Issuing stock options without a current 409A valuation is not a timing risk you manage—it is a tax liability you transfer to your employees. That distinction matters, because the penalties do not land on the company. They land on the people you hired.

Section 409A of the Internal Revenue Code sets the rules for nonqualified deferred compensation, and discounted stock options fall squarely inside those rules. Grant options at a strike price below fair market value (FMV), and each affected employee owes ordinary income tax on the spread at vest, plus a 20% federal excise tax, plus potential state penalties. There is no administrative fix after the fact.

This guide covers how a 409A valuation works, what drives the FMV output at each stage of growth, how it connects to your cap table and FP&A model, and where founders most often get it wrong.

What you'll learn

- What a 409A valuation is and why the IRS requires one before granting options

- Which valuation methods apply at which funding stage — and what inputs matter most

- What common stock FMV benchmarks look like from pre-seed through Series C

- How your cap table structure directly determines your option strike price

- The six compliance mistakes that create the most downstream exposure

- A pre-409A checklist for founders and operators preparing for the next engagement

What a 409A valuation is and what it actually determines

A 409A valuation is an independent appraisal of the fair market value of a private company's common stock. Its primary purpose is to establish the legally defensible strike price for employee stock options.

For public companies, FMV is the market price. For private companies, there is no observable price. The IRS mandates that option exercise prices equal or exceed common stock FMV on the grant date. A 409A valuation is how you prove that.

Three things a 409A valuation produces:

- A per-share FMV for common stock — the floor below which you cannot set option strike prices

- A dated, documented analysis that satisfies the IRS safe harbor standard when done by a qualified independent appraiser

- A 12-month compliance window during which grants made at or above that FMV are presumptively valid

What a 409A does not do: it does not tell you what your preferred investors paid, and it is not meant to. Common stock and preferred stock are different instruments with different economic rights. The gap between them is structural and expected.

Why this sits in your FP&A model, not just your legal files

Most founders treat the 409A as a compliance checkbox — something legal handles, filed somewhere, renewed annually. That framing is incomplete.

Your 409A valuation directly affects three financial planning variables:

- Stock-based compensation expense (ASC 718): The FMV from your 409A is the input to your Black-Scholes option pricing model, which determines the compensation expense you book on your income statement. A higher FMV means higher expense. If your FP&A model does not reflect the current 409A, your personnel cost projections are wrong.

- Option pool economics: The strike price affects whether employees will exercise, which affects dilution timing and cap table composition going into your next round.

- Investor due diligence: In any Series B, C, or acquisition process, investors will review your option grant history and compare dates and prices against your 409A valuation log. Gaps are red flags.

This is finance governance, not just legal compliance.

How the valuation is performed: methods and inputs

An independent appraiser selects from three core valuation approaches based on your company's stage and financial profile. Most engagements use a combination. The AICPA's practice guide on valuation of privately held company equity securities is the authoritative reference appraisers use when selecting and applying these methods.

The three valuation approaches

For SaaS companies between Series A and Series C, the market approach — often anchored by ARR multiples of comparable public software companies — is typically the primary method. The income approach may be layered in as revenue becomes predictable.

The backsolve method: the most common anchor at Series A

For venture-backed companies that have recently closed a priced round, the most common enterprise value anchor is the backsolve. The appraiser starts with the price paid by investors in the most recent round - which is observable and arm's-length — and works backward to infer the total enterprise value that is consistent with that preferred stock price. The option pricing model (OPM) then allocates that enterprise value across all share classes.

The backsolve is powerful because it grounds the valuation in a real transaction. It is also why your 409A must be updated after every priced round: the old enterprise value anchor is invalidated the moment a new one exists.

Equity allocation: OPM and PWERM

Once enterprise value is established, the appraiser must distribute it across share classes. Two models dominate:

Option Pricing Model (OPM): Treats each equity class as a call option on company value. Models the full distribution of exit outcomes using a Black-Scholes framework. Best for early-stage companies where exit timing and value are uncertain.

Probability-Weighted Expected Return Method (PWERM): Models discrete, named exit scenarios — IPO, acquisition, continued private operation, dissolution — each with an assigned probability and projected exit value. More appropriate at Series B and beyond, where a credible exit timeline is visible.

At Series C and pre-IPO, the PWERM or a hybrid OPM-PWERM approach becomes standard because specific exit scenarios carry real probability weight.

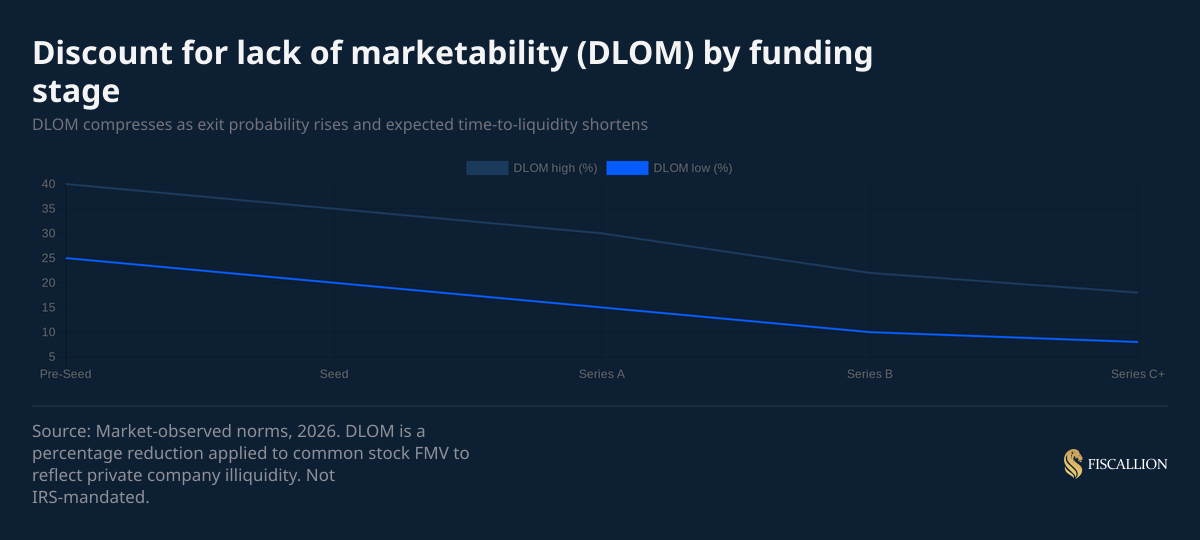

DLOM: the discount that most founders underestimate

After allocating enterprise value to common stock using OPM or PWERM, the appraiser applies a Discount for Lack of Marketability. DLOM reflects the fact that private company shares cannot be freely sold. A holder of common stock cannot simply exit. That illiquidity has value, and the discount reduces the common stock FMV accordingly.

DLOM is not arbitrary. It is derived from restricted stock studies, option-based models, or quantitative methods such as the Quantitative Marketability Discount Model (QMDM). It varies by funding stage, industry, and expected time to liquidity.

As the chart shows, DLOM compresses steadily as companies mature. Pre-seed companies — where time-to-liquidity is uncertain and long — face DLOM in the 25%-40% range. Series C companies approaching a credible exit face DLOM of 8%-18%. That compression is not cosmetic: it directly raises the common stock FMV and therefore increases option strike prices for new grants.

Benchmarks by stage: what a normal 409A result looks like

Founders frequently ask whether their valuation result is reasonable. The honest answer is that there is no single correct number — but there are observable market ranges.

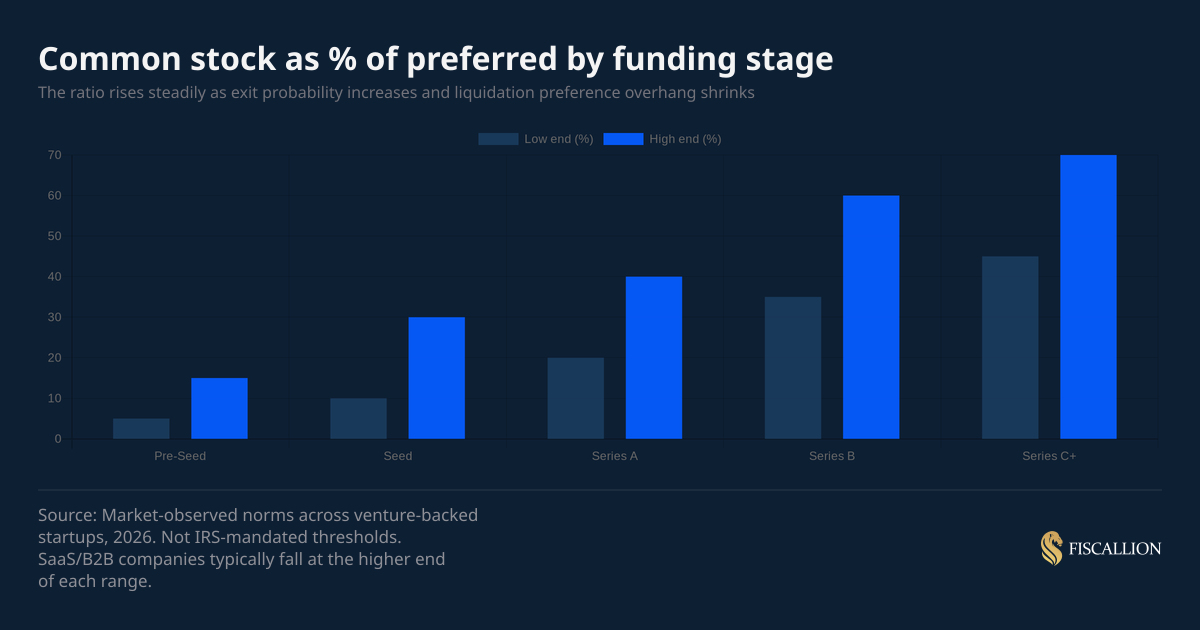

The most useful benchmark is common stock FMV as a percentage of the most recent preferred share price. This ratio is sometimes called the common/preferred ratio. It rises at each stage because liquidation preference overhang shrinks as exit probability increases.

Stage-by-stage benchmark table

These are market-observed norms, not IRS-mandated thresholds. A valuation that falls outside these ranges is not automatically wrong — it may accurately reflect your capital structure, recent performance, or exit timeline.

SaaS companies typically sit at the upper end of each range

For B2B SaaS, ARR is recurring, revenue multiples are well-established, and comparable public companies are abundant. That predictability supports higher common stock ratios relative to preferred. At Series A, a SaaS 409A commonly produces a common/preferred ratio of 25%-42%. At Series B, 40%-62%.

If your result is notably below the lower bound for your stage and industry, ask your appraiser which assumptions are driving it. The three most common explanations are: participating preferred with a high liquidation multiple, a large preference overhang relative to enterprise value, or poor recent financial performance that shifts probability weight toward downside scenarios.

The safe harbor standard: what it means and why it matters

Safe harbor means the IRS presumes your valuation is reasonable. That presumption shifts the burden of proof — if the IRS challenges your option pricing, they must disprove your valuation, rather than you having to prove it.

Three methods qualify for safe harbor under Section 409A regulations (Treas. Reg. § 1.409A-1(b)(5)(iv)):

- Independent appraisal — the standard path. Hire a qualified valuation firm, get a report, use it for grants within 12 months of the valuation date.

- Illiquid startup method — for companies under 10 years old with no imminent IPO or change of control. Allows an internal valuation by someone with relevant expertise, documented in writing. Rarely used beyond seed stage.

- Non-lapse restriction method — formula-based pricing via binding buy/sell agreements. Not applicable to most startups.

For any company past the early seed stage, option 1 is the right answer. The cost of a qualified independent appraisal - typically $1,000-$5,000 for most Series A companies - is a fraction of the tax exposure a non-compliant grant creates.

The 12-month clock

A 409A valuation is valid for 12 months from the valuation date, or until a material event occurs, whichever comes first. After the clock runs out, safe harbor is lost. Any grants made on an expired valuation are out of safe harbor, even if no material event occurred.

Mark your valuation expiry date. Treat it with the same seriousness as your Delaware franchise tax or SOC 2 renewal.

What triggers a new valuation before the 12-month window closes

The 12-month maximum assumes no material changes. In practice, companies at the Series A-C stage often need more frequent updates. The clearest triggers:

The post-round update is the one most commonly missed. Companies close a Series B, grant options to the new hires funded by that capital, and fail to update the 409A first. That grant is out of safe harbor from the date the round closed.

How your cap table determines your option strike price

The cap table is the primary input to the equity allocation waterfall. Every structural choice you made across your financing history — liquidation preference terms, participation rights, option pool size, convertible instruments — flows directly into the per-share common stock FMV.

Liquidation preferences suppress common stock value at lower exit valuations

A 1x non-participating liquidation preference means preferred investors recover their capital in a sale, then convert to common for further upside. Common stock benefits from the full distribution above the preference threshold. This is the most founder-friendly structure.

A 1x participating preference is materially worse for common stockholders. Preferred investors recover their investment and participate pro-rata in remaining proceeds. In mid-range exit scenarios, this compresses common stock value significantly.

A 2x or 3x liquidation multiple means preferred must receive 2x or 3x invested capital before common receives anything. At lower exit valuations, common stock may receive nothing at all. That scenario weighting in the OPM directly reduces FMV.

If your cap table carries stacked preferences from multiple rounds, each with participation rights, do not be surprised when your 409A produces a common/preferred ratio toward the bottom of the benchmark range.

The option pool affects the fully diluted share count

Unissued option pool shares are typically included in the fully diluted share count. More shares distributed across the same enterprise value means lower per-share FMV. The effect is usually modest, but the more relevant issue is how the option pool interacts with the backsolve.

Investors frequently require an option pool expansion pre-close, which means that dilution falls on existing shareholders before the round. If the appraiser does not correctly account for whether the pool was included in the pre-money or post-money cap structure, the implied enterprise value will be wrong, and so will the common stock FMV.

SAFEs and convertible notes must be reflected accurately

Outstanding unconverted SAFEs or convertible notes are not yet equity, but they represent future equity claims. The appraiser must include the expected dilution from conversion in the fully diluted share count.

Post-money SAFEs define the investor's ownership percentage post-close, so the dilution falls on existing holders. That structure requires a different treatment in the backsolve model compared to pre-money SAFEs. If your cap table management software does not correctly distinguish between the two, the valuation inputs are wrong before the engagement even starts.

Common cap table errors that produce non-compliant strike prices:

- Missing or wrong liquidation preference terms

- SAFEs or notes not reflected in the fully diluted count

- Option pool expansion not entered after the most recent round

- Warrants issued to lenders or service providers omitted

- Outdated share counts not reconciled with corporate records

These are not edge cases. They show up regularly in due diligence, and they create compliance exposure that no amount of after-the-fact documentation resolves.

The FP&A implications your model cannot ignore

The 409A valuation does not live only in your legal folder. It has direct, material effects on your financial model.

ASC 718 stock-based compensation expense

Under ASC 718 (FASB Accounting Standards Codification Topic 718), you recognize the grant date fair value of stock options as a compensation expense over the vesting period. The grant date fair value is computed using Black-Scholes or a similar option pricing model, and the 409A FMV is the exercise price input.

A higher 409A FMV reduces the intrinsic value component of the option and affects the Black-Scholes output. The relationship is not linear — it also depends on volatility, expected term, and risk-free rate — but the direction is consistent: as your 409A FMV rises, the compensation expense per option grant typically changes, and your people costs on the income statement shift accordingly.

If you are modeling headcount plans 12-18 months out, you need a reasonable estimate of your next 409A FMV to forecast SBC expense accurately. That requires coordinating between your cap table, your FP&A model, and your legal team — not treating each as a separate workstream.

Runway model accuracy depends on accurate personnel costs

For companies between $5M and $50M ARR, SBC is often 5%-15% of total compensation expense when properly booked under ASC 718. If your runway model uses only cash payroll and excludes non-cash SBC, your burn rate is understated and your gross margin is overstated.

This is a specific manifestation of the broader problem we see repeatedly: implicit assumptions baked into financial models that nobody owns. Someone chose to exclude SBC. Nobody documented why. The board sees a runway number that does not match what an auditor or sophisticated investor would calculate.

Own the inputs. If SBC is excluded, that is a deliberate choice that should be disclosed, not a silent omission.

A company at $12M ARR was modeling runway off cash burn. Stock-based compensation — which under ASC 718 is a real income statement expense — was completely absent from the model. The founder's argument was that SBC isn't a cash expense, so it shouldn't affect runway. True for cash runway. But the same number was being used to communicate EBITDA margin to the board and to investors. Reported EBITDA margin was -8%. Adding back roughly $1.4M of annual SBC moved it to -19%.

The gap was caught during prep for a Series B. The lead investor's model would inevitably include SBC, and the company was about to walk into a meeting presenting one number while the investor was reading another. The board deck got rebuilt with two parallel views — cash burn and runway on one axis, EBITDA margin including SBC on the other.

The 409A and your fundraising model

Your 409A history will be reviewed in any institutional fundraising process. Investors and their counsel will compare grant dates and strike prices against your valuation log to confirm that options were not granted during periods when the valuation was expired or invalidated by a material event.

A clean 409A log — one where every grant batch is preceded by a current, defensible valuation — removes a diligence friction point that otherwise adds time and negotiating cost to a process you want to close cleanly. A clean 409A log — one where every grant batch is preceded by a current, defensible valuation — removes a diligence friction point that otherwise adds time and negotiating cost. The discipline pays in the transaction.

The six compliance mistakes that create real exposure

Most 409A failures follow one of six patterns. Each has a straightforward replacement behavior.

1. Granting options after a round closes without updating the valuation

The mistake: Closing a Series A in March, then granting options to the new hires you funded in April using the pre-round valuation from the previous October.

The replacement: Initiate the new 409A engagement in parallel with the round close process. Most reputable providers deliver in 2-3 weeks. Budget for it in the round planning, and do not make grants until the updated valuation is in hand.

2. Letting the 12-month window expire quietly

The mistake: The last valuation was dated in February of the prior year. New hires start in March of the current year, and the valuation expired without anyone noticing.

The replacement: Set a calendar reminder 45-60 days before expiration. Treat the 409A renewal as a standard annual compliance item with an owner, a deadline, and a budget line.

3. Choosing a provider on price alone

The mistake: Using the cheapest automated tool because the company is frugal.

The replacement: Choose a provider with credentials (CFA, ASA), startup-relevant experience, and a methodology that passes Big Four audit scrutiny. A $500 savings on the valuation fee can produce a $50,000 problem if the report is rejected by your auditor and you have to redo it at a higher FMV — and reprice already-granted options.

4. Submitting a stale or incomplete cap table

The mistake: Sending the appraiser a spreadsheet cap table that has not been reconciled since the last round, with incomplete SAFE terms and missing warrants.

The replacement: Before initiating any 409A engagement, export a fully diluted cap table from a professional cap table management system (Carta, Pulley, or equivalent) and reconcile it against corporate records. Confirm liquidation preference terms, SAFE formats, and option pool size are all current.

5. Treating the 409A as a legal matter rather than a financial planning input

The mistake: Delegating the 409A entirely to legal counsel and never connecting the FMV output to the FP&A model, SBC forecasting, or board reporting.

The replacement: The operator or Head of Finance should review the 409A output before it is filed, understand what methodology was used, and confirm the resulting FMV is reflected in the compensation model. The board should know the current common stock FMV, not just the preferred price.

6. Backdating or manipulating grant dates

The mistake: Retroactively setting option grant dates to a prior date when the valuation was lower, to give employees cheaper options.

The replacement: Do not do this. It is fraud. Grant options on the date you intend to grant them, using the current valid valuation.

The first two mistakes above interact. A company that misses the post-round update and the 12-month renewal at the same time can run for nearly two years on an invalidated valuation, with every option grant in that window exposed.

A case from a Fiscallion engagement: a company at $14M ARR had been operating on a 409A from 22 months earlier. The valuation had expired at month 12, and they had closed a Series A at month 14 — definitively a material event. They kept issuing options at the original strike for another eight months. The exposure was roughly 47 grants, all priced below FMV at the time of grant.

Remediation required a corrective 409A backdated to capture the exposure period, plus Section 409A correction filings for the affected grants. Total cost — counsel, valuation firm, and grossing up affected employees — was a little over $180K.

Your 409A pre-engagement checklist

Run through this list before contacting any valuation provider. Every item you can check off reduces engagement time, cost, and the risk of inaccurate inputs.

Cap table data

- Fully diluted cap table exported from a professional platform (Carta, Pulley, or equivalent)

- All equity classes confirmed: common, each series of preferred, option pool (issued and unissued)

- Issued option grants entered with correct grant dates, exercise prices, share counts, and vesting schedules

- Outstanding SAFEs and convertible notes entered with principal, interest, valuation cap, discount rate, and format (pre-money vs. post-money)

- All warrants listed with exercise price, share quantity, and expiration date

- Cap table reconciled against stockholder registry and most recent board minutes

Preferred stock terms

- Liquidation preference type confirmed for each series (1x non-participating, 1x participating, 2x+)

- Participation caps (if any) documented

- Conversion ratios and anti-dilution provisions confirmed

Corporate documents

- Certificate of Incorporation (and all amendments) available

- Most recent financing term sheet or stock purchase agreement available

- Financial statements current (P&L, balance sheet)

- Financial projections prepared (at least 12-24 months)

- Latest board deck or company overview ready to share

Timing

- Confirm whether any material events have occurred since the last valuation

- Confirm no term sheets or LOIs are outstanding that could affect enterprise value

- Grant timing coordinated with legal counsel and the expected valuation delivery date

A clean engagement starts before you send the first email to the appraiser. The time you invest in preparation is returned directly as a faster turnaround and a more defensible report.

A note on the high vs. low valuation tradeoff

Founders sometimes try to influence their 409A toward a lower result, reasoning that lower strike prices make options more attractive to employees. That logic is incomplete.

A lower FMV does reduce the strike price — but only if the appraiser's analysis supports it. A result that cannot be defended by the methodology is not a lower valuation; it is a non-compliant one.

What you can do within the rules:

- Use a stock split to reduce the per-share price without changing ownership percentages. A 2-for-1 split halves the per-share FMV and makes options feel cheaper to candidates. This is cosmetic, legitimate, and widely used.

- Time grants before a round when the prior valuation is still valid. Options granted just before a Series B closing will carry the pre-round FMV, which is typically lower than the post-round refresh.

- Ask the appraiser to walk through the range. Defensible valuations often fall within a range rather than at a single point. Understand the inputs that drive the result toward the upper or lower end, and discuss whether those inputs reflect your actual business facts.

The goal is not the lowest possible number. The goal is the most accurate and defensible number, which happens to also protect your team.

Treat the 409A as financial governance, not paperwork

A 409A valuation is not a formality you delegate and forget. It is a financial governance decision that affects your employees' tax treatment, your FP&A model accuracy, your fundraising due diligence, and your board's understanding of your equity structure.

The decisions worth owning here are straightforward: engage a qualified independent appraiser before granting any options, update the valuation after every priced round and at least annually, maintain a clean cap table as the input, and connect the resulting FMV to your compensation model and runway projections.

The founders who get this wrong are not usually careless. They are treating the 409A as a checkbox rather than as a financial input with downstream consequences. The fix is not adding more process — it is making sure someone with FP&A ownership understands what the valuation produces, what it drives, and when it needs to change.

At Fiscallion, we work with founders at Series A through Series C who are navigating exactly these financial governance questions — connecting the equity structure to the operating model so that decisions about headcount, capital allocation, and investor reporting are made with the full picture in view. If you are preparing for a new round or managing your first post-round 409A cycle, that is a good moment to get the model right.

Audit your equity compensation model and financial assumptions. If your FP&A model does not reflect your current 409A FMV — or if you are unsure whether your cap table is clean enough to support a defensible valuation — that is the right place to start.