Ownership percentage and exit proceeds are not the same number. Most founders find this out late — after a $60M acquisition that felt like a win until the waterfall ran and common shareholders received less than half of what their cap table stake implied.

Liquidation preference is the clause that creates that gap. It is the single most economically consequential term in a venture term sheet, and the one most commonly misunderstood, undermodeled, or negotiated in isolation from the exit math that determines whether it actually matters.

This article gives you the framework to read, calculate, and negotiate liquidation preferences the way a CFO would: with scenario discipline, explicit trade-offs, and decisions grounded in the actual distribution of realistic exits — not the $500M outcome that makes every structure look the same.

Key takeaways

- 1x non-participating preferred is market standard at Series A. Anything above 1x multiple, or any fully participating structure, requires explicit exit modeling before you accept it.

- The participation right is often more expensive than the multiple. A 1x participating preferred can cost founders more at a mid-range exit than a 2x non-participating preferred.

- Liquidation preferences stack across rounds. Evaluating each round's terms in isolation is the primary mistake. The cumulative preferred overhang is what determines how much common equity is actually worth.

- Model three exit scenarios before you sign. The structure that looks acceptable at a $300M exit looks very different at a $40M exit — which is statistically where most venture-backed companies end up if they exit at all.

What we'll cover

- What liquidation preference is and why it exists

- The four structures and how they differ

- How to calculate the waterfall — with worked examples

- What triggers a liquidation preference

- What a 3x preference actually means in practice

- How stacked preferences compound across rounds

- Is 1% equity in a startup good? The ownership context question

- How to negotiate — what moves and what doesn't

- Common mistakes and the replacement moves

- A pre-signing waterfall checklist

What liquidation preference is — and why it exists

Liquidation preference is a provision in preferred stock that gives investors the right to receive a specified return on their investment before common shareholders receive anything in a liquidity event.

It exists because preferred investors — VCs, institutional funds — are buying equity at a fixed valuation. If the company sells for less than that valuation (or even modestly above it), the investor loses money on a straight percentage-of-proceeds basis. Liquidation preference is downside protection: a floor that guarantees the investor gets some portion of their capital back before founders and employees see a dollar.

That framing is accurate. What it omits is the other side: in a mid-range exit scenario, the same clause that protects a $10M investment can absorb most of the proceeds before common shareholders participate at all.

The key point is not whether liquidation preference is fair. It is standard market infrastructure in venture deals. The key point is that its economic impact on founders varies enormously across structures — and modeling that impact is not optional if you want to make informed decisions when you negotiate. As Carta's overview of liquidation preferences notes, rights and preferences are classified as either "standard" or "non-standard" — and knowing which category each term falls into is the starting point for any negotiation.

The four structures you need to understand

The difference between participating and non-participating preferred is the most impactful variable in most term sheets. It is not always the most negotiated one.

How to calculate the liquidation waterfall

The mechanics are straightforward once you have the right inputs. The complexity comes from modeling across scenarios, not from the formula itself. Carta's waterfall analysis guide describes the process well: a waterfall model combines your cap table with the payout terms in your certificate of incorporation and lets you stress-test different exit valuations against those rules.

The inputs you need

- Total invested capital per round (including all rounds with preferred outstanding)

- Liquidation multiple per round (1x, 1.5x, 2x, etc.)

- Participation rights per round (participating vs. non-participating)

- Participation cap, if any (e.g., investors participate until they've received 3x total)

- Seniority order (which round gets paid first)

- Fully diluted common and preferred ownership percentages at exit

The basic waterfall formula

Step 1: Calculate the liquidation preference for each preferred round.

Liquidation preference = Investment amount × Liquidation multiple

Step 2: Determine seniority. Most recent rounds are typically senior to earlier rounds (Series B senior to Series A, Series A senior to Seed). Some deals use pari passu — pro-rata across rounds — instead of strict seniority.

Step 3: Pay out preferences in seniority order until either:

- All preferences are satisfied, and remaining proceeds go to common (in a non-participating structure), or

- All preferences are satisfied, and investors also participate in remaining proceeds pro-rata (in a participating structure)

Step 4: If exit proceeds are insufficient to cover all preferences, proceeds are split proportionally based on each round's share of total outstanding preferences (in a pari passu structure) or paid in strict order until funds run out.

Worked example: 1x non-participating preferred

Company cap table at exit:

- Raised $10M at Series A. Investors hold 30% fully diluted.

- Founders and employees hold 70% fully diluted.

- Series A has a 1x non-participating preference.

Exit at $20M:

- Investor preference: $10M × 1x = $10M

- Remaining for common: $20M - $10M = $10M

- Investor choice: take $10M preference, or convert to common and take 30% × $20M = $6M

- Investor takes preference: $10M

- Founders + employees: $10M

Exit at $40M:

- Investor preference: $10M

- Investor choice: take $10M, or convert and take 30% × $40M = $12M

- Investor converts to common: $12M

- Founders + employees: 70% × $40M = $28M

The conversion threshold — the exit price at which an investor switches from taking their preference to converting to common — is: Investment ÷ Ownership % = $10M ÷ 0.30 = $33.3M. Below that, the investor stays in preferred. Above it, they convert.

Worked example: 1x participating preferred

Same cap table. Now the Series A has 1x participating preferred.

Exit at $40M:

- Investor takes preference first: $10M

- Remaining proceeds: $30M

- Investor also participates pro-rata in remainder: 30% × $30M = $9M

- Total investor proceeds: $10M + $9M = $19M

- Founders + employees: $30M - $9M = $21M

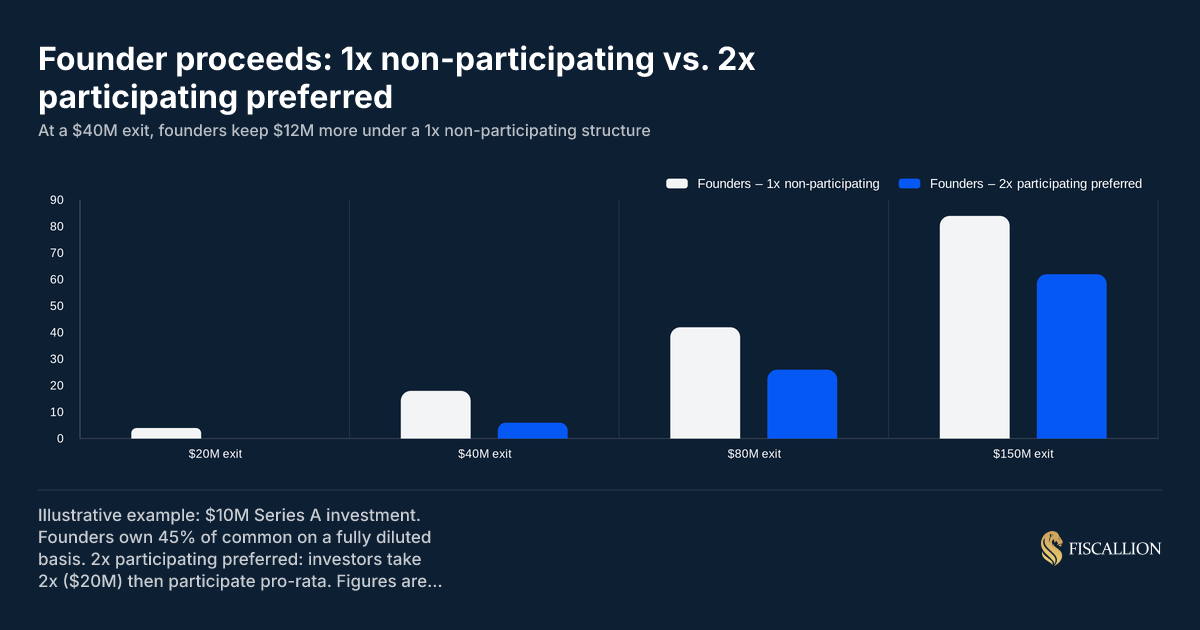

Compare that to the non-participating outcome at $40M: founders received $28M with a 1x non-participating structure, versus $21M with 1x participating. The participating right cost founders $7M on a $40M exit — from the same headline "1x" liquidation preference.

Worked example: 2x participating preferred

Same cap table. Series A now has 2x participating preferred.

Exit at $40M:

- Investor preference: $10M × 2 = $20M

- Remaining proceeds: $20M

- Investor participates pro-rata in remainder: 30% × $20M = $6M

- Total investor proceeds: $20M + $6M = $26M

- Founders + employees: $14M

At a $40M exit, founders receive $14M with a 2x participating structure versus $28M with a 1x non-participating structure — a 50% reduction in proceeds from one term change.

What triggers a liquidation preference

Liquidation preference is triggered by a "liquidation event" — which in most term sheets is defined broadly enough to include events that are not what most people think of as a "liquidation."

The typical definition covers:

- Dissolution or winding up of the company (actual liquidation)

- Sale of the company — including an asset sale or merger where existing shareholders receive less than 50% of the voting power of the surviving entity

- Acquisition — any transaction where a third party acquires more than 50% of the company's outstanding voting shares

This means a standard M&A acquisition triggers liquidation preference. An IPO typically does not — preferred shares convert to common automatically at IPO under most standard terms, making the liquidation preference irrelevant in a genuine public offering. The NVCA model legal documents — the industry's standard template for venture financing — define this conversion mechanism explicitly and are worth reviewing alongside any non-standard term sheet you receive.

There is an important wrinkle here for SaaS founders doing secondary transactions or structured deals: some term sheets define "deemed liquidation" broadly enough to capture transactions that are not full exits. Read your specific definition carefully before you structure any transaction that involves a transfer of voting control.

What does not trigger a liquidation preference

- Raising a new equity round (this dilutes ownership but doesn't trigger the payout mechanism)

- Taking on venture debt (no equity transaction, no trigger)

- Revenue-based financing

- Standard employee equity grants

- An IPO (preferred converts to common automatically)

What a 3x liquidation preference means

A 3x liquidation preference means the investor receives three times their invested capital before any common stockholder receives proceeds.

On a $10M investment, the investor must receive $30M before founders, employees, or common shareholders see a dollar.

A 3x preference is not market standard at Series A. It appears most commonly in:

- Down rounds or structured bridge financing where investors are taking on higher perceived risk

- Late-stage growth rounds (Series C, D, E) done at high valuations — particularly in environments where public market comps are falling

- Distress capital where investors have negotiated heavily investor-favorable terms in exchange for saving a company from closure

The economic impact of a 3x preference depends entirely on whether it is participating or non-participating, and on the exit scenario.

3x non-participating at $50M exit (on $10M invested)

- Preference: $30M

- Investor choice: take $30M, or convert to 30% common = $15M

- Investor takes preference: $30M

- Founders + employees: $20M

3x participating at $50M exit (on $10M invested)

- Preference: $30M

- Remaining: $20M

- Investor participates: 30% × $20M = $6M

- Total investor: $30M + $6M = $36M

- Founders + employees: $20M - $6M = $14M

At a $50M exit on a $10M raise, 3x participating preferred leaves founders with less than 28% of proceeds despite owning 70% of the fully diluted cap table.

This is not a negotiating abstraction. It is a structural reality that Fiscallion has seen play out in the financial models of companies in the $10–30M ARR range that raised bridge capital under distress conditions without running the waterfall before signing.

Participation caps as a middle ground

Some term sheets include participation caps: investors participate in common equity proceeds until they have received a total return of 2x or 3x their investment (including the preference). Once the cap is hit, the remaining proceeds go to common.

A 3x participating preferred with a 3x total cap means: investors receive their preference plus pro-rata participation, but stop at a 3x total return. Above that threshold, common shareholders benefit from the excess.

This is a meaningful structural concession if you cannot move the investor off participating preferred entirely. It limits the "double dip" at larger exit values. Carta's breakdown of capped vs. uncapped participation shows clearly how the cap changes the payout curve across different exit sizes — worth reviewing before you accept any participating structure without one.

An example of a liquidation preference in practice

Here is a realistic scenario a SaaS founder encounters at Series B.

Company:

- $18M ARR, growing 80% year-over-year

- Raised $3M seed (1x non-participating, investors hold 12%)

- Raised $12M Series A (1x non-participating, investors hold 22%)

- Now closing $25M Series B

Series B term sheet: 1x participating preferred, no cap. Series B investors will hold 28% post-round.

Post-round fully diluted ownership:

- Series B investors: 28%

- Series A investors: 16% (post-dilution)

- Seed investors: 9% (post-dilution)

- Founders and employees: 47%

Exit scenario: acquired for $80M (roughly 4.4x ARR)

Waterfall (assuming Series B is senior):

- Series B preference: $25M × 1x = $25M. Remaining: $55M

- Series A preference: $12M × 1x = $12M. Remaining: $43M

- Seed preference: $3M × 1x = $3M. Remaining: $40M

- All preferred investors have taken their preference (Series A and Seed are non-participating, so they now evaluate: convert or keep preference?)

- Series A conversion value: 16% × $80M = $12.8M vs. preference of $12M → converts to common

- Seed conversion value: 9% × $80M = $7.2M vs. preference of $3M → converts to common

- Series B investors participate in remaining $40M pro-rata: 28% × $40M = $11.2M

- Series A (converted): 16% × $40M = $6.4M

- Seed (converted): 9% × $40M = $3.6M

- Founders and employees: 47% × $40M = $18.8M

Total proceeds:

- Series B: $25M + $11.2M = $36.2M (45% of total proceeds on 28% ownership)

- Series A: $18.8M (6% uplift over preference due to conversion)

- Seed: $10.2M (3.4x return)

- Founders + employees: $18.8M (23.5% of total proceeds on 47% ownership)

The founders and employees own 47% of the cap table and receive 23.5% of proceeds. The Series B participating preferred structure transferred roughly $10M from founders to investors compared to a 1x non-participating structure.

That $10M is not a hypothetical. It is the cost of signing the term sheet without running the waterfall first.

How stacked preferences compound across rounds

Evaluating each round's liquidation preference in isolation is the most common and costly mistake in this area.

By Series B, most startups have three rounds of preferred outstanding. Each round has its own preference, participation rights, and seniority. The cumulative effect can mean that a company needs to sell for a specific minimum exit value before common shareholders receive any proceeds at all.

The preference overhang is the total amount that must be paid to preferred shareholders before common equity sees a dollar. At the point where a single investor's 2x preference plus participating rights absorb more than 60% of a mid-range exit, common shareholders hold an option — not an asset.

When this structural tipping point is crossed, the impact shifts from a modeling problem to a cultural crisis. Option-holding employees can sense when their equity has been pushed into a statistical tail event, and trying to manage that reality with generic encouragement will backfire.

This interacts directly with your equity dilution model. As covered in Fiscallion's analysis of equity dilution in startups, ownership percentage and economic outcome are not the same number. The cap table percentage is what you negotiate. The waterfall output is what you receive.

The practical implication: before signing any round that adds to the preference stack, run the full waterfall at three exit scenarios — $50M, $150M, and $300M — and evaluate what percentage of proceeds reaches common at each. If common equity receives less than 40–50% at your most likely exit scenario, that is a signal to negotiate the structure, not just the valuation.

Is 1% equity in a startup good? The ownership context question

This is a common question, and the correct answer is: it depends entirely on the exit math, not the percentage.

1% equity in a startup could be worth:

- Zero, if the company is sold at a price below the total liquidation preferences outstanding

- $300K, if the company sells for $50M and liquidation preferences absorb 40% of proceeds — leaving $30M for common, and 1% of that is $300K

- $3M, if the company sells for $400M and preferred has already converted to common at IPO or high-exit threshold

- $10M+, if the company reaches IPO at a multi-billion valuation

The percentage itself is not the variable that drives the outcome. The two variables that determine what 1% is worth are:

- Total exit value — the proceeds from the sale or IPO

- The liquidation stack — how much preferred capital sits above common equity, and whether it is participating

A 1% stake in a company with $50M of 2x participating preferred outstanding is worth functionally nothing in most realistic exit scenarios below $150M. The same 1% stake in a company with 1x non-participating preferred is worth meaningfully more at a $60M exit.

This is the lens through which startup equity offers should be evaluated — particularly for employees, advisors, and early common shareholders who are below the liquidation waterfall. The ownership percentage without the waterfall context is not a complete picture. Fiscallion's cap table management guide covers how to build and maintain the model that keeps this picture accurate as new rounds close.

What this means when you receive an equity offer

Before you evaluate or offer equity, build the waterfall — not just the cap table.

How liquidation preferences interact with your 409A valuation

There is a less discussed but practically important connection between liquidation preferences and your 409A valuations.

A heavy liquidation preference stack suppresses the fair market value (FMV) of common stock. This is intentional in the 409A methodology: the valuation provider accounts for the fact that common shareholders are subordinate to preferred in the exit waterfall, which reduces the present value of the common equity position.

This means that more aggressive liquidation preference structures result in lower 409A FMV, which produces lower option strike prices for employees. From an employee perspective, that can appear attractive. From a company perspective, it creates a structural misalignment between the option strike price and the real economic value of the equity — which becomes visible at exit.

As covered in the 409A valuation guide for startups, liquidation preference structures are a primary input to the option allocation models that determine FMV. If your preference stack changes materially between annual 409A updates, the impact on employee option economics can be significant.

How to negotiate liquidation preference: what moves and what doesn't

Terms that typically move with clear rationale

Liquidation multiple: 1x is market standard at Series A. If you receive 1.5x or 2x, push back explicitly. Name it as non-market and provide comparable deal references. Moving from 2x to 1x on a $10M raise can represent millions of dollars in founder proceeds at a realistic exit.

Participating vs. non-participating: Fully participating preferred is the most expensive structural concession and the one with the highest return on negotiating effort. Push for non-participating at every round. If the investor won't move fully, propose a participation cap at 2x or 3x total return — this limits the downside without eliminating investor flexibility. Scott Kupor of a16z explains this dynamic clearly: the participation right is often where the most meaningful economic negotiation happens, even though founders frequently focus attention elsewhere.

Participation cap: If you cannot get non-participating, negotiate the cap down to 2x rather than accepting an uncapped participating structure. The cap means investors participate until they've earned a 2x total return (preference plus participation combined), then stop.

Seniority structure: In later rounds, investors will push for their round to be senior to all prior rounds. This is standard but not unconditional — in some cases, pari passu across all rounds is achievable and preferable if you have strong negotiating leverage.

Terms that rarely move

1x non-participating preference for a lead investor: If you have already negotiated to this structure, don't push further. 1x non-participating is market standard and the outcome to lock in.

ROFR and co-sale rights: Universal in VC deals for structural reasons. Not worth negotiating capital on this.

Standard drag-along provisions: Market standard. Accept them.

The negotiation posture that works

Come in with a modeled waterfall, not just a position. Show the investor three exit scenarios and where each structure produces. This reframes the negotiation from a positional argument ("we want non-participating") to a data-informed trade-off conversation ("at a $50M exit, participating preferred means we receive X versus Y — we'd like to find a structure that works for both sides at realistic exit scenarios").

Investors who model exits understand this framing. Those who push back on it are signaling something about their assumptions around your outcome range.

According to Aleksandar Stojanovic, CEO & Founder at Fiscallion, when a founder has their back against the wall in a restrictive market, the solution is to unbundle the investor's terms and negotiate on the specific dimensions of the preference. "An investor pushing 2x participating with strict seniority is often really asking for downside protection; a 1x participating with a 3x cap and pari passu can deliver most of that protection while preserving far more common upside," Stojanovic points out.

By offering structured middle grounds—like a participation cap where common equity catches up or pivoting to a pari passu structure alongside previous backers—founders can isolate the investor's core risk management goals while stripping away the excessive negotiating margin that would destroy the common equity tier.

As covered in the Fiscallion term sheet guide for startups, liquidation preference structure and valuation together represent the majority of substantive economic negotiation in a term sheet. Most founders focus on valuation and accept the preference structure as given. The trade-off runs in the other direction: a lower valuation with clean preference terms often produces better founder economics than a higher valuation with aggressive preference terms.

Common mistakes and the replacement moves

Mistake 1: Treating "1x" as the whole story

A 1x liquidation preference sounds minimal. A 1x participating preference is not minimal — it means the investor gets their money back and participates in upside, effectively taking a double dip on every dollar of proceeds.

Replacement move: Always read both the multiple and the participation right as a combined term. Model the combined effect at three exit values before you assess whether the structure is acceptable.

Mistake 2: Evaluating each round's preference in isolation

A round 3 term sheet that adds another $20M of 2x participating preferred to a cap table that already has $15M of 1x non-participating outstanding does not just create a "$20M problem." It creates a $40M preference overhang above common equity.

Replacement move: Build a cumulative preference stack model before every new round. The relevant question is not "what does this round's preference look like?" It is "what does the total preference overhang look like, and at what exit price does common equity start receiving meaningful proceeds?" Fiscallion's pre-money vs. post-money valuation guide walks through exactly this type of cumulative modeling in the context of term sheet evaluation.

Mistake 3: Accepting a participation cap without modeling it

Participation caps sound like a founder-friendly concession. They are — relative to uncapped participating preferred. But a 3x cap on a 2x participating preference on a $20M raise means investors participate until they've received $60M total. On a $100M exit, that cap may not bind at all.

Replacement move: Model the cap against your realistic exit range. If your most likely exit is $80M and the cap doesn't bind until $90M, the cap provides no meaningful protection. Negotiate the cap at a level that actually binds within your realistic exit scenarios.

Mistake 4: Not knowing the conversion threshold before negotiating

The conversion threshold — the exit value at which investors convert from preferred to common — determines when your ownership percentage starts mattering. For a 1x non-participating preferred, the threshold is: Investment ÷ Investor Ownership %. For any preference structure above 1x, the threshold is higher.

If you are negotiating valuation without knowing this number, you are negotiating the wrong variable.

Replacement move: Calculate the conversion threshold for every preferred round on your cap table. This is the minimum exit value at which your ownership percentage starts translating to proceeds. Make sure your target exit scenario clears every threshold on the stack.

Mistake 5: Using ownership percentage to evaluate equity offers without the waterfall

This affects both how founders evaluate their own economic stake and how they structure equity offers to employees and advisors.

Replacement move: Build a simple waterfall model and include it in your equity offer context — internally and with key hires. The waterfall is what determines actual proceeds, not the cap table percentage.

Waterfall modeling checklist — run this before every signing

Use this before you sign any term sheet that adds to or modifies your liquidation preference stack.

Step 1: Map the full preference stack

- List every preferred round outstanding with: investment amount, liquidation multiple, participation rights, participation cap (if any), seniority order

- Calculate total preference overhang: sum of (investment × multiple) for all rounds

- Identify the conversion threshold for each round

Step 2: Run three exit scenarios

Run the waterfall at:

- 1x on invested capital (a disappointing but realistic exit)

- 3–5x on invested capital (a solid but not exceptional outcome)

- 10x+ on invested capital (a strong outcome)

For each scenario, calculate:

- Total investor proceeds by round

- Total common shareholder proceeds

- Common shareholder proceeds as a percentage of total exit value

- Founder proceeds specifically (not lumped with all common)

Step 3: Evaluate the new round terms in context

- Add the proposed new round's preference to the existing stack

- Re-run the three scenarios with the new structure

- Identify the exit value at which common shareholders receive at least 40–50% of proceeds

- Compare that threshold to your realistic exit distribution

Step 4: Identify which terms to negotiate

- Flag any multiple above 1x — negotiate down

- Flag any participating structure — push for non-participating or participation cap

- Flag any seniority structure that puts the new investor ahead of all existing rounds — evaluate pari passu alternatives

Step 5: Know your floor before you enter the conversation

- Identify the minimum acceptable structure that keeps common shareholder proceeds above your threshold at a mid-range exit

- Separate this analysis from valuation negotiation — they interact, but they are not the same variable

- Document your assumptions so they can be reviewed and updated as terms change during negotiation

Shifting from cap table valuation to scenario discipline

Liquidation preference is not a fine-print technicality. It is the mechanism that determines whether the ownership percentage on your cap table translates to actual cash at exit — and in most moderate exit scenarios, the participation structure matters more than the multiple, and the cumulative stack matters more than any single round.

The founders who are most protected against preference-related economic surprises are not the ones who negotiated hardest on every term. They are the ones who modeled three exit scenarios before every signing, understood the conversion threshold for each round, and treated the waterfall — not the cap table — as the financial document that actually governs their outcome.

Building that model takes one afternoon. Not building it before a Series A, Series B, or structured bridge can cost millions in exit proceeds.

If you are preparing for a fundraising round and want a structured review of your liquidation stack, exit waterfall, and the negotiating trade-offs in your specific term sheet, book a working session with Fiscallion. We work with SaaS companies at $5–50M ARR to build the financial infrastructure that holds up when the term sheet arrives — and the models that make the preference conversation a data exercise rather than a guess.