Most founders treat the cap table as a legal artifact - something to hand to counsel, file away, and revisit only when a new round forces the conversation. That framing is expensive.

The cap table is a forward-looking financial model in disguise. Every hire you make with equity, every SAFE you sign, every option pool you set before a term sheet - those decisions compound. They shape the ownership structure your Series A or B investor will see, the dilution math your board will debate, and the actual proceeds you receive at exit. Treating the cap table as documentation rather than a planning tool is a decision you make by default.

This guide gives you the framework to manage your cap table the way a CFO would: with scenario discipline, ownership assumptions made explicit, and a direct line from equity structure to capital allocation decisions.

What you'll learn

- How to read your cap table as a decision tool, not just a record

- The six structural mistakes that kill fundraising rounds - and when to fix each one

- How to model dilution scenarios before signing a term sheet, not after

- What a Series A investor actually checks in your cap table - and why it matters at your stage

- A pre-raise audit checklist you can use in the next 30 days

What the cap table actually is (and what it isn't)

A capitalization table records every ownership claim on your company - common shares, preferred shares, stock options, warrants, convertible notes, SAFEs, and any other security that converts to equity. It shows who owns what, at what price they came in, and under what conditions their stake could change.

Most people describe it as a spreadsheet. That is technically accurate and practically misleading.

Think of the cap table as a claims register on your company's future cash flows. Every row is a promise about who receives proceeds when the company is sold, merges, or goes public. The sum of those promises has to equal 100%. If you add more claims without increasing the total value, you are redistributing - not creating - ownership.

The three layers that matter for FP&A decisions

If your cap table doesn't give you clean answers on all three layers, it is not ready for a fundraising conversation.

How dilution compounds across rounds

The most common cap table mistake is treating each financing event in isolation. You sign a $250K SAFE at a $3M cap. You sign another at $5M. You close a pre-seed round. Then you start building a Series A pitch - and the math hits you all at once.

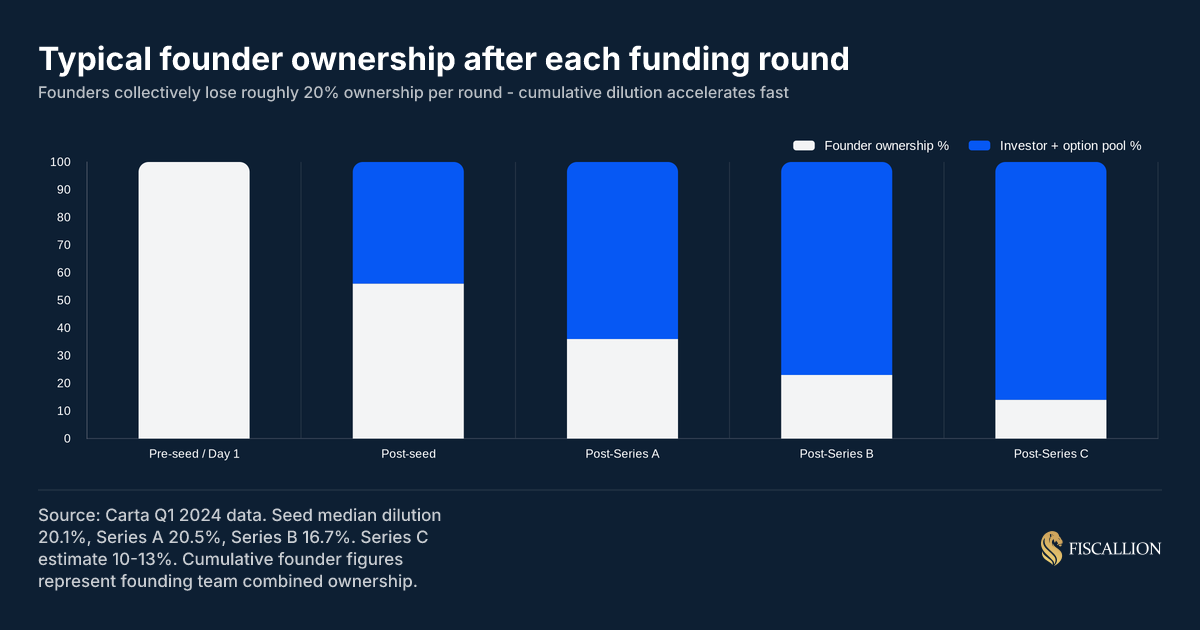

Carta's Q1 2024 data on median dilution by round makes the compounding effect concrete:

- Seed stage: founders give up roughly 20.1%

- Series A: another 20.5% dilution

- Series B: another 16.7%

- Series C: typically 10-13%

Cumulatively, a founding team that started at 100% ownership sits at approximately 56% after seed, 36% after Series A, and 23% after Series B. By Series C, you are often at 14% or below.

That dilution is not inherently a problem. A 14% stake in a $500M company is worth more than an 80% stake in a $10M company. The question is whether each dilutive event was priced correctly, sized intentionally, and modeled in advance.

SAFEs and convertible notes create invisible dilution

SAFEs feel cost-free at signing. No valuation negotiation, no board seat, no immediate change to the cap table. That is the problem.

A $200K SAFE at a $2M cap and a $400K SAFE at a $4M cap look manageable in isolation. At a $6M Series A priced round, both convert - and the combined dilution is larger than either note suggested when you signed it. Founders who didn't model this are surprised. Investors who did are not.

Y Combinator's standard SAFE documents are widely used precisely because they defer the valuation negotiation - but that deferral means the dilution calculation lands entirely at the priced round. Run your fully diluted cap table on the day you're considering each instrument, not the day you close it.

The option pool shuffle costs more than founders expect

VCs typically require a fresh employee option pool before closing a priced round - and that pool is created pre-money, which means it comes out of the existing shareholders (primarily founders), not from the new investor's capital.

Here's how the math works on a $5M pre-money deal:

- Stated pre-money valuation: $5M

- Required option pool: 15% of post-money

- Effective pre-money after pool creation: ~$4.25M

- Dilution from pool alone: ~15%, landing entirely on founders and early shareholder

Many founders evaluate term sheets based entirely on the headline valuation number without recognizing how severely an unmodeled option pool degrades their equity position. When this dilution calculation lands unexpectedly after a term sheet is signed, it leaves teams scrambling to claw back critical percentage points.

Size your option pool against a specific 18-24 month hiring plan before you enter term sheet conversations. Y Combinator's Series A term sheet guidance is explicit that the pool size is a negotiated point - a forward-looking hiring plan is your best argument for keeping it smaller than the investor's opening ask.

The six structural problems investors find in diligence

These are not edge cases. They appear in a meaningful share of Series A diligence processes.

Problem 1: Over-dilution before product-market fit

The pattern: founders raise multiple small rounds from angels, sign several SAFEs, grant advisor equity generously, and arrive at Series A with combined founder ownership below 20%.

The threshold most institutional Series A investors use is 15-25% combined founder ownership at closing. Below that, incentive alignment becomes a concern. Future dilution from the A round, a B round, and option pool expansions will push founders toward single digits before any exit.

Fix: model your ownership floor before you accept the first check, not the second.

Problem 2: Vesting gaps and departed co-founders

Standard institutional vesting is a 4-year schedule with a 1-year cliff. Andreessen Horowitz's primer on startup options is worth reading in full here - it explains exactly why vesting schedules exist and what happens to alignment when they're missing or poorly structured. When vesting is absent - or when a co-founder departed without a repurchase provision - investors see dead equity: ownership held by someone who is no longer driving value.

Assuming your initial legal paperwork is inherently clean is a dangerous trap that often completely unravels during institutional diligence. Uncovering ambiguous or un-papered vesting logic weeks before a scheduled close can entirely derail a growth round.

A single departed co-founder with unvested equity and no repurchase rights can block a Series A or force a repricing. Retrofitting vesting is possible, but it requires board approval and co-founder consent - a harder conversation six weeks before a close.

Fix: if your founding team lacks standard vesting agreements, start the process now. Do not wait for a term sheet.

Problem 3: Too many early investors with pro-rata rights

Pro-rata rights give existing investors the option to maintain their ownership percentage in future rounds. Thirty small seed investors each claiming a $40K pro-rata allocation fragments the Series A round before the lead investor reaches their target ownership.

Most institutional funds need to deploy meaningful capital. If your round is crowded with micro pro-rata claims, the lead investor either passes or demands a clean-up round first. The NVCA Model Term Sheet - the industry standard template - clarifies exactly how pro-rata provisions are typically structured and when they can be waived.

Fix: keep early investor count manageable (10-15 at seed is workable). Consolidate rights through one lead and avoid side letters that grant individual protective provisions.

Problem 4: Missing or unsigned legal documentation

An accurate number on a spreadsheet means nothing if the paperwork behind it does not exist. Common gaps:

- Stock purchase agreements not signed by all parties

- Board consents missing for equity grants

- 83(b) elections not filed within the 30-day window after restricted stock grants

- Equity promised over email with no signed agreement

The 83(b) issue deserves specific attention. Under IRC Section 83(b), you have exactly 30 days from the grant date to make the election with the IRS. Miss that window and each vesting event becomes a taxable moment - the tax bill arrives years later, at the worst possible time, and investors treat it as a governance failure. Morrison & Foerster's 83(b) explainer for founders walks through exactly how the election works and the cost of missing it.

Fix: run a documentation audit at least six months before you fundraise. Pull every grant agreement, board consent, and 83(b) filing. Confirm each is signed and dated. Bring your startup lawyer into this process - and pair it with the due diligence checklist framework so legal documentation is reviewed alongside your financial data room.

Problem 5: Stacked liquidation preferences

Participating preferred stock lets investors take their liquidation preference first, then share in remaining proceeds alongside common shareholders. Stack a 2x or 3x participating preferred from an early investor with a standard 1x from a later investor, and exit math for common shareholders and new investors gets complicated fast.

A Series A investor modeling a $30M exit scenario on your cap table will see how much of those proceeds get absorbed before they receive a return. If the answer is "most of it," they will pass or demand restructuring. This interacts directly with your 409A valuation - a heavy liquidation preference stack compresses common stock FMV and affects every option grant you make.

Fix: build a waterfall model before you pitch any priced round. Run exit scenarios at $20M, $50M, and $100M. If common shareholders receive less than 40% of proceeds at a mid-range exit, review which preferences are negotiable.

Problem 6: Using a spreadsheet past the point where it is reliable

A spreadsheet has no audit trail, no version control, and no automatic enforcement when a new option grant is issued. One formula error in a shared Google Sheet can misrepresent your ownership structure to an investor - and you may not catch it until their counsel does.

Dedicated equity management platforms resolve this at scale. They track every share class, grant, and transfer, run vesting schedules automatically, and let you model round scenarios in minutes rather than rebuilding a spreadsheet from scratch each time.

The platforms worth knowing at the $5-50M ARR stage:

The right platform is less about features and more about which one your legal counsel and lead investor can access cleanly during diligence.

How to use the cap table as an FP&A planning tool

Most founders check the cap table before fundraising and after fundraising. The FP&A use case is different: you use it continuously, before every material equity decision, to model the downstream ownership and governance implications.

Scenario modeling before each round

Before you begin any fundraising process, run at least three dilution scenarios:

- Base case: raise the target amount at your expected valuation

- Lower valuation: what your ownership looks like if you raise at 20-30% below your target

- Bridge scenario: what a small extension round does to the cap table before a priced round closes

Each scenario should show post-money founder ownership, post-money option pool size, and the ownership threshold of any new investor. If the lower valuation scenario puts founders below 15% combined, that is a planning constraint, not a surprise to encounter in the term sheet. For context on what bridge financing actually does to your cap table versus your cash position, the venture debt analysis covers the dilution and covenant math in detail.

Option grant modeling against the hiring plan

Every option grant reduces the available pool. The pool size affects dilution calculations for the next round.

A forward-looking grant model should show:

- Current pool size (authorized minus issued)

- Grants expected over the next 12 months, mapped to open roles

- Remaining pool after those grants

- Implied option pool expansion need at the next round, and the dilution that creates

This is not complex to build. It is a simple table. But without it, option grants are made ad hoc, and the pool is a black box until a term sheet surfaces the problem.

The cap table and your runway are connected

A raise extends runway - but the dilution cost of that runway extension is the price you pay. If your current runway forecasting model treats a future raise as a simple cash injection, you are missing the equity side of the trade.

The more complete framing: each financing event is a transaction where you exchange equity for cash. The price of that cash is the dilution you accept. Your job, as the decision-maker, is to ensure the cash is deployed against opportunities that return more value than the dilution cost - and that the board can see that math explicitly.

Startup runway calculation done well doesn't just tell you how many months you have - it models the dilution cost of each potential financing event against the milestones that cash enables. That is the runway-versus-dilution trade-off that makes the capital allocation decision visible to your board.

This connects directly to the kind of FP&A work that scaling SaaS companies often lack: not just runway forecasting in months, but runway-versus-dilution trade-off modeling that makes the capital allocation decision visible. At Fiscallion, this is where fractional CFO-level support adds real value - building the model that connects cap table decisions to growth scenarios, rather than treating them as separate conversations.

Pre-raise cap table audit checklist

Run this six months before you plan to start fundraising. Every item that comes back incomplete is a problem you can fix now, before it costs you a term sheet. This checklist complements the broader investor due diligence checklist - the two should be run in parallel, not sequentially.

Ownership and documentation

- Every issued share has a signed stock purchase agreement on file

- All equity grants have board consent resolutions

- 83(b) elections filed within 30 days for every restricted stock grant

- No equity promised by email without a signed agreement

- Departed co-founders either have fully vested shares or signed repurchase agreements

Vesting and governance

- All founding team members have standard 4-year / 1-year cliff vesting

- Any co-founders who departed have had their unvested shares addressed

- Board and investor consent rights are documented in your investor agreements

- Side letters are inventoried - check for blocking rights and pro-rata obligations

Structure and modeling

- Fully diluted share count reconciles with all issued shares + option pool + unconverted SAFEs/notes

- Liquidation preference stack is modeled at three exit scenarios ($20M, $50M, $100M)

- Option pool has at least 12-18 months of grants available at current hiring pace

- A clean cap table summary (not the full working file) is prepared for investor sharing

- Your cap table lives in dedicated software, not a manually maintained spreadsheet

Investor profile review

- Total investor count reviewed - if above 20-25 at seed, understand consent process implications

- Pro-rata rights inventoried - model the impact on next round allocation

- Any investors with information rights or approval rights identified

Common mistakes and the replacement move

What good cap table management looks like at each stage

Pre-seed to seed

Keep the structure as simple as possible. Common shares for founders, a straightforward SAFE structure for early investors, and a clearly sized option pool. Document everything. File every 83(b). Do not issue equity to advisors or early contractors without signed agreements and vesting terms.

The goal at this stage is not optimization - it is clean formation. Every shortcut you take before product-market fit creates a clean-up cost before your Series A. Seed round financial projections and cap table structure are built at the same time - if your financial model assumes a clean equity stack but your cap table has four SAFEs with different caps and discount rates, those two documents are already contradicting each other.

Series A ($5-25M ARR range)

This is where cap table management becomes a material fundraising factor. Institutional investors will open your cap table before your deck in many cases. They are running three calculations immediately: post-money dilution, their projected return at a realistic exit, and how much of the company actually produces that return.

Your cap table should be in dedicated software, fully documented, and modeled out through at least the B round. A scenario model showing post-A and post-B founder ownership, investor ownership, and option pool size signals that you are running this company like a financial decision-maker, not just a builder. At this stage, the cap table is also a direct input to your 409A valuation - every new round, option grant, and preference structure affects the FMV calculation your valuation provider runs.

Series B and beyond ($25M+ ARR)

By Series B, your cap table is a complex legal document with multiple preferred share classes, liquidation preferences to manage, and a governance structure that affects every major decision. The management challenge shifts from documentation to ongoing scenario planning.

At this stage, the cap table is an input to your board reporting. Every capital allocation decision - a new acquisition, a secondary transaction, a down-round bridge - has cap table implications that need to be modeled before the decision is made, not after the term sheet arrives. Your burn rate and burn multiple analysis

Treat the cap table as a planning tool and the fundraising conversation changes

The cap table is not a filing. It is a forward model of who gets paid and how much, under every scenario you are likely to face.

Managing it well means three things: keeping it structurally clean (documented, vested, in proper software), modeling dilution proactively before each financing event rather than reacting to it, and connecting cap table decisions to the broader trade-offs your business faces - runway, headcount, and growth rate.

Most of the structural problems that slow or kill fundraising rounds are fixable. The catch is that fixing them proactively costs weeks. Fixing them reactively, mid-diligence, costs months and sometimes the deal itself.

Run the audit. Build the scenarios. Treat the cap table as a planning tool. That discipline is what separates a founder who arrives at a term sheet conversation in control of the conversation from one who is learning the math for the first time.

If you want to build the scenario model that connects your cap table decisions to runway, growth, and capital allocation trade-offs, book a working session with Fiscallion.