A secondary sale lets a founder, employee, or early investor turn paper equity into cash without the company raising new capital or issuing a single new share. The decision that actually matters is not "can we do this" (the mechanics are well understood) but sizing, timing, and how you frame it to your board so it reads as discipline instead of doubt. Get the size wrong and a secondary sale becomes the thing your next lead investor brings up in every diligence call. Get it right and it removes personal financial pressure from the people building the company, without touching your cap table's dilution math or your cash runway model.

This is a decision that belongs in your FP&A process, not just your legal team's inbox. Every secondary sale changes who owns what, how your next round gets priced, and what story your board deck tells about company health. Treat it like any other capital allocation decision: model it, size it against a range, and own the assumptions before you take it to the board.

What you'll learn

- What a secondary sale is and how it differs from a primary raise, tender offer, or company buyback

- How to calculate the size of a secondary sale relative to your holdings, your round, and your cap table

- How to interpret secondary sale size and timing as a signal to investors and employees

- What to model before you approve or request a secondary sale

- The most common sizing and framing mistakes, and the better move for each

- A practical readiness checklist you can run before your next board conversation

What is a secondary sale in startups

A secondary sale is a transaction where an existing shareholder, a founder, an employee, or an early investor, sells their shares to a buyer. The company is not a party to the cash flow. No new shares get created, and no capital lands on your balance sheet.

Compare that to a primary raise, where the company issues new stock and the proceeds go straight to the business to fund growth. A Series B round might include $30 million in primary capital plus $5 million in secondary; your cash balance only grows by the $30 million, but your cap table shifts on both pieces.

| Transaction type | Who receives the cash | Effect on company cash | Effect on ownership |

|---|---|---|---|

| Primary raise | The company | Increases cash balance | New shares issued, all existing holders diluted |

| Secondary sale | The selling shareholder | No change | Existing shares change hands, no new dilution |

| Tender offer | Selling employees/founders | No change | Structured, company-run secondary at a set price |

| Stock buyback | Selling shareholders | Decreases cash balance | Company repurchases its own shares, consolidating the table |

Secondary sales show up in a few recognizable forms:

- Founder secondary: a founder sells a modest slice of personal holdings, usually bundled into a priced round, to the new lead investor or an existing investor increasing their stake.

- Tender offer: the company runs a structured, company-sponsored window where eligible employees (sometimes founders too) can sell a portion of vested shares at a set price, often the last round's valuation. The distinction between a tender offer and a broader secondary sale matters legally—Gunderson Dettmer's overview lays out why all tender offers are secondary sales but not all secondary sales are tender offers.

- Direct secondary: a shareholder finds a buyer independently, subject to the company's right of first refusal (ROFR) and any co-sale (tag-along) rights in the investor rights agreement.

- Fund secondary: an early investor sells its position, or its LP interest in the venture fund, to a dedicated secondary buyer, unrelated to your company's own cap table decisions but relevant if it shows up as a new name on your table.

The mechanics run through the same documents every time: your investors' rights agreement, your certificate of incorporation, and any ROFR/co-sale agreement. Almost every venture-backed company restricts share transfers, which means a secondary sale is never a private handshake. It requires board awareness, notice periods, and usually company counsel managing the paperwork so the cap table stays clean. Cooley's guide to secondary sales of private company stock walks through the legal considerations—securities law, 409A impact, tax treatment—that make counsel involvement non-negotiable.

How to calculate the size of a secondary sale

The number that matters is not the dollar amount. It is the percentage of the seller's holdings changing hands, because that percentage is what gets read as a signal.

Run the calculation in three steps.

Step 1: Calculate the seller's stake before the transaction.

Take fully diluted shares owned, common or preferred as applicable, divided by fully diluted shares outstanding.

Step 2: Calculate the percentage of the position being sold.

Shares sold ÷ shares owned before the transaction = percent of position liquidated. This is the number a lead investor will ask for immediately.

Step 3: Calculate the price relative to the last primary round.

Secondary shares, especially common stock, typically price at a discount to the headline valuation from the most recent primary round, because preferred shares carry liquidation preferences and protective rights that common stock does not have. Model the range, not a single number, the same way you'd model a CAC or LTV range instead of anchoring to one point estimate. Typical secondary discounts run 20–40% below the last preferred round price—Earlyasset's breakdown of the secondary discount explains the five structural reasons behind that range.

Market practice on sizing has landed in a fairly narrow band across recent deal data and legal guidance, and it shifts by stage. PitchBook's Q1 2025 analysis estimated the total US VC direct secondary market at $41.8–$59.9 billion, and Industry Ventures' 2025 outlook projected global venture secondary volume exceeding $120 billion—both reflecting a market that has grown materially as companies stay private longer.

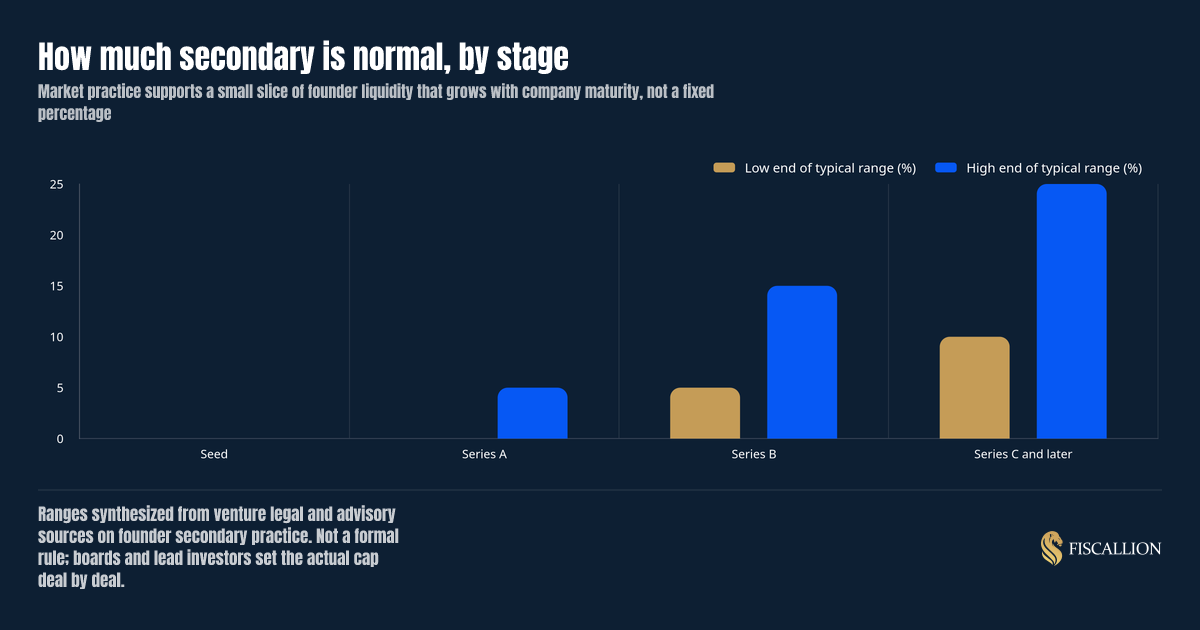

| Stage | Typical secondary range | What it signals |

|---|---|---|

| Seed | Rare, near 0% | Almost never appropriate; reads as a lack of conviction before you've proven the model |

| Series A | 0-5% of a founder's position | Occasionally negotiated as a small $100K-$250K allocation, not a norm |

| Series B | 5-15% | The realistic window opens; investors expect founders with 5+ years in to want some liquidity |

| Series C and later | 10-25% | Common, often formalized through structured tender offers |

None of these ranges are codified law. They are patterns that show up across venture financing term sheets and advisory practice. The number that actually gets negotiated in your term sheet is whatever your lead investor is willing to cap it at, and that cap is the real signal, not a rule you can cite back to them.

How to interpret a secondary sale as a signal, not just a transaction

A secondary sale tells your investors, employees, and future acquirers something about what you believe the next few years look like. Read it the way your board will.

Small and modest reads as retention insurance. A founder selling 5-10% of a position, alongside a strong primary round, signals that the person building the company can stop worrying about a mortgage and start compounding decisions with a longer time horizon.

Large or early reads as a loss of belief. Selling 20% or more, especially before the business has proven durable retention or margin, tells the room you might be more interested in de-risking than building. Investors underwriting growth do not want to co-invest next to someone quietly exiting.

Timing changes the read entirely. A secondary tied to a strong primary round, healthy net revenue retention, and a lead investor's blessing looks like normal portfolio management. A secondary requested because you need personal cash, disconnected from company performance, looks like distress even if the business is fine.

Employee-wide tenders read differently than founder-only sales. The market has shifted meaningfully here. Recent tender offers at companies like Clay, Linear, and ElevenLabs were structured to include broad employee participation, not just founders, and that framing gets received far better by investors and the press than the founder-heavy secondary sales common during the 2020-2021 period. Carta's VC secondary trends report documented $61.1 billion in total VC secondary transaction value from July 2024 through June 2025—surpassing the combined value of all VC-backed IPOs over the same period—driven largely by this shift toward broader liquidity programs. If you are considering a tender, structuring it as a company-wide liquidity window rather than a founder-only cash-out changes how your board and future investors interpret it.

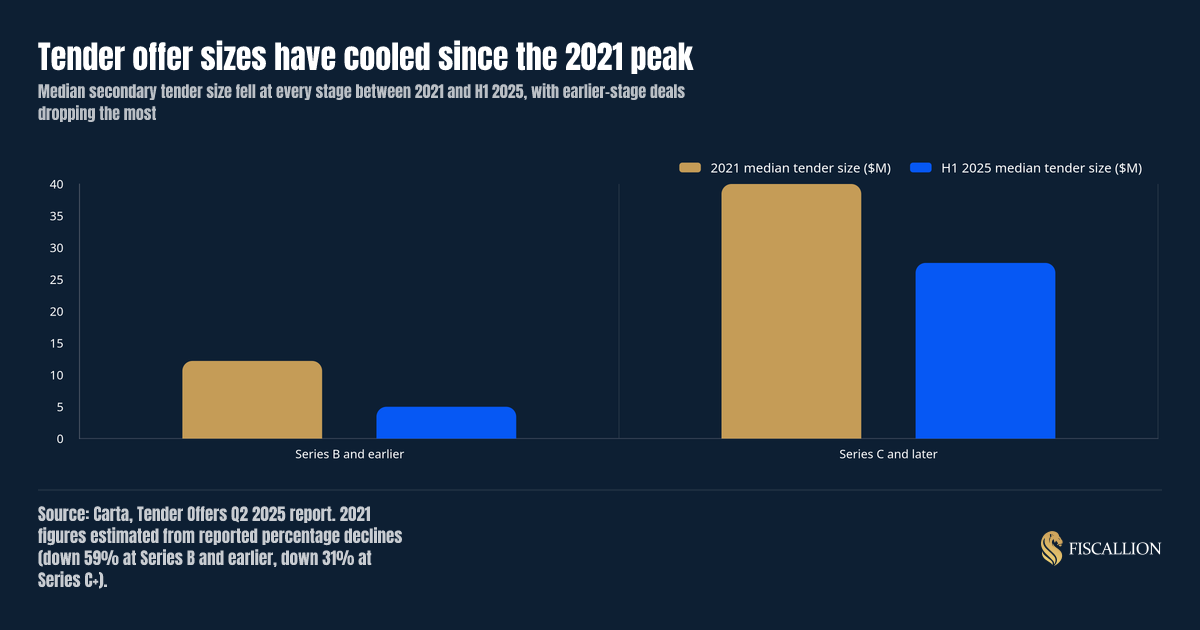

Tender offer sizes themselves have also normalized since the 2021 peak, which matters context for what "typical" looks like right now.

Median tender size at Series C and later fell roughly 31% between 2021 and the first half of 2025. At Series B and earlier, it fell about 59% over the same window. Deals are smaller and more disciplined than they were during the zero-rate era, which is exactly the environment a board expects you to model against, not the 2021 peak comparables that still circulate in founder group chats.

What to do next: build the model before you take it to the board

Do not bring a secondary sale request or proposal to your board as a legal question. Bring it as a modeled decision.

- Model the cap table before and after. Show fully diluted ownership pre- and post-transaction. Confirm total shares outstanding are unchanged, because a secondary does not dilute anyone; it only changes who holds what.

- Model the price discount explicitly. Do not anchor to the last round's headline preferred price. Build a range for what common stock should trade at given your liquidation preference stack, and show your board that range rather than a single assumed number.

- Tie the ask to a cash flow and runway story, not just a cap table story. Even though a secondary doesn't touch company cash, your board will still ask what problem it solves. Have the answer ready: retention risk, founder compensation history, or a specific employee flight risk you're managing against. This is the same runway-versus-dilution trade-off modeling that should sit at the center of your capital allocation decisions.

- Set the cap before you negotiate, not during. Decide internally what percentage of any individual's position is on the table before you're in the room with a lead investor. A number you defend on the spot reads as improvised; a number you walk in with reads as governed.

- Decide who gets to participate and document it. If it's a tender, define eligibility (all vested holders vs. a subset), the price, and the participation cap before you announce it. Ambiguity here creates internal resentment fast.

- Confirm ROFR and co-sale mechanics with counsel before any conversation with a buyer. Skipping this step can void the transfer or breach your investor agreements outright. The SEC's tender offer rules and interpretations and Morrison Foerster's private company tender offer guidance both make clear that whether a transaction constitutes a formal tender offer turns on a multi-factor test—not on what the parties call it.

This is the same discipline Fiscallion applies across cash flow visibility, runway forecasting, and board reporting: state the assumption, model the range, and bring your board a decision framed with trade-offs, not a fact pattern they have to interrogate. A secondary sale decision without a modeled cap table and cash story is the same mistake as a headcount plan without a hiring model or a CAC number treated as a single point instead of a cohort range.

Common mistakes and the better move

| Common mistake | Why it backfires | Better move |

|---|---|---|

| Anchoring the sale price to the last round's headline valuation | Preferred and common stock carry different rights; buyers won't pay preferred pricing for common | Model a discount range based on your liquidation preference stack and negotiate from there |

| Treating the secondary size as a private negotiation with no internal cap | Investors set the number for you in the room, and it can land larger than you're comfortable defending | Decide your own cap before any conversation starts, then hold the line |

| Framing a founder-only cash-out as a routine liquidity event | Investors and employees read founder-only secondaries as a signal that leadership is quietly de-risking | Structure liquidity as a company-wide tender where possible, or clearly limit founder participation below employee caps |

| Requesting a secondary during a weak quarter or a raise driven by need, not momentum | Investors underwriting survival read any liquidity ask as confirmation you don't believe in the business | Time the ask to a strong primary round or a period of clear, demonstrable momentum |

| Skipping the ROFR and co-sale review before talking to a buyer | You can void the transfer or breach your investor rights agreement, creating a legal mess mid-transaction | Confirm transfer mechanics with counsel first, every time, before any buyer conversation |

| Presenting the transaction to the board as a legal update instead of a modeled decision | The board is left to ask basic questions you should have already answered | Bring the cap table model, the pricing range, and the rationale in one package |

A practical readiness checklist

Run this before you say yes to a secondary sale, a tender offer, or a founder liquidity request.

- What percentage of the seller's fully diluted position does this represent?

- Where does that percentage land against the stage-appropriate range, and can you defend the gap if it's outside it?

- What is the pricing discount versus the last primary round, and is it modeled as a range?

- Is this tied to a strong primary round and real momentum, or is it disconnected from company performance?

- Have you confirmed ROFR, co-sale, and any lock-up terms with counsel?

- Is the participation pool limited to founders, or does it include employees, and have you thought through why?

- What does the post-transaction cap table look like, and have you shown it to your board before the ask, not after?

- What's the retention or morale problem this solves, and can you name it specifically rather than generally?

If you can't answer all eight with a number or a name attached, the request isn't ready for the board yet. This is exactly the kind of decision-grade prep Fiscallion builds into board reporting: not a history recap, but a framed choice with the trade-offs already worked through.

FAQ

What is secondary sale in startups?

A secondary sale in startups is any transaction where an existing shareholder, a founder, an early employee, or an early investor, sells their shares directly to a buyer instead of the company issuing new stock. The company receives no proceeds and no new shares are created. Ownership simply changes hands. It's distinct from a primary raise (new shares, cash goes to the company) and from a stock buyback (the company itself repurchases shares, reducing cash on the balance sheet). Common buyers in a startup secondary sale include new investors joining a funding round, existing investors increasing their position, or dedicated secondary funds and marketplaces that specialize in pre-IPO equity—Carta's guide to the secondary market covers the full range of transaction types and buyer profiles.

What is the 7% sell rule?

There is no formal, codified "7% sell rule" written into securities law or standard venture financing documents, so treat any version you've heard as an informal guideline rather than a binding rule. What people usually mean when they reference a number like this is the informal diversification guidance financial advisors give employees and founders sitting on concentrated equity: sell a modest, single-digit-to-low-double-digit percentage of vested holdings periodically, rather than holding 100% of your net worth in one illiquid, unhedged position. In practice, the market-observed ranges are closer to 5-10% of a position read as neutral diversification, 10-20% as acceptable with a clear narrative, and anything above 20-30% triggering real scrutiny from a board or lead investor. If someone cites a specific "7%" figure to you, ask what source or agreement it comes from before treating it as policy, because your actual constraint is whatever your investor rights agreement, ROFR terms, and board are willing to approve.

Is a secondary offering good or bad?

Neither, by default. A secondary offering is a tool, and whether it's good or bad depends entirely on size, timing, and framing. A modest, well-timed secondary alongside a strong primary round can be genuinely healthy: it reduces personal financial pressure on founders and key employees, which tends to produce better long-term decisions instead of decisions driven by desperation for liquidity. It can also broaden your shareholder base with patient capital. It turns bad when it's large relative to the seller's position, disconnected from company momentum, or framed as a founder-only cash-out that reads as reduced conviction. The same transaction structure can be read as disciplined portfolio management or as a red flag depending entirely on the percentage sold and the story around it.

What is a secondary startup?

"Secondary startup" isn't a distinct company category; it typically refers loosely to a startup that has run or is running a secondary transaction, most often a tender offer, as part of its normal financing and equity management cadence. Companies staying private for 10+ years now routinely run secondary programs as a substitute for the liquidity an IPO used to provide on a predictable timeline. This has gone from a niche, sometimes-stigmatized move to a standard part of late-stage private company operations, particularly among companies with strong revenue growth and low burn that don't actually need more primary capital but still need to give employees and early holders a path to cash. Industry Ventures' market sizing analysis traces this shift from the 2021 peak through the 2025 recovery, showing how the liquidity gap created by a muted IPO market turned secondaries into a structural feature of venture capital rather than an anomaly.

Conclusion

A secondary sale is not a legal formality you clear with counsel and move past. It's a capital allocation and signaling decision that deserves the same modeling discipline you'd apply to a pricing change, a headcount plan, or a runway forecast. Size it against a stage-appropriate range, model the pricing discount explicitly instead of anchoring to the last round's headline number, and bring your board a framed decision instead of a fact pattern to interrogate.

Most $5-50M ARR companies that get burned by a secondary sale didn't have a legal problem. They had a decision-quality problem: no modeled cap table before the ask, no defensible cap on the percentage, no story connecting the request to company performance. That's the same gap Fiscallion closes across cash flow visibility, runway forecasting, and board reporting, because a secondary sale is just one more decision that needs assumptions owned and trade-offs modeled before it reaches your board deck.

Audit your metrics definitions and forecasting model before your next board conversation touches liquidity, dilution, or cap table changes.