ownership

Dilution is the cumulative result of specific decisions, most of which are negotiable before you sign.

1. Raise the right amount, not the maximum available

Every dollar of capital you raise beyond what the business needs in the next 18–24 months is dilution you accepted prematurely. Raise to a milestone that creates pricing power for the next round, not to a comfort threshold that feels safe.

The calculation is straightforward: identify the 2–3 metrics that will move your Series B valuation from X to Y, determine the capital required to reach them, add a 15–20% buffer for execution variance, and raise that number. Not more.

2. Manage your pre-money valuation aggressively

The pre-money valuation sets the price per share. A $15M pre-money and a $20M pre-money on the same $7M raise produce meaningfully different dilution outcomes.

Valuation is negotiable. It is set by investor appetite, your metrics, and the quality of your narrative. All three of those are workable variables.

3. Negotiate option pool timing and size separately from valuation

The option pool size is presented as a standard condition. It is not. The right pool size is the number of options you actually need to grant over the next 18 months of hiring, sized using your actual hiring plan with dilution modeled explicitly.

If your investor insists on 15–20% and you have modeled that 8% covers the next hire cycle, counter with 8% post-money and offer to revisit at Series B based on actual grant activity. Many investors will accept this.

4. Model three scenarios before every raise

Before opening a funding process, build three cap-table models: a bear case (lower valuation, higher dilution), a base case, and a bull case. For each scenario, calculate:

- Your post-round ownership percentage

- The estimated value of your stake at three exit valuations ($50M, $150M, $300M)

- The runway the capital provides at current burn and at 20% higher burn

This exercise surfaces the minimum acceptable pre-money valuation that keeps your ownership above a threshold you can commit to. It also prevents you from accepting a term sheet that looks acceptable in isolation but produces a poor outcome in context.

5. Consider whether venture debt can replace equity at specific moments

Venture debt is most valuable when you are six to nine months from a priced equity round and need runway to hit a pricing milestone without issuing equity at today's valuation. The debt is repaid, the warrant cost is modest, and you raise your next equity round at a higher valuation with less dilution.

This trade only works if you are highly confident in the milestone and timeline. If you are uncertain whether you will reach the milestone, debt adds a mandatory repayment obligation that constrains your options. Replacing a difficult equity conversation with debt is the wrong use of the instrument.

Common mistakes and the replacement moves

These are the five patterns that cost founders the most ownership and the replacement move for each.

Mistake 1: You model dilution only as "percentage given away in this round"

This single-round view misses SAFE conversions, warrant shares, and pool expansion that all happen at the same close. It produces an ownership estimate that does not match the actual post-close cap table.

Replacement move: Build a full dilution model that accounts for every share issuance event at the close: investor shares, SAFE/note conversion shares, new pool shares, and any warrant shares. Run it before you sign the term sheet.

Mistake 2: You agree to a pre-money option pool expansion without sizing it

Investors propose pool sizes based on what they want, not on what your hiring plan requires. Accepting a 20% pool expansion pre-money when your actual 18-month hiring plan requires 6% is a direct transfer of 14 percentage points of dilution from the investor to you.

Replacement move: Before each raise, build a hiring plan for the next 18–24 months with grant sizes per role. Sum the grants, add a 10–15% buffer, and that is your option pool request. Present it during term sheet negotiation with the underlying model.

Mistake 3: You treat anti-dilution provisions as protection for your shares

Most founders vaguely assume anti-dilution clauses protect them in a down round. They protect preferred investors, not common shareholders. In a down round, anti-dilution adjustments for preferred holders can generate additional share issuances that further dilute your common stock.

Replacement move: Your real anti-dilution protection is avoiding a down round. That means building runway models that are conservative rather than optimistic, raising only when you can hit the milestone required for an up-round, and treating bridge notes as a red flag rather than a routine tool.

Mistake 4: You ignore the liquidation waterfall when evaluating dilution

A 20% ownership stake looks the same in every cap table view. Its actual value depends entirely on how much preferred capital sits above it in the liquidation stack and what the participation rights are. Two founders can each own 20% and see very different outcomes at a $100M exit depending on the preferred terms.

Replacement move: Build a basic waterfall model at three exit prices — $50M, $150M, $300M — for every round you close. Update it every time new preferred capital enters the stack. This is a one-hour spreadsheet exercise that reframes dilution from an abstract percentage to an actual dollar outcome. The 409A valuation process is closely tied to this — your 409A valuation guide for startups explains exactly how liquidation preference structures suppress common stock FMV and what that means for option strike prices.

Mistake 5: You conflate "non-dilutive" with "no dilution impact"

Revenue-based financing has no share issuance and no dilution. Venture debt principal has no share issuance but warrants do carry dilution. Convertible notes and SAFEs have no immediate share issuance but convert to shares at the next priced round. "Non-dilutive" is almost always incomplete shorthand.

Failing to look past the marketing terms of facility agreements can lead to severe cap table reconciliation shocks down the line.

Replacement move: For every financing instrument, model the fully diluted impact including all conditions, conversions, and attached instruments. The question is not whether new shares are issued today — it is how many shares exist at exit and who owns them.

A pre-raise dilution checklist

The dilution events that do the most damage accumulate between term sheets, without a model running underneath them. This checklist helps close that gap before you open a fundraising process.

Cap table accuracy

- Confirm your current fully diluted share count, including all outstanding SAFEs, convertible notes, options granted, options available to grant, and any warrants

- Identify the conversion terms (caps, discounts, most-favored-nation clauses) for all outstanding SAFEs and notes

- Confirm the 409A FMV is current and within 12 months — see Fiscallion's 409A valuation guide for startups for the compliance clock and what triggers an early refresh

Pre-money modeling

- Build three pre-money valuation scenarios (bear / base / bull)

- For each scenario, calculate post-round fully diluted ownership for all current and new shareholders

- Calculate what your stake is worth at three exit valuations under each scenario

Option pool

- Build a 18–24 month hiring plan with role-level grant estimates

- Calculate the option pool size needed to cover that plan + 15% buffer

- Determine whether pool expansion should be pre- or post-money and why

Term sheet review

- Verify the liquidation preference structure (1x non-participating is baseline acceptable; anything else requires explicit modeling of exit scenarios)

- Identify any anti-dilution provision type (broad-based weighted average is standard; narrow-based or full ratchet requires pushback — NVCA model documents define the market baseline)

- Model the impact of any attached warrants or board seat provisions on your cap table

Post-close

- Update the cap table immediately upon close with all actual share issuances

- Project forward to the next round with updated ownership percentages and exit scenarios

Dilution is a decision

Equity dilution is not something that happens to your cap table. It is a series of decisions you make — or fail to make explicitly — across every financing event from incorporation to exit.

The founders who retain the most meaningful ownership through Series C are not necessarily the ones who raised the least capital. They are the ones who modeled the cumulative dilution path before each raise, negotiated option pool timing and size with a hiring model, and understood that their ownership percentage only matters as a percentage of a specific waterfall at a specific exit price.

The single most valuable FP&A exercise ahead of any fundraise is building the three-scenario cap table model before you open the process. Not after you receive term sheets, when you are negotiating under time pressure. Before, when you still have the information and the time to set your minimum acceptable valuation.

If you want to build that model together — combining your actual cap table, hiring plan, and burn rate into a dilution-aware fundraising framework — book a working session with Fiscallion.