Bookkeeping tells you where your money went; FP&A tells you where your runway is going. For a SaaS company burning cash between $5M and $50M ARR, confusing clean accounting with strategic financial planning is a fatal mistake. You don’t need more detailed line items; you need a reliable operational cadence that translates raw actuals into immediate capital allocation choices.

This article explains what a functional FP&A system looks like at the startup stage, how to build one without a full finance team, and where most companies between Series A and Series C break down.

What you'll learn

- The exact difference between a financial model and an FP&A function - and why confusing them is expensive

- The five core FP&A outputs that matter at $5–50M ARR, from runway to CAC payback

- How to run a decision-grade monthly cadence with as few as two people

- The most common FP&A failure modes at this stage, and what to do instead

What FP&A actually means for a startup

Financial planning and analysis (FP&A) is the practice of building forward-looking financial views, comparing them to actuals, and using the gap to make better resource allocation decisions.

Bookkeeping tells you where the money went. FP&A tells you what you can afford next, and when. The difference matters most when your decisions are burning cash at speed.

At the startup stage, FP&A sits at the intersection of four problems most founders are already fighting:

FP&A is not a department you build. At $5M–$25M ARR, it's a system - a model, a cadence, and a clear owner of the assumptions.

Why most startups don't have real FP&A yet

The gap is almost never ambition. It's architecture.

Here's what typically exists at a $10M ARR SaaS company before they put a proper FP&A system in place:

- A financial model built for the last fundraise, now 14 months out of date

- A bookkeeper or controller closing the month in QuickBooks

- A spreadsheet someone pulls actuals into manually before board meetings

- A deck that shows revenue, ARR growth, and burn - but not what the business should do next

This setup gets companies to $5M–$10M ARR. It stops working somewhere between Series A and Series B when the number of decisions per month - hiring, pricing, channel allocation, contract terms - exceeds what a founder can hold in their head.

The trigger is usually one of these: metrics chaos before a board meeting, an unexpected cash crunch, or a fundraise where an investor asks a question about unit economics that takes three days to answer.

The five outputs FP&A must produce at the startup stage

Not all FP&A is equal. At $5–50M ARR, these are the five outputs that drive decisions. Everything else is reporting for reporting's sake.

1. Runway with scenario splits

Runway is not a single number. It's a range across your base, upside, and downside assumptions.

A useful runway output answers: "Under what conditions do we have 18 months of cash? Under what conditions do we have 9?"

As a16z's framework for navigating down markets makes clear, raising capital with less than 12 months of runway sends a negative signal to investors and weakens your negotiating position — making runway visibility a fundraising input, not just an operational one.

The inputs that most change runway answers at this stage:

- Net revenue retention (do existing customers expand or contract?)

- New logo growth rate (and what's the range of outcomes from the current pipeline?)

- Headcount additions by quarter

- Collections timing if you invoice annually

Formula:

Runway (months) = Cash balance / Monthly net burn

Monthly net burn = Cash out - Cash in (collected, not invoiced)

The common pitfall: using invoiced revenue instead of collected cash. Annual contracts billed upfront look like cash until the next renewal cycle, and then cash suddenly doesn't match the P&L.

2. Rolling 12-month forecast updated monthly

A forecast that is only updated for board meetings is not an FP&A function. It's a reporting function.

A rolling 12-month forecast means every month you add a new month at the end and update your assumptions based on what actually happened. This is the structure that lets you catch a slowdown in new logo growth in month two rather than month five.

McKinsey's research on advanced FP&A practices identifies back-testing as one of the highest-leverage habits in forecasting: comparing projections against actuals every month — not just quarterly — is what allows teams to identify and correct systematic estimation errors before they compound. The same principle applies at the startup stage: a rolling forecast you never update is a static budget with a different name.

The mechanics:

- Lock actuals for the closed month within 10 days of month end

- Update your forward assumptions (growth rate, churn rate, headcount ramp) based on what changed

- Compare your new forecast to the prior forecast - the delta is where the conversation needs to happen

3. Actuals vs. plan with explicit variance owners

Every line in your P&L with a variance greater than 10% needs an owner and an explanation. Not a narrative paragraph - a one-line answer to "is this timing, a structural change, or a mistake in the original assumption?"

The discipline of labeling variances by type - rather than writing prose that obscures them - is what separates FP&A from financial reporting.

4. Unit economics as a decision input, not a board slide

CAC and LTV reported as single numbers are almost useless for decisions. The question you need answered is: "which channels, cohorts, and contract sizes are generating positive unit economics, and which are eroding them?"

That requires:

- CAC by channel (paid, outbound, inbound, partner) - not blended

- LTV by cohort (customers signed in Q1 2024 vs. Q3 2025 look different)

- CAC payback period by ACV band

OpenView's benchmark data ties CAC payback directly to net dollar retention to define what "healthy" actually looks like: below 100% NDR, target CAC payback under 12 months; at 100–120% NDR, 12–18 months is acceptable; at 150%+ NDR, you may tolerate longer payback depending on cash and product stickiness. The point is that a blended CAC payback number means nothing without knowing your retention profile — the two metrics must be read together.

When you see a blended CAC of $8,000 and a blended LTV of $32,000, the ratio looks fine. When you break it down and see that your outbound enterprise motion has a $22,000 CAC with an LTV of $28,000, the picture changes entirely. That's the number that drives channel allocation decisions.

5. Headcount model linked to cash

Headcount is usually the single largest cost line at $5–50M ARR. It is also the cost most commonly added without a forward model.

A headcount-linked FP&A model answers:

- What does the cash runway look like if we hire the planned five engineers and two AEs this quarter?

- At what ARR does this headcount become self-funding based on current gross margin?

- What is the trade-off between hiring two salespeople now vs. waiting two quarters?

The loaded cost calculation matters here. Base salary is not the number to put in the model. Loaded cost - including payroll taxes, benefits, equipment, and allocated overhead - is typically 1.25x to 1.35x base salary for most US-based SaaS companies.

The FP&A cadence: what to do and when

The question "how often should we run FP&A?" has a clear answer for this stage: monthly, with weekly cash monitoring.

Here's the cadence that works at $5–50M ARR:

Weekly (15 minutes, founder or Head of Finance)

- Cash balance vs. last week

- Any invoices overdue beyond 30 days

- Any unexpected large payments

Monthly (2–3 hours, founder + finance owner)

- Close actuals within 10 days of month end

- Update rolling 12-month forecast

- Label and explain variances >10%

- Refresh runway under base, downside, and upside

- Identify any assumptions that need to change before next board meeting

Quarterly (4–6 hours, founder + finance owner + optional fractional CFO)

- Full scenario review (what changed vs. the annual plan?)

- Update headcount model for next two quarters

- Review unit economics by channel and cohort

- Prepare board materials with decision framing - not just performance reporting

Annually (2–3 days, with external support if needed)

- Set the annual operating plan with department-level budgets

- Agree on the metrics definitions that will govern reporting for the year

- Lock assumptions ownership: who owns the inputs to each major forecast driver?

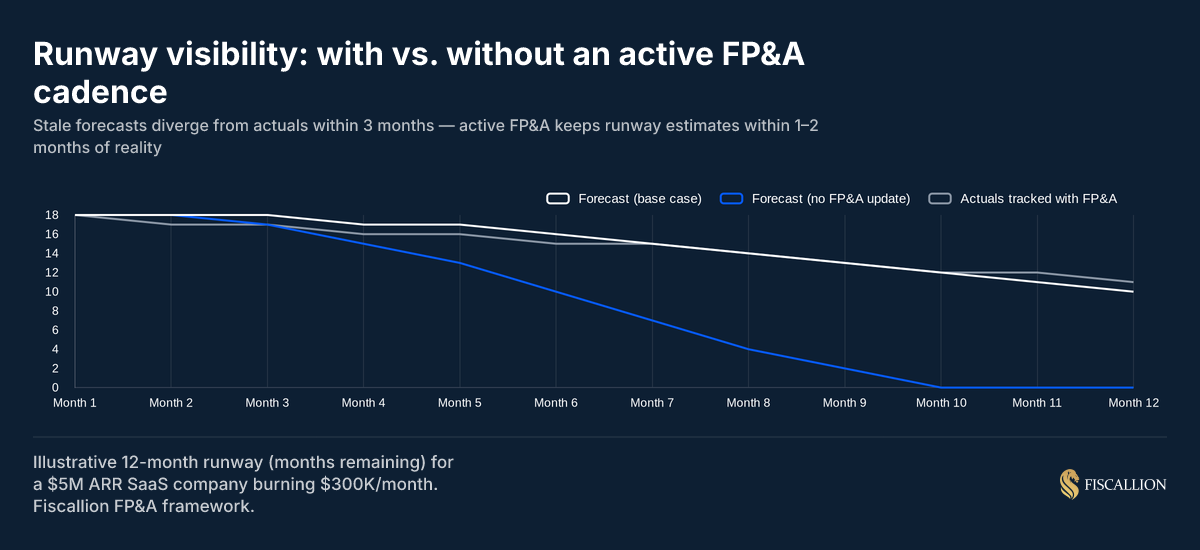

The chart above illustrates what happens to runway visibility when forecasts stop being updated. A stale model diverges from actuals within 90 days - often by several months of runway.

How to structure the FP&A model itself

A functional startup FP&A model is not a 40-tab spreadsheet. It's a linked, three-statement structure that lets you change one assumption and see the cash impact within 60 seconds.

The minimum viable FP&A model for a $5–50M ARR SaaS company contains:

Assumptions tab

- Revenue drivers: MRR, churn rate, expansion rate, new logo additions by month

- Headcount plan: roles, start dates, loaded costs

- COGS drivers: hosting, support, payments as % of revenue

- Opex: fixed items (office, tools, insurance) + variable items (marketing spend, sales commissions)

Revenue schedule

- Monthly MRR build: opening MRR + new ARR + expansion - churn = closing MRR

- Recognized revenue split from deferred (critical for annual contracts)

Headcount schedule

- Roles by function, start month, and loaded cost

- Auto-roll of headcount costs into opex and cash burn

Three-statement model

- Income statement (P&L)

- Cash flow statement - this is the most important output for runway

- Balance sheet (required if you carry deferred revenue, AR, or AP on meaningful scale)

Scenario toggles

- Base, downside, and upside - ideally as a single switch in the assumptions tab

- The downside scenario should reflect: churn +2%, new logo growth -30%, no expansion ARR

The goal is not to build the most sophisticated model. The goal is to build a model that any informed person can update in under two hours when a key assumption changes.

FP&A maturity vs. decision quality

The pattern is consistent across the $5–50M ARR range: companies with a formal FP&A cadence outperform on every decision quality dimension. The gap is widest on cash visibility and runway confidence - the two inputs that most directly affect when and whether you raise, hire, or cut.

Who owns FP&A at the startup stage

This is where many companies get stuck. They're too small to justify a full-time VP of Finance, but the founder is too busy to own the FP&A cadence themselves.

The honest answer: FP&A ownership depends on your current stage.

$5M–$10M ARR

The founder or CEO should own the assumptions. A bookkeeper or controller closes the actuals. A fractional CFO or FP&A advisor runs the monthly cadence and maintains the model. This is the most capital-efficient structure - you get CFO-level judgment on the inputs without a full-time hire.

Establishing an intentional, recurring cadence keeps this system actionable without creating unnecessary organizational drag. Rather than serving as a passive reporting function, the process shifts focus onto immediate re-forecasting and distributed input accountability

$10M–$25M ARR

A Head of Finance or Senior FP&A Analyst takes over day-to-day model maintenance and the monthly close cycle. The founder reviews the output and owns the strategic decisions the model informs. A fractional CFO provides board-level financial narrative and scenario planning support.

$25M–$50M ARR

A full-time CFO or VP Finance starts to make sense - but only if the FP&A system is already working. Hiring a CFO into a broken FP&A environment produces expensive reporting polish, not better decisions.

The mistake at every stage is the same: hiring a person before building the system. The person ends up spending their first 90 days building infrastructure that should already exist.

At Fiscallion, the companies that get the most from our financial planning and analysis services are the ones that engage before the chaos point - not in response to it. The CFO-level FP&A advisory model works because it separates assumption ownership from assumption execution.

The most common FP&A mistakes at $5–50M ARR

Mistake 1: using revenue instead of cash

The model shows 18 months of runway. The bank account says 11. The gap is almost always deferred revenue - annual contracts billed upfront that show as revenue but haven't been fully earned - and AR timing - invoices sent but not yet collected.

Replacement move: Cash flow statement first, always. If your model doesn't have a cash flow statement linked to the P&L, your runway number is not reliable.

Mistake 2: treating the board deck as the FP&A output

The board deck is a communication artifact. FP&A is the process that generates what goes in it. When the board deck becomes the trigger for doing FP&A rather than the output of it, you are always operating with a 30-45 day lag on your own numbers.

Replacement move: Separate the model from the deck. The model runs monthly regardless of board cycle. The deck is built from the model in the week before the board meeting.

Mistake 3: blending assumptions that should be segmented

Blended churn, blended CAC, and blended gross margin all look fine until one cohort or segment starts deteriorating. By the time the blended number moves, the underlying problem is usually 6–9 months old.

SaaStr's analysis of high-NRR SaaS businesses illustrates why this matters: median NRR across private SaaS companies has fallen materially, but the companies where it has declined most are those where cohort-level degradation was masked by blended aggregates until it was too late to act. You cannot manage a trend you cannot see.

Replacement move: Segment by channel for CAC, by cohort for churn and expansion, and by contract type for gross margin. You don't need 40 cuts - you need the 3–4 that correspond to actual strategic decisions you face.

Mistake 4: orphaned assumptions

Most financial models have inputs that nobody owns. The growth rate for enterprise new logos is in the model, but nobody reviewed whether it was still reasonable after the last quarter. The customer success team knows churn is getting worse, but it hasn't made it into the forecast.

McKinsey's research on FP&A best practice identifies the same failure mode at larger companies: probability values and key assumptions go unstated or unowned, leading to wildly inconsistent forecasts across business units. The fix is identical at the startup stage — one owner per material assumption, stated explicitly, updated on a known cadence.

Replacement move: Assign an owner to every material assumption. Revenue growth rate: owned by the CEO with sales input. Churn rate: owned by VP CS with monthly update. CAC by channel: owned by VP Marketing. These owners update their inputs before the monthly model refresh.

Mistake 5: skipping the downside scenario

The base case is not a decision tool. It's a description of expectations. The downside scenario - what happens if new logo growth drops 30%, churn ticks up 1.5%, and that enterprise deal closes in Q3 instead of Q1 - is where decisions live.

a16z's burn multiple framework makes the underlying logic explicit: a one-in-three probability of a bad outcome is not a tail risk — it's a planning input. Companies that fail to model the downside explicitly are more likely to face it unprepared.

Replacement move: Run the downside scenario every month, not just before a board meeting. If the downside scenario shows less than 12 months of runway, that is a decision trigger - not a data point to present.

Board reporting as a FP&A output, not a reporting exercise

Board decks that show only what happened are not FP&A outputs. They are reports.

A board deck built on a working FP&A system shows three things:

- What happened vs. what we planned - with variance explanations, not just variance numbers

- What the updated forecast shows - including the downside scenario and what would have to be true for it to materialize

- What decision the board needs to make - or what the management team has already decided, with the trade-off that was evaluated

The third element is what most boards actually want and rarely get. "We closed $1.2M ARR vs. $1.4M plan" is a report. "We closed $1.2M ARR vs. plan. The shortfall is entirely in the outbound enterprise segment where we have a 90-day sales cycle problem. We are choosing between: (a) extending the current team's runway with a target revision, or (b) adding one experienced enterprise AE in Q2. The cash impact of option B is $180K loaded cost before productivity. Here's what each path looks like for runway." - that's an FP&A output.

Fiscallion's fundraising and investor support work is built on this framing. The financial narrative - pitch deck, investor updates, due diligence responses - is only as strong as the FP&A system underneath it.

When to bring in fractional CFO support

Most companies at $5–50M ARR don't need a full-time CFO. They need CFO-level judgment applied at the right moments.

Those moments are:

- Building the annual operating plan for the first time with real departmental input

- Preparing for a Series B or Series C fundraise where unit economics scrutiny intensifies

- Navigating a cash crunch that requires real scenario planning, not back-of-envelope math

- Transitioning from cash-basis to accrual accounting, where the month-close process changes materially

- Building board-ready financial materials where the narrative and the numbers need to align

A fractional CFO at this stage does two things a controller or bookkeeper does not: owns the model assumptions, and translates the numbers into the trade-off language that drives decisions.

The fractional CFO advisory at Fiscallion is built around this gap - getting CFO-level judgment onto the assumptions and decision framing without the full-time cost before you need it.

FP&A implementation checklist: where to start

If you are starting from scratch or fixing a broken FP&A function, work through this in order. Each step is a prerequisite for the next.

Step 1 - Clean up the actuals (Week 1–2)

- Confirm your books are closed and accurate for the last 3 months

- Confirm your MRR schedule reconciles to your billing system

- Confirm deferred revenue is tracked separately from recognized revenue

Step 2 - Build or audit the model structure (Week 2–4)

- Confirm the model has a three-statement structure (P&L, cash flow, balance sheet)

- Confirm revenue is modeled from drivers (MRR build) not top-down guesses

- Confirm headcount has a line-by-line plan with loaded costs

- Confirm the model has a base and downside scenario

Step 3 - Assign assumption owners (Week 3–4)

- Revenue growth rate: assign an owner

- Churn and expansion rate: assign an owner

- CAC by channel: assign an owner

- Headcount plan: assign an owner

- COGS drivers: assign an owner

Step 4 - Establish the monthly cadence (Month 2)

- Set a hard close date (actuals locked within 10 days of month end)

- Schedule a monthly model review meeting with assumption owners

- Build a one-page monthly summary: actuals vs. plan, runway (base + downside), and the one decision the numbers are pointing to

Accelerating the monthly close requires moving away from slow, manual processes like hand-matching transactions or waiting endlessly for trailing vendor invoices. Delays in this area ultimately force executive teams to steer the business using obsolete historical data.

Step 5 - Connect FP&A to board materials (Month 3)

- Build the board financial section from the model, not separately

- Draft the variance section using the three-type framework (timing, structural, assumption error)

- Include the downside scenario runway in every board package

Turn your model into the process

FP&A for startups is not about hiring the right person or buying the right tool. It's about building a system where assumptions are owned, actuals are closed on time, and the output answers the question: "given where we are, what should we do next?"

At $5–50M ARR, the companies that make better capital allocation decisions - hire faster when growth is ahead of plan, cut sooner when it isn't, and raise at better terms because their numbers are clean and defensible - are the ones with a working FP&A function, not necessarily the ones with the largest finance team.

The gap between where most SaaS companies are and where they need to be is rarely a headcount problem. It's a decision-quality and FP&A architecture problem.

If you want to audit your current FP&A setup - what's working, what's creating blind spots, and what to fix first - book a working session with Fiscallion.