Most founders approach venture debt as a backup plan - something to think about when the equity round stalls or runway gets tight. That is exactly backwards. The best time to negotiate venture debt is immediately after closing an equity round, when your leverage is highest and lenders are most willing to commit. By the time you need it urgently, the terms have already gotten worse.

This article explains how venture debt works mechanically, what the all-in cost actually looks like when you model it properly, and the decision framework for figuring out whether it makes sense for your company right now — or not at all.

Key takeaways

- Venture debt typically sizes at 20-35% of your last equity round and costs 8-15% annually in interest, plus upfront fees, an end-of-term fee, and a small equity kicker via warrants.

- The dilution comparison is only meaningful if you model the warrant cost at your expected exit valuation — not at face value.

- Venture debt is not a rescue instrument. It extends runway for companies already on a clear path to the next round; it does not create that path.

What venture debt is (and what it is not)

Venture debt is a term loan or revolving credit facility offered to VC-backed growth-stage companies as a complement to equity financing. It is non-dilutive in the sense that it does not require issuing new shares - though warrants typically attach a small equity kicker that creates dilution at exit.

The key distinction from a traditional bank loan: lenders do not underwrite based on your profitability or hard assets. They underwrite based on the quality of your existing investors, the size of your most recent round, and the plausibility that you will raise another equity round to repay them. That last point is the structural assumption the entire market rests on.

Venture debt follows venture capital. It does not replace it.

If you do not have institutional VC backing or a credible path to profitability, most venture debt lenders will not give you a term sheet. The instrument is specifically designed for companies that have already proven enough to raise equity - and now want to extend runway without resetting valuation.

How it differs from other non-dilutive financing

Revenue-based financing from providers like Capchase is often faster and simpler for SaaS companies with predictable ARR below $5M. Venture debt makes more sense once you are post-Series A and the deal size justifies the legal overhead.

How venture debt is structured

Most venture debt deals share the same basic anatomy. Understanding each component is how you avoid signing a term sheet that looks cheap on the interest rate line and expensive everywhere else.

The loan principal and sizing

The standard sizing rule is 25-35% of your most recent equity round. If you raised a $12M Series A, you can typically access $3M-$4.2M in venture debt.

Some lenders will alternatively size against ARR — typically 30-50% of ARR. So at $6M ARR, the ceiling might be $2M-$3M from that metric. Lenders use whichever produces the lower number as a risk control.

Interest rate: variable, not fixed

Venture debt is priced as a floating rate: a benchmark (usually SOFR) plus a spread. According to the Federal Reserve's SOFR data, rates have moderated from their 2023 peak:

- SOFR as of early 2026: approximately 3.7-4.3%

- Typical spread for growth-stage SaaS: 6-9%

- All-in rate range: 10-13.5% APR for most deals

Riskier profiles (short runway, high burn, weak unit economics) will see rates above 15%. Stronger profiles with tight unit economics, tier-1 VC backing, and 18+ months runway can negotiate closer to 9-10% all-in.

The interest-only period

Most facilities begin with 6-18 months of interest-only payments before the principal amortization schedule starts. This is what gives you the runway extension benefit - your monthly cash outflow during the IO period is just the interest cost.

On a $3M loan at 11% APR, the IO period payment is $27,500/month. That is a meaningful but manageable drag on burn for a company at $5M+ ARR.

Warrants: the equity kicker

Lenders take a warrant — the right to buy shares at your last round's price per share - as compensation for taking on startup risk without equity upside. As a16z notes in their guide to raising debt, typical warrant coverage on term loans runs 20-100 basis points of fully diluted share ownership — though coverage expressed as a percentage of loan principal (the more common founder-facing convention) typically lands between 1-5%.

On a $3M loan at 2% warrant coverage, the lender receives warrants worth $60,000 at your current share price. The real cost of those warrants is only knowable at exit - if you exit at 5x your current valuation, those warrants are worth $300,000.

Model warrant cost at 2-3x and at 5x your current valuation before you sign. The difference is significant.

Fees

Three fee buckets matter:

- Upfront fee: 1-2% of the loan, paid at closing. On $3M, that is $30,000-$60,000.

- End-of-term (or success) fee: 3-6% of the loan, paid when the loan matures or is repaid. On $3M, that is $90,000-$180,000.

- Prepayment penalty: 1-3% if you repay early, usually waived after 6-12 months.

The end-of-term fee is the one founders most often undercount. Include it when modeling the total cost of the facility.

Covenants: the hidden risk

Covenants are contractual conditions. Breaching them constitutes a technical default, which gives the lender the right to demand full immediate repayment.

The minimum cash covenant is the one that catches founders off guard most often. You sign a deal requiring a $2M minimum cash balance while burning $600K/month. Eight months later you are at $2.3M and the covenant is four weeks from triggering — and nobody modeled that scenario before signing.

The fix: run a monthly covenant compliance model. Set an internal yellow flag at 120% of the covenant threshold. If the covenant says $2M minimum cash, your internal alarm should go off at $2.4M.

What happens in practice when that alarm goes off is different from what the loan documents describe.

A case from a Fiscallion engagement: a company that had taken on $4M of venture debt with a $2M minimum cash covenant. The early signal was projected month-end cash for the following month dropping to $2.3M — within $300K of the covenant. The founder hadn't flagged it because technically they were still in compliance.

What the lender did in practice was different from what the documents implied. The documents said breach would trigger a default and potentially acceleration. When we proactively reached out at the $2.3M projection, the lender wanted a weekly cash update, a revised forecast, and a written plan to maintain the covenant. They didn't accelerate. They didn't threaten to. But the soft pressure was significant — every operating decision for the next two quarters was effectively reviewed against the covenant.

To stay safely above the threshold, the founder pulled in AR through factoring at unfavorable terms — paying roughly 4% of AR value to accelerate collection by 30 days. Month-end cash moved to $2.7M.

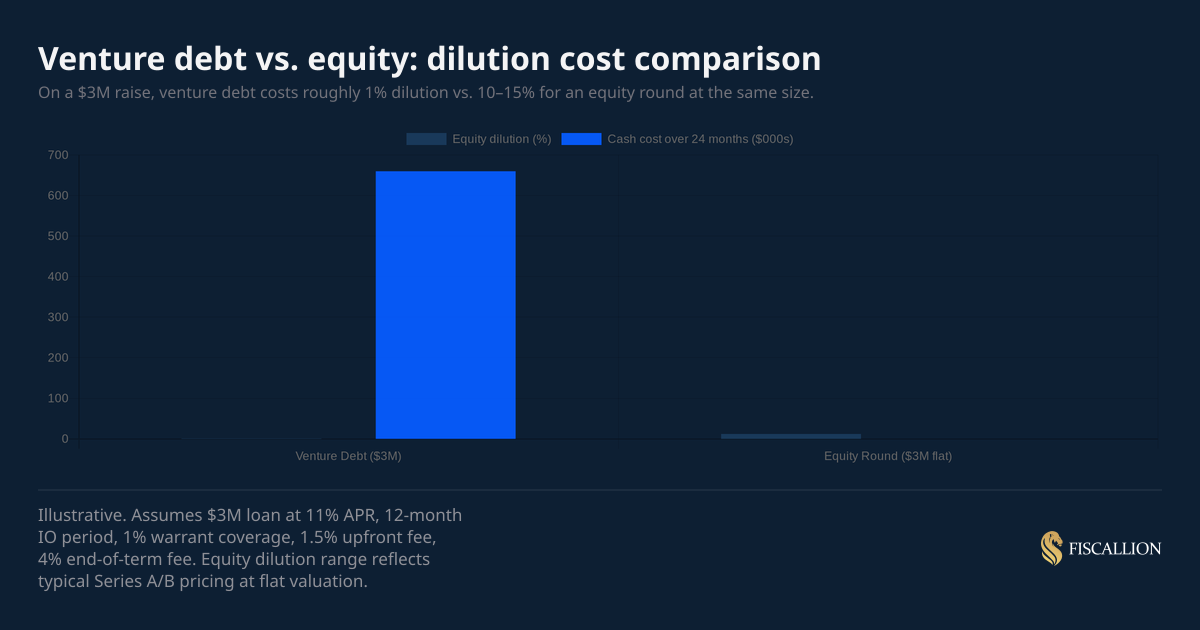

The true cost model: a $3M example

The interest rate headline is not the cost of venture debt. Here is the full 24-month picture on a $3M facility at 11% APR:

All-in cash cost: approximately $660,000 over 24 months on a $3M loan. That is a 22% effective cost when you include fees.

Compare that to raising the same $3M in a flat equity round at your current valuation: roughly 8-12% dilution. If your company is worth $30M today, that 10% dilution represents $3M in equity value given away permanently.

The debt is cheaper in most scenarios where you have a credible path to raising your next round at a materially higher valuation. The debt is not cheaper if you burn the proceeds with no milestone attached and the next round stalls.

When venture debt makes sense - and when it does not

The framing most founders use — "does venture debt make sense for us?" - is less useful than the more specific question: "does taking on $X in debt, at this cost, to hit this specific milestone, in this timeframe, produce a better outcome than the alternative?"

The case for venture debt: four scenarios worth modeling

1. Runway bridge to a milestone inflection

You are 6-7 months from hitting the ARR number that justifies a materially higher Series B valuation, but only have 4 months of cash. Debt bridges that gap without forcing a flat or down round. This is the most common and most defensible use case. Understanding your startup runway calculation in detail - not just a rough cash/burn estimate - is what makes this case buildable before you approach a lender.

2. Avoiding a valuation reset

You could raise equity now, but your metrics are not yet where you want them to be. Taking on $2-3M in debt to buy 5-6 months of runway - and then raising equity when the numbers justify the valuation you want — saves significant dilution.

3. Non-dilutive CAPEX or infrastructure investment

You need servers, equipment, or infrastructure that generates clear ROI over 2-3 years. Debt financing tied to a specific asset with identifiable return is a sensible structure.

4. Working capital smoothing for enterprise SaaS

Enterprise contracts with annual prepayment create large cash flow swings. A revolving credit line addresses seasonality without requiring an equity round.

When not to use venture debt

- Less than 6 months of runway with no clear path to next round. Debt accelerates insolvency for companies that cannot service it.

- Pre-product-market fit. Lenders will not underwrite it, and you should not take on fixed obligations before your model is proven.

- Burn rate accelerating beyond plan. Adding $30-50K/month in interest payments to an already deteriorating burn trajectory makes a bad situation worse.

- Deploying it as general working capital with no milestone attached. "Good to have extra cash" is not a use case. Every dollar of debt should be tied to a specific output - "$3M extends runway to $5M ARR, which supports a $30M Series B" is a plan. "General operations" is not.

- Debt already above 50% of your last round. At that leverage ratio, future equity investors will discount your company's clean balance sheet story.

What lenders actually evaluate

Venture debt underwriting does not work the way equity underwriting does. Investors bet on your ceiling. Lenders bet on your floor — specifically, whether you will raise another round to repay them. As a16z's debt-raising guide puts it: lenders are primarily underwriting to future equity funding, not to your current profitability.

The metrics that drive your rate and approval:

Investor quality: having Tier 1 VCs on your cap table who recently invested is the single biggest signal lenders use. It tells them the next round is plausible.

Runway post-loan: most lenders want to see 12+ months of runway after the loan closes. This gives you time to raise the next round before the amortization schedule creates pressure.

ARR and growth rate: predictable, growing ARR reduces lender risk. Sub-$2M ARR will limit your options significantly. Above $5M ARR with 80%+ gross margin is where most lenders become genuinely competitive for your business.

Burn multiple: lenders evaluate how many dollars you burn per dollar of new ARR. David Sacks, who originated the burn multiple metric, defines it as: Net Burn ÷ Net New ARR. A burn multiple below 1.5x signals capital efficiency. Above 2.5x raises concerns about your path to repayment. This is the same lens your next equity investor will use, which is why lenders have adopted it as a primary screen.

Customer concentration: if one customer represents 30%+ of your ARR, that is a red flag. It puts the lender's security interest at the mercy of one renewal decision.

Gross margins: SaaS gross margins above 70-75% indicate the business model works. Below 60%, lenders will probe whether you have the capacity to service debt through a growth slowdown. Understanding your SaaS unit economics - specifically gross margin by cohort, not just blended - is what lets you defend this number when a lender pushes on it.

How to prepare your materials before approaching lenders

Do not approach lenders cold with a pitch deck. Lenders want a financial story, not a vision story.

According to a16z's execution guide, corporate debt typically closes in 4-6 weeks from introductory call to closing — but that timeline assumes your materials are already ready before you start outreach. Companies that run into delays almost always trace them back to missing or inconsistent financial documentation.

The materials you need:

- Three-year financial model with monthly granularity for Year 1. It must include a runway waterfall, a burn rate trend, and an ARR bridge. If you do not have this model built, building it is the prerequisite - not the lender conversation. Our SaaS financial model guide covers the architecture in detail.

- ARR breakdown: revenue by customer segment, cohort retention, and contract length. Lenders want to see that the ARR is sticky.

- Cap table and most recent term sheet: the loan sizing is anchored to your last round. Have the documentation ready.

- Six months of bank statements: lenders verify your actual cash position and spending patterns against your model. Discrepancies between your model and bank statements will kill a deal.

- Board deck (latest version): lenders will ask about this or want to reference it. Your board materials should already tell the capital allocation story - if they do not, that is a separate problem worth fixing first. Our SaaS board reporting framework covers what decision-ready board materials actually look like.

- Covenant sensitivity model: before you even see a term sheet, build a model showing what happens to your cash balance and ARR under your base case, a 20% revenue miss, and a 40% revenue miss. Know in advance which covenants you can accept and which ones create too much downside risk.

The Fiscallion fundraising and investor support service is built around exactly this kind of preparation — making sure your financial model, ARR documentation, and investor materials all tell a consistent story before you sit across from a lender.

Negotiating the term sheet: five variables that matter

Most founders negotiate the interest rate and forget everything else. In practice, the rate is often the least negotiable term once a lender has underwritten you. These five items are more negotiable and more consequential:

1. Warrant coverage percentage: push for 1% or below. Anything above 2% starts to add up at exit. If a lender insists on 3-5%, model the warrant dilution at your expected exit multiple before accepting.

2. End-of-term fee: negotiate this down from 4-5% to 2-3% if you have competing term sheets. It is a large lump sum that founders often overlook during negotiation.

3. Covenant structure: push to replace financial covenants (minimum ARR, minimum cash) with reporting covenants wherever possible. Reporting covenants - deliver financials monthly, notify of material changes - give you obligations without a hair-trigger default. Financial covenants create risk in scenarios you cannot fully predict.

4. Draw structure: if the facility allows tranche draws over 6-12 months, do not draw the full amount at close unless you need it. Interest starts accruing on drawn capital immediately. Drawing in stages reduces your interest cost.

5. Prepayment penalty: try to cap this at 1% or negotiate for it to expire after 12 months. If you raise your next equity round ahead of schedule, you want to be able to retire the debt without significant penalty.

Having 3-5 competing term sheets is the most effective way to negotiate on any of these terms. Your lead VC's existing relationships are the fastest way to get warm introductions to multiple lenders simultaneously.

The decision framework: four questions before you sign

Before signing any venture debt term sheet, you should be able to answer all four of these questions clearly:

- What specific milestone does this capital fund, and how long will it take to reach it? "Six months to $5M ARR" is an answer. "General growth" is not.

- What does the all-in cost look like at my expected valuation at the next round? Model the interest, fees, and warrant dilution at 2x, 3x, and 5x your current valuation. At what multiple does equity become cheaper?

- Which covenants in the term sheet could I breach in my downside scenario? Run the 40% revenue miss model and check every financial covenant. If a covenant triggers in that scenario, negotiate to soften it or remove it.

- Who owns the monthly covenant compliance review? This needs a named owner with a standing monthly calendar item. If the answer is "someone will check on it when it comes up," you are setting yourself up for an avoidable default.

If you cannot answer all four questions before signing, the preparation work is not done yet. The decision framework is not about being conservative — it is about making sure you are taking on known, modeled risk rather than implicit, unmeasured risk.

The framework is most useful when the headline terms look attractive. Those are exactly the moments when downside scenarios get skipped.

A case from a Fiscallion engagement: a company at $6M ARR with a Series A in the bank wanted a Series B in 18 months. The pitch from the lender was attractive — $5M facility, 8.5% interest, 24-month draw period. The founder saw it as a way to extend runway without further dilution.

I advised against it. The milestone clarity wasn't there. The Series B raise was contingent on hitting roughly $14M ARR, and the path to that target depended on a sales motion that hadn't been proven at scale. Venture debt magnifies the consequences of missing milestones. Hit the target, the debt is fine. Miss by 20%, you're raising a Series B with $5M of debt on the balance sheet — which either compresses valuation significantly or forces the new investor to refinance the debt as a condition of the round.

The founder pushed back. Their argument was that debt is always cheaper than equity at any reasonable valuation. True per-dollar, but it ignores the optionality cost. We modeled three scenarios — hit milestone, miss by 20%, miss by 40%. The value destruction in the miss scenarios was significant enough that the founder passed.

Over the next 12 months, they hit roughly 75% of the target. Series B took an extra quarter and closed at a flat valuation. Without the debt on the balance sheet, the conversation was about a flat round. With it, the conversation would have been substantially harder.

The five most common venture debt mistakes

Mistake 1: Taking debt when you need equity

Debt at 25-35% of your last round is a complement to equity, not a substitute. If you need capital equivalent to a full new round, raise the round. Taking on debt to avoid a difficult equity conversation delays the problem and adds mandatory repayment pressure.

Replacement move: use debt to extend runway to a milestone that justifies higher valuation at the next equity round.

Mistake 2: Not modeling covenant risk

Signing a term sheet with a $2M minimum cash covenant and a $700K/month burn rate without mapping out when that covenant will trigger is a planning failure. The lender is not responsible for warning you.

Replacement move: build a monthly covenant compliance model before you sign. If a covenant triggers in your downside scenario, negotiate to remove or relax it before closing.

Mistake 3: Treating warrant dilution as immaterial

"It's only 1.5% of the loan amount" — that is the face value of the warrants at your current price. At a 5x exit, those same warrants represent 5x the value in real dilution. Founders consistently undercount this.

Replacement move: model warrant dilution at your expected exit valuation, not at the loan's face value.

Mistake 4: Drawing the full facility at close

Drawing $3M at close when you need $1M in the next six months means paying interest on $3M starting day one. That is the equivalent of pre-paying $100,000+ in interest for capital you have not yet deployed.

Replacement move: negotiate a draw schedule and take capital in tranches aligned to your actual spending timeline.

Mistake 5: No specific deployment plan

"It adds to our cash cushion" is not a deployment plan. Debt has a fixed monthly cost and a repayment schedule. If the capital is not generating a return — through faster hiring, a faster sales cycle, or a specific product milestone — you are paying for nothing.

Replacement move: define the exact use of proceeds, the milestone it funds, and the timeline before closing. That document also becomes part of your next board update.

Practical checklist: before you start the lender conversation

Use this checklist to assess readiness before approaching any lender. If you cannot check every item, address the gap first.

Qualifications

- Series A closed within the last 18 months

- Institutional VC backing (not angels alone)

- ARR above $1M (ideally $3M+)

- 12+ months of post-loan runway in your base case model

- Gross margins above 65%

- Burn multiple below 2.0x

Model readiness

- Three-year financial model with monthly Year 1 detail

- Runway waterfall built and current

- ARR bridge with net retention and expansion components

- Covenant sensitivity analysis (base, -20%, -40% scenarios)

- Warrant dilution modeled at 2x, 3x, and 5x current valuation

Materials

- Cap table current and clean

- Most recent board deck available

- Six months of bank statements organized

- ARR breakdown by customer segment and contract tenure

Negotiation prep

- 3-5 lender targets identified (not one)

- VC intros to lenders requested

- End-of-term fee modeled and included in total cost

- Covenant language reviewed by counsel before signing

The goal is not to rush to a term sheet. The goal is to walk into the first lender conversation with a clear answer to why you want this capital, what it funds, and how you will service it — so the conversation is about terms, not viability.

If your financial model, runway forecast, or ARR documentation is not yet decision-ready, that is the right problem to fix first. Fiscallion's fractional CFO and FP&A support is specifically structured to get companies from "our model exists somewhere" to "our model tells a clear story about capital, runway, and trade-offs" — which is the prerequisite for any serious lender conversation.

Treat the decision as a modeling problem before a fundraising one

Venture debt is a precision instrument. It works well in a narrow set of conditions: post-Series A, VC-backed, with a specific milestone inside a realistic timeline, where the cost of dilution from a flat equity round exceeds the all-in cost of the debt.

It fails when it is used as a safety net, a substitute for hard equity conversations, or a way to fund runway without a clear path to repayment. The instrument does not save struggling companies — it extends runway for companies already on a clear trajectory.

The decision to take on venture debt is a financial modeling problem before it is a fundraising problem. Know the all-in cost, model the covenant risk, and define the deployment plan before you talk to a single lender.

If you want help building the financial model that makes that conversation possible - runway forecast, ARR bridge, unit economics, and covenant sensitivity — book a working session with the Fiscallion team.