Most founders celebrate when a term sheet drops, sign it quickly, and leave the 'details' to the lawyers. That is a million-dollar mistake. A term sheet isn't just a preliminary proposal; it’s where your actual payout at exit is permanently locked in. If you don't negotiate the structure now, you won't have the leverage to do it later.

This guide walks you through what a term sheet is, which clauses carry the most economic weight, how it differs from a letter of intent, and what to do before you sign anything.

Key takeaways

- A term sheet is non-binding on deal terms but binding on no-shop and confidentiality - violating the exclusivity clause exposes you to real legal risk.

- Liquidation preferences and the option pool shuffle together determine your effective ownership and payout at exit more than valuation does. Most founders negotiate valuation and miss both.

- The 50/100/500 rule is a useful maturity signal, not a fundraising formula - passing one of those thresholds changes what investors expect from your financial infrastructure.

- At Series A and beyond, the quality of your financial model and data room has more influence on deal outcome than your pitch deck.

What a term sheet is - and what it actually commits you to

A term sheet is a preliminary document that outlines the key financial and governance terms of a proposed investment. It is not the final deal. It is a structured offer - usually two to five pages at Series A, occasionally longer for complex rounds - that becomes the blueprint for the definitive legal documents: the stock purchase agreement (SPA), investors' rights agreement, and voting agreement.

The term sheet signals that the investor has formed a view on your business and is prepared to negotiate specifics. It is the first time most investors formally state their interest in numbers and structure.

Crucially, 'non-binding' is a misnomer. Two provisions are always legally binding:

- The no-shop (exclusivity) clause - Once signed, you typically agree not to solicit or entertain other investors for 30 to 60 days.

- Confidentiality - Both parties agree not to disclose the terms publicly.

Violating the no-shop clause is not a soft reputational risk. It is a contractual breach that can result in legal liability and, just as damaging, permanently end your relationship with investors in a market where everyone talks.

Never sign a term sheet under pressure to stop talking to other investors without first confirming you are genuinely ready to pursue this specific deal. If you are not, say that clearly and negotiate the timing.

The core components: what's in a term sheet and why it matters

Every venture-backed term sheet covers three categories of terms. Some are highly negotiated. Others are market standard. Knowing which is which saves time and relationship capital.

The National Venture Capital Association (NVCA) publishes model term sheet documents that represent the closest thing to an industry standard in U.S. venture financing. They are worth reading once in full before you enter any fundraising process.

Pricing and economics

These are the terms that determine how much your equity is actually worth.

The option pool shuffle is one of the most consistently misunderstood pricing dynamics at Series A. Investors typically require you to expand the option pool to a target percentage before closing. Because that expansion happens pre-money, it dilutes existing shareholders - primarily founders - not the new investor. A $15M pre-money valuation with a 15% option pool expansion has a materially different effective price per founder share than the headline number suggests. Run the fully diluted math before you assess whether the valuation is fair.

Economic rights

These determine how proceeds are distributed when the company is sold, wound down, or goes public.

Liquidation preference is the single most economically consequential clause in most early-stage term sheets. It defines what investors get paid back - and in what order - before common shareholders receive anything in a liquidity event.

The key variables:

- Multiple: 1x is market standard at Series A. Anything above 1x (1.5x, 2x) is aggressive and should be negotiated down.

- Participating vs. non-participating: A non-participating preference means investors take their preference or convert to common and participate pro-rata - not both. A fully participating preference means they take their preference first and then participate again in the remaining proceeds alongside common. Participating preferred is significantly more investor-favorable and should be flagged immediately.

- Capped participation: A middle ground - investors participate after their preference, but only up to a stated multiple cap (e.g., 2x or 3x total return).

In a strong exit scenario, this distinction often matters less. In a moderate exit - a $40M acquisition on a $20M raise - the structure can mean founders and employees receive almost nothing. Andreessen Horowitz's breakdown of the economics of term sheets illustrates exactly this dynamic with worked exit-scenario math.

Pro-rata rights give existing investors the right to maintain their ownership percentage in future rounds by investing additional capital. This is standard and generally acceptable. Watch for super pro-rata rights, which allow investors to take more than their ownership percentage in future rounds - these can create complications if you are trying to bring in new lead investors.

Anti-dilution provisions protect investors if you raise a future round at a lower valuation (a "down round"). The two main variants:

- Broad-based weighted average: The most founder-friendly form. Adjusts the conversion price based on the full dilution impact of the new round.

- Full ratchet: Adjusts the conversion price to match the new lower price exactly. This is extremely investor-favorable and rare in clean term sheets - push back hard if you see it.

For a detailed breakdown of how each anti-dilution structure affects your cap table in a down round, see our equity dilution guide - it covers the compounding math across seed through Series C with worked examples.

Control rights

These terms determine who has authority over company decisions.

Board composition is, in many ways, the most consequential long-term term in the document. A standard Series A board is 5 seats: 2 founders, 1 lead investor, 1 independent. Some deals are structured as 3 seats (1 founder, 1 investor, 1 independent), which is also acceptable. Watch for structures that give investors majority control from day one - that is not standard.

Protective provisions are the list of decisions that require investor approval even if they don't require a board vote. Standard protective provisions include: raising additional equity, selling the company, amending the charter, and taking on debt above a threshold. Non-standard protective provisions - such as requiring investor approval for hiring above a certain salary, or any acquisition regardless of size - should be negotiated out.

Right of first refusal (ROFR) and co-sale rights give investors the right to buy stock before a founder sells to a third party, or to sell alongside the founder. These are standard in VC deals and generally acceptable.

Drag-along rights allow a majority of investors and common stockholders to force a sale even if some shareholders object. These exist for administrative ease and are generally market standard.

Where negotiation effort actually concentrates

Don't waste leverage. Focus your energy where investors are actually willing to move.

Liquidation preference structure and the valuation/option pool math together represent the majority of substantive negotiation. Board composition is the third most significant area. Anti-dilution mechanics and pro-rata rights matter but are easier to get investor alignment on when you frame them correctly.

Most negotiation that stalls does so because founders treat valuation as the primary variable and miss the downstream economic impact of liquidation mechanics.

A higher headline valuation often leads to significantly lower founder payouts due to structural traps like double-dipping participating preferences.

Term sheet vs. letter of intent: the functional difference

Founders at the growth stage encounter both documents, and conflating them creates problems.

A term sheet is primarily used in equity investment rounds. It is an investor's formal offer to fund your company, outlining the financial and governance structure of the transaction. It leads to definitive investment documents.

A letter of intent (LOI) is a broader instrument used across a wider range of deal contexts: acquisitions, strategic partnerships, licensing agreements, and late-stage growth deals. It is less prescriptive than a term sheet and more flexible in structure. In the M&A context, an LOI typically covers purchase price methodology, deal structure (cash, stock, earnout), due diligence conditions, exclusivity period, and expected closing timeline.

Here is how they differ practically:

The practical implication: if an investor sends you an "LOI" for an equity investment, read it the same way you would a term sheet. The label matters less than the substance. Focus on the binding provisions - especially exclusivity - before anything else.

Both documents are generally non-binding on core deal terms. But both contain binding carve-outs that carry real legal weight. "Non-binding" is not a blanket protection. Have legal counsel review either document before you sign.

Term sheets at the early stage: seed through Series A

The format and stakes of a term sheet vary significantly by stage.

Seed stage

At seed, many rounds use a SAFE (Simple Agreement for Future Equity) or convertible note rather than a full priced term sheet. These instruments are standardized, faster to close, and avoid the need to set a firm valuation when the business is still early. Y Combinator, which created the SAFE format, publishes its standard SAFE documents openly and they are widely used as the starting point for most seed rounds.

When a term sheet does appear at seed, it is typically shorter - 2 to 3 pages - and focuses primarily on valuation cap, discount rate, and pro-rata rights. Board composition may not be addressed in detail. Protective provisions are usually minimal.

The risk at seed: simplified documents can obscure economically significant terms. A valuation cap that seems generous now sets the floor for your Series A conversion. A broad MFN (most favored nation) clause in a SAFE can create complications later. Shorter does not mean lower stakes.

If you are preparing financial projections to support a seed raise, our seed round financial projections guide covers the model structure investors actually scrutinize - including why a bottom-up revenue build is non-negotiable and what the assumptions tab must contain.

Series A

Series A is where the full term sheet structure described above becomes standard. Governance terms come into sharp focus. Board seats are formally negotiated. The option pool expansion is calculated. Liquidation preference mechanics are set.

Y Combinator has published a model Series A term sheet that is widely referenced as a benchmark for what a clean, founder-friendly structure looks like. It is a useful calibration tool before you receive your own.

The FP&A readiness bar also increases substantially. Before you receive a term sheet at Series A, serious investors will have reviewed your financial model, your unit economics, and your metrics package. After you receive the term sheet and enter formal due diligence, they will go deeper: cohort retention by ARR cohort, CAC by channel, and scenario-level runway analysis.

If your financial model doesn't have an explicit assumptions tab, if your CAC is blended rather than channel-specific, or if your NRR is calculated without a documented cohort methodology, these gaps will surface during due diligence - typically after you've signed the no-shop clause and lost leverage to keep other conversations running.

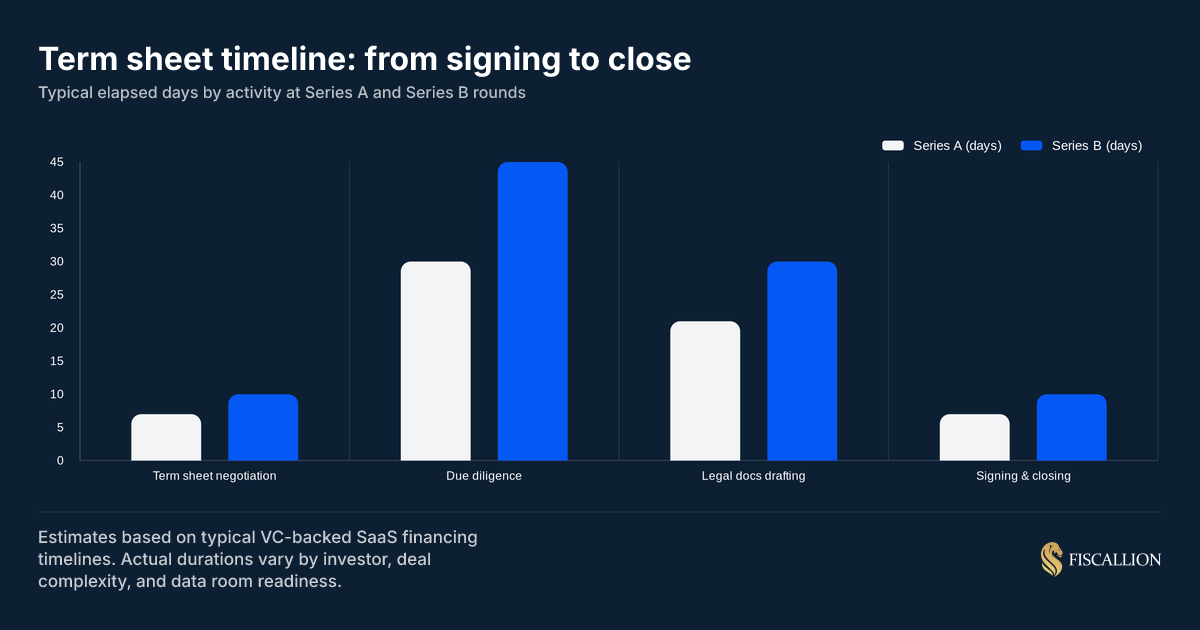

Build the data room before you receive the term sheet, not after. The fastest way to close at Series A is to enter due diligence already organized. Our due diligence checklist for startups covers every document and metric investors examine at Series A through Series C - including the financial model tests and unit economics documentation that cause the majority of deal friction.

What the 50/100/500 rule means for your fundraising readiness

The 50/100/500 rule - popularized by technology analyst Alex Wilhelm - describes when a startup can generally be considered to have exited the early experimental phase and entered a more mature operating structure. The thresholds are:

- $50M in annual revenue

- 100 or more employees

- $500M valuation

When any one of these milestones is reached, the argument is that the company is no longer a startup in the operational sense - it is a structured business with defined departments, a validated model, and investor confidence behind it.

For fundraising purposes, the rule is useful in a different way than most founders expect. These thresholds are not targets to aim for before raising. They are signals that change what investors expect from your financial infrastructure.

Here is how the rule maps to investor expectations:

The implication for SaaS founders at $5–50M ARR is direct: you don't need to reach these thresholds before raising, but approaching them signals that investors will hold your financial model and data room to a higher standard. A $20M ARR SaaS company raising a Series B at a $150M valuation is not yet at the 50/100/500 threshold - but investors will apply a scrutiny level closer to that standard than to a seed round.

The 50/100/500 rule also reframes what "not a startup anymore" means practically. Once you're past one of these thresholds, the finance function needs to operate as a structured discipline - not just a quarterly board deck and a shared spreadsheet. That does not necessarily mean hiring a full-time CFO. It means the FP&A infrastructure - assumptions documented, scenarios modeled, unit economics tracked at the cohort level - needs to exist and be owned.

Most companies at $5–50M ARR don't have a CFO problem. They have a decision-quality and FP&A problem. Adding a CFO without fixing the underlying model and assumptions ownership adds reporting overhead without improving the quality of decisions. The fractional CFO model exists precisely for this stage: you need the strategic financial judgment, not the full-time headcount cost.

How to negotiate a term sheet: the clauses that move and the ones that don't

Not everything in a term sheet is negotiable. Knowing the difference matters more than being aggressive on everything.

Clauses that move with a clear rationale

Liquidation preference multiple: 1x is market standard. If you receive a 1.5x or 2x preference, push back directly - it is not market and you should name that. Offer data: "Our last three comparable deals closed at 1x non-participating. We'd like to match that structure."

Participating vs. non-participating preferred: Fully participating preferred is investor-favorable and non-standard in clean term sheets. Push for non-participating. If the investor won't move, propose a participation cap at 2x or 3x total return.

Option pool size: Every point of option pool expansion reduces your effective pre-money price per share. Negotiate the size down to what is actually needed for the next 12-18 months of hiring, not what gets you to some round number. Know your hiring plan before you negotiate this. Our cap table management guide walks through how to build a forward-looking grant model against a specific hiring plan - the argument that keeps the pool smaller than an investor's opening ask.

Board composition: If a 3-seat board structure is proposed (investor, founder, independent), understand that the independent is often harder to fill than it sounds and can create a de facto 2:1 investor advantage until the seat is filled. Push for 5 seats if you have a strong candidate in mind.

Exclusivity period: The standard is 30-60 days. If you have active competing processes, negotiate a shorter window or a hard deadline with defined consequences if the investor doesn't close by a specific date.

Clauses that rarely move

1x liquidation preference (market standard): If you've negotiated to 1x, that is already the founder-friendly outcome. Don't push further.

ROFR and co-sale rights: These are universal in VC deals and exist for reasonable structural reasons. Negotiating these out is almost never worth the relationship cost.

Standard drag-along provisions: Majority-vote drag-along with a reasonable threshold is market standard. Don't spend capital here.

Confidentiality of term sheet terms: Standard. Agree to it.

The negotiation posture that works

Come in with data, not complaints. Know the market rate for each term. Name what's non-market clearly and without apology. Prioritize: pick the two or three clauses that matter most economically and make those your focus. Trade movement on lower-priority terms to get concessions on the ones that change your actual economics at exit.

Common mistakes and what to do instead

Mistake 1: Celebrating the term sheet before reading it

Getting a term sheet is a meaningful milestone. It also starts a clock - the no-shop period - during which your leverage is highest before you know whether the deal will close.

Replace with: Read the term sheet in full before acknowledging receipt or sharing it internally. Identify the three clauses that most affect your economics. Have your lawyer review it within 24 hours. Then celebrate.

Mistake 2: Treating "non-binding" as "no stakes"

The no-shop clause is binding. Breaking it can result in legal action. It also burns the relationship with the investor and, in a market where VCs communicate freely, with others in their network.

The single biggest mistake founders make during this phase is letting alternative investor conversations drop entirely, which strips them of their competitive leverage and exposes them to late-stage price renegotiations.

Replace with: Treat the no-shop clause as a hard commitment. Only sign when you are prepared to stop other processes for the stated period. If you aren't ready to do that, don't sign yet.

Mistake 3: Negotiating valuation while ignoring liquidation mechanics

A $20M pre-money valuation with a 2x participating preferred provides far less founder upside in a $60M exit than a $16M pre-money valuation with a 1x non-participating preferred. The headline number is not the economics.

Replace with: Model the exit economics under each scenario before you compare offers. Run the math at a 1x exit (no proceeds above preference), a 3x exit, and a 10x exit. The structure matters most at the low and middle exit cases, which are statistically more common than 10x outcomes. Andreessen Horowitz's term sheet economics piece has worked examples showing exactly how participation changes founder proceeds across exit scenarios.

Mistake 4: Signing the term sheet before your data room is organized

Once the no-shop clause is signed, due diligence begins. If your data room isn't ready, you'll be assembling it under time pressure while also managing investor conversations, fielding questions, and negotiating final documents. The disorganized data room signals exactly the opposite of what you want to project at this stage.

Replace with: Build the data room to a close-ready standard before you start any fundraising outreach - not after you receive investor interest. That means monthly P&L for 24+ months, a three-year model with an explicit assumptions tab, channel-level CAC, cohort-level NRR, and a fully diluted cap table. Our due diligence checklist for startups covers the full document and metrics list by stage. For runway-specific model requirements, the startup runway calculation guide covers the net burn methodology investors expect to see.

Mistake 5: Conflating a term sheet with a commitment to close

A term sheet is an expression of intent. Deals fall apart after term sheets are signed. The most common reasons: diligence reveals undisclosed problems, the market moves and the investor reprices, or the legal process reveals unexpected complications in the cap table or IP ownership.

Replace with: Keep a parallel process running until the definitive documents are fully executed and the wire has cleared. That does not mean running a competing term sheet process after signing the no-shop - it means not standing down your internal momentum, your team communications, or your financial discipline until the money is actually in the bank.

The pre-signing checklist: before you execute a term sheet

Use this before you sign anything.

Financial readiness

- Monthly P&L for 24+ months is current and reconciles with bank statements

- Three-year financial model has an explicit assumptions tab with documented rationale per line

- CAC is broken out by channel - not blended only

- NRR and GRR are calculated with a documented, consistent cohort methodology

- Runway calculation uses net burn on a 3-month trailing average and ties to the model

- Scenario infrastructure: base case and downside case at minimum

- Cohort retention chart is available for the last 6-8 cohorts

For a complete view of what investors will stress-test in each of these areas - and the exact failure modes that slow or kill deals - see the due diligence checklist for startups. For SaaS-specific unit economics preparation, the SaaS unit economics guide covers gross margin, NRR, CAC, and LTV:CAC at the depth Series A investors expect.

Cap table and corporate

- Cap table is fully diluted - includes SAFEs, convertible notes, option pool, and warrants

- All prior financing documents are accessible: term sheets, SPAs, side letters

- Founder vesting agreements are executed and match what you'll represent in due diligence

- IP assignments exist for all founders, employees, and material contractors

- No unresolved verbal equity commitments or co-founder departures without clean paperwork

The cap table management guide includes a pre-raise cap table audit checklist covering ownership documentation, vesting gaps, stacked liquidation preferences, and the six structural problems investors most commonly find in diligence.

Term sheet review

- Legal counsel has reviewed the full document - not just the valuation and amount

- Liquidation preference multiple and structure (participating vs. non-participating) are understood and modeled

- Option pool expansion math has been run on a fully diluted basis

- Board composition post-close is clear, and you understand the implications

- No-shop period length and start date are explicitly noted

- Exclusivity clause has no ambiguous language about what activities it prohibits

- Protective provisions are reviewed for any non-standard clauses

Process

- You have a clear internal decision on whether to accept, negotiate, or decline before the deadline

- Key stakeholders (co-founders, existing lead investors) have been briefed

- Legal fees for drafting definitive documents are estimated and budgeted

Next step: Protect your exit before you sign

A term sheet is not a formality. It is the moment your deal is set. Everything after it - the diligence, the legal docs, the closing calls - is execution of what's already been agreed in principle.

The clauses that matter most economically are usually not the ones that generate the most founder anxiety. Valuation is visible and easy to compare. Liquidation preference structure, option pool mechanics, and board composition are less visible and more consequential over most exit distributions.

Go into the term sheet stage with your financial model documented, your cap table clean, and your priorities ranked. Know which terms are market standard, which are negotiable, and which would change your actual economics at exit. Model the downside scenarios, not just the upside.

The founders who close well are not the ones who negotiate hardest on every clause. They're the ones who negotiate precisely on the clauses that matter, treat counsel as a strategic asset rather than a deadline dependency, and enter the process with enough financial clarity that due diligence confirms the story rather than contradicting it.

If you're preparing for a Series A, Series B, or Series C round and want a structured review of your financial model, unit economics, and data room before you start outreach, book a working session with Fiscallion. We work with SaaS companies at $5–50M ARR to build the financial infrastructure that holds up when the term sheet arrives.