A startup exit strategy is not a slide you build the year before you sell. It is a set of financial decisions you make years earlier: how you price, how you hire, which metrics you protect, and how disciplined your forecasting is when nobody outside the company is watching. By the time a banker or acquirer asks for diligence materials, your exit outcome is already largely determined by the finance infrastructure you built beforehand.

This article gives you the framework Fiscallion uses when advising $5-50M ARR SaaS companies on exit readiness: what an exit strategy actually is, how to calculate exit readiness and a valuation range, how to interpret where you stand today, and the specific FP&A moves that separate a founder who controls their exit timeline from one who gets forced into a rushed sale.

Key takeaways

- A startup exit strategy is a plan for how equity holders convert ownership into cash or liquid stock. The four common paths are acquisition (M&A), IPO, acquihire, and private equity buyout or secondary sale.

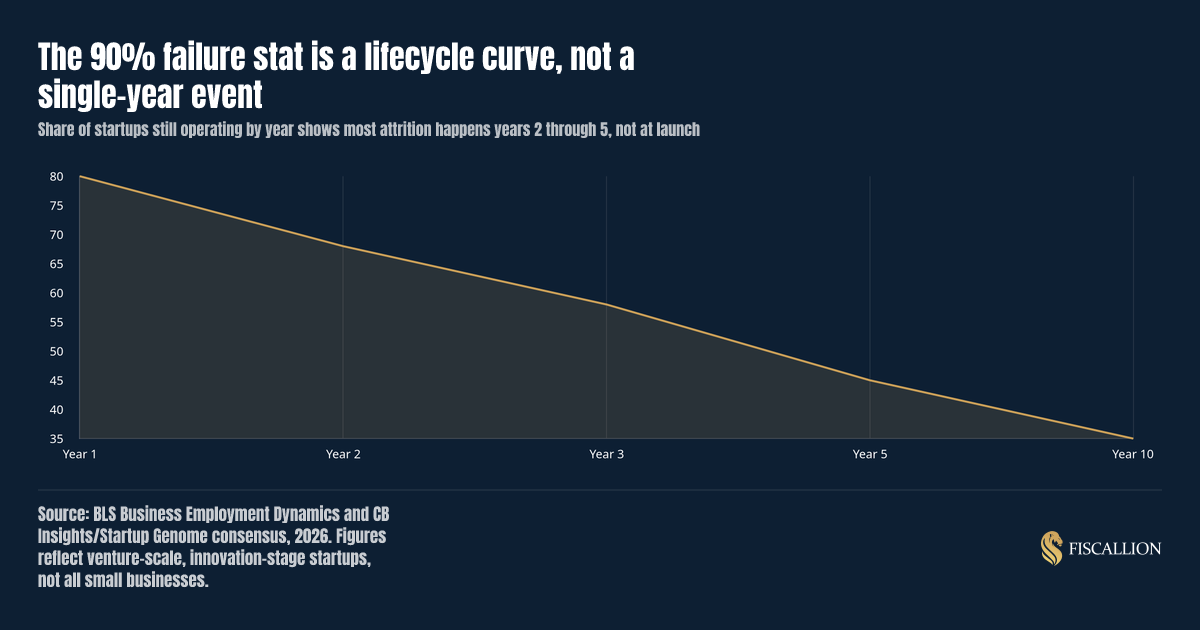

- The "90% of startups fail" statistic is real but misleading without context. It applies to venture-scale companies across a full lifecycle, not to a well-run SaaS business at $5-50M ARR with positive unit economics.

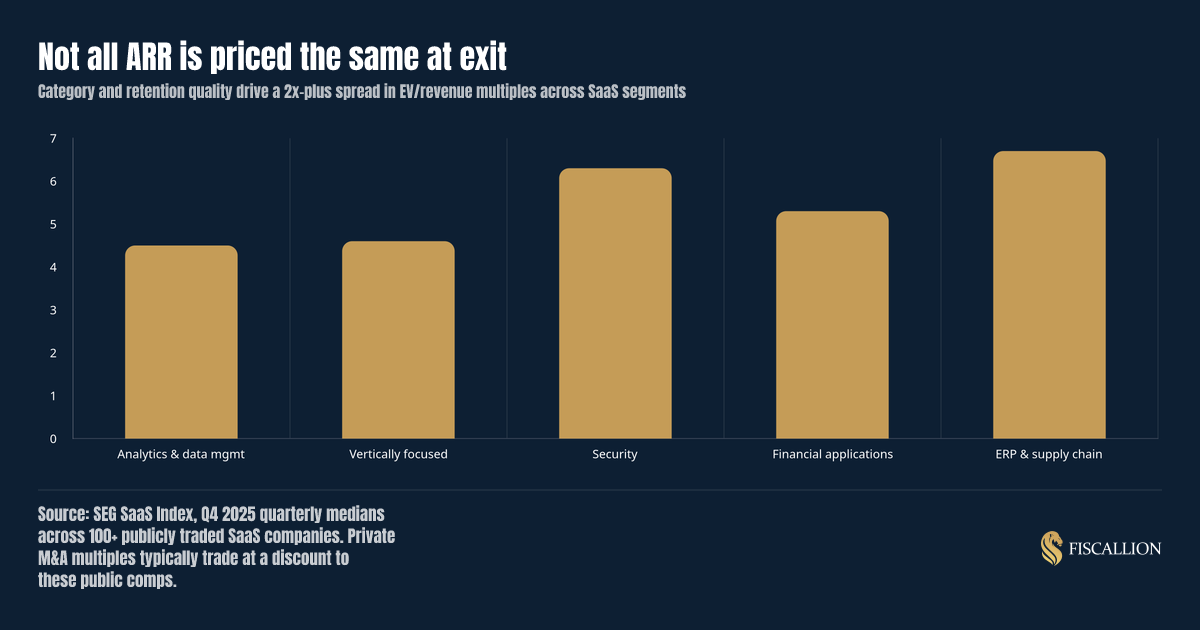

- Exit valuation is driven far more by net revenue retention, gross margin, and growth efficiency than by ARR size alone. SaaS categories with strong retention trade at more than a 2x spread in multiple versus weaker categories.

- Exit readiness is a finance infrastructure problem before it is a banker problem. Clean cohort-level unit economics, accrual-based statements, and a defensible forecast model matter more than a polished pitch deck.

- Most founders wait too long to build exit-ready reporting. The right time to start is 18-24 months before you want optionality, not the quarter you decide to explore a sale.

What we'll cover

- What a startup exit strategy actually means for a scaling SaaS company

- The four common exit strategies and how they differ financially

- How to calculate your exit readiness and rough valuation range

- How to interpret your position and pick the right path

- What to do next to build optionality

- Common mistakes founders make and the better move

- A practical exit-readiness checklist you can run this quarter

- Frequently asked questions

What a startup exit strategy actually is

A startup exit strategy is the plan for how founders, employees, and investors convert their equity into cash or liquid stock. It answers three questions: who buys, when, and at what price.

For a SaaS company between $5M and $50M ARR, the exit strategy question usually surfaces at one of four trigger points: a board member starts asking about timeline, a competitor gets acquired and resets market expectations, growth slows and the next round gets harder to raise, or the founder decides they are done building.

Here is the part most founders get backward: an exit strategy is not a document you write when a buyer shows interest. It is the byproduct of years of financial discipline. Acquirers and bankers do not pay a premium for a good story. They pay a premium for verifiable, cohort-level evidence that your unit economics hold up and your forecast is credible. That evidence either exists in your finance function already, or it does not, and you cannot manufacture it in a 90-day sprint before diligence.

This is the same discipline Fiscallion applies across FP&A for startups: decisions get made on cash, runway, and trade-offs, not on activity metrics dressed up for a board deck. An exit is the highest-stakes version of that same discipline, applied under a deadline.

The four common exit strategies for SaaS companies

There are four paths that account for nearly every SaaS exit. Each has a different buyer profile, valuation logic, and preparation timeline.

| Exit strategy | Who buys | Typical trigger | Valuation basis | Preparation runway |

|---|---|---|---|---|

| Acquisition (strategic M&A) | A larger company buying product, team, or market share | Competitive consolidation, product gap in acquirer's roadmap | Revenue multiple (ARR or EV/revenue), sometimes EBITDA multiple at scale | 12-24 months |

| IPO | Public market investors | Company reaches durable scale, usually $100M+ ARR | Public market comps, growth plus profitability (Rule of 40) | 24-36+ months |

| Acquihire | A company primarily buying the team, not the business | Product or growth stalls, but the team is strong | Per-employee price, minimal revenue credit | 3-9 months |

| Private equity buyout or secondary sale | A PE firm or growth investor buying control or a partial stake | Founder wants partial liquidity, or growth has plateaued into a profitable steady state | EBITDA multiple, heavy weight on margin and retention | 12-18 months |

For companies in the $5-50M ARR band this article is written for, strategic acquisition is the most common outcome by a wide margin. IPO is a real path only above roughly $100M ARR with a durable Rule of 40 score. Acquihire is a fallback outcome, not a strategy worth planning toward. Private equity buyouts have become more common as PE-backed platforms roll up profitable, retention-strong SaaS businesses, particularly in vertical software.

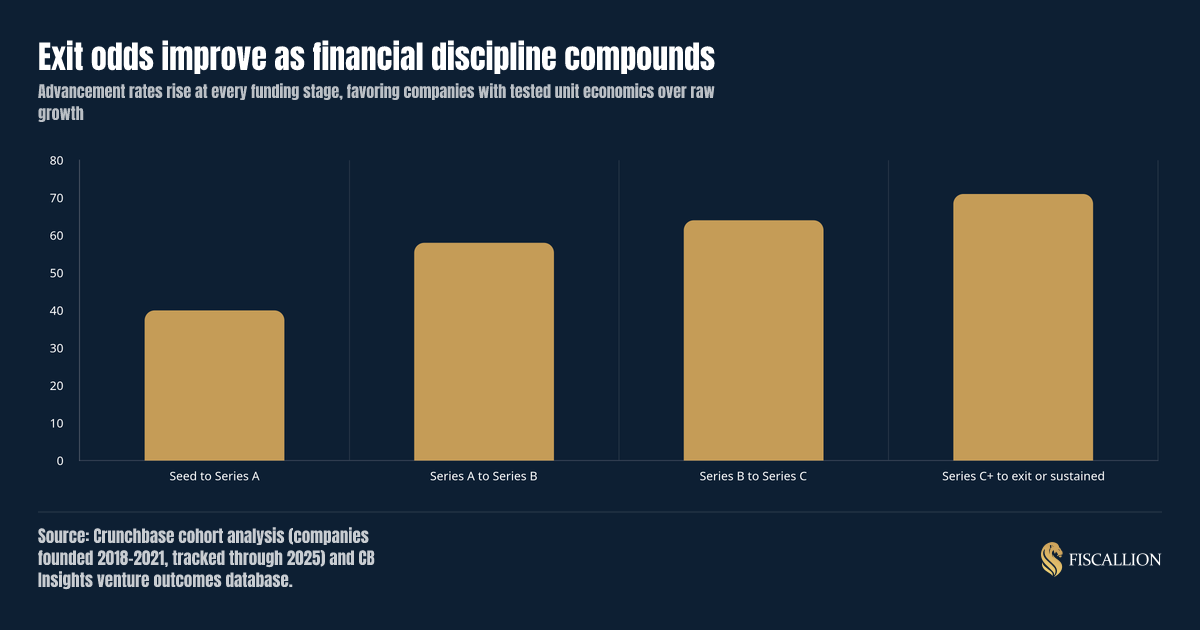

Financial discipline compounds across funding stages, and it shows up directly in how often companies survive to the next round instead of stalling out or shutting down.

Acquisition is the default path, and retention decides the price

This is the exit most venture-backed and bootstrapped SaaS companies reach. A larger company buys you to acquire your customer base, your product capability, or to remove a competitor from the market.

The valuation almost always comes down to a revenue multiple, adjusted heavily for net revenue retention, gross margin, and customer concentration. Two companies at the same ARR can be priced two to three times apart depending on retention quality alone.

IPO applies to a narrow slice of companies, not most of them

An IPO is the highest-visibility exit and the one most founders reference by default, but it applies to a small fraction of companies in the $5-50M ARR range. The bar has risen since 2022: public investors now price growth against profitability using the Rule of 40, not growth alone.

If IPO is even a plausible long-term path for your company, your finance function needs to look like a public company's finance function years before the S-1, with clean accrual accounting, audited financials, and forecasting discipline that would survive an analyst's questions.

Acquihire is a signal to fix something, not a plan to build toward

An acquihire happens when a buyer wants your engineering or product team more than your business. Revenue and customers get little to no valuation credit. Founders often end up with retention packages tied to continued employment, not a clean cash exit.

This is rarely a strategy worth planning toward. It is what happens when a company runs out of better options. If acquihire language starts surfacing in your own exploratory conversations, treat that as a signal that your unit economics or growth trajectory need attention before you talk to anyone else.

Private equity buyouts reward margin discipline over growth rate

PE buyers and growth equity firms increasingly target profitable, retention-strong SaaS businesses that have plateaued into steady, defensible growth rather than hypergrowth. This path rewards margin discipline and predictable cash flow over top-line growth rate.

A secondary sale, where existing investors or the founder sell a partial stake without a full change of control, can also deliver partial liquidity without giving up the company. Raise this directly with your board if founder liquidity, not a full company sale, is the actual goal.

How to calculate your exit readiness and rough valuation range

Exit valuation is not one number. Treat it as a range built from three inputs: your revenue quality, your margin profile, and your growth efficiency.

Step 1: Establish your clean ARR base.

Strip out one-time revenue, services revenue that will not transfer to a buyer, and any customer concentration above 15% in a single account. Buyers discount for concentration risk immediately, and they will find it in diligence even if it is not in your headline metrics.

Step 2: Calculate net revenue retention and gross revenue retention by cohort.

NRR above 110% and GRR above 90% put you in premium-multiple territory. NRR below 100% signals a leaky bucket, and buyers will price that risk into the multiple rather than treat it as a caveat you can explain away.

Step 3: Apply a category-adjusted revenue multiple.

Public SaaS multiples compressed meaningfully from their 2021 peak, and private M&A multiples typically trade at a discount to public comps. The multiple you should model depends heavily on category and retention quality, not just company size.

Step 4: Layer in your growth and margin efficiency score.

The Rule of 40 (growth rate plus profit margin) is the shorthand buyers use to judge whether your growth is efficient or subsidized by cash burn. A company growing 25% with break-even margins scores the same as one growing 40% while burning 15 points of margin. Buyers are increasingly indifferent between those two paths as long as the Rule of 40 clears roughly 30-40, but they will discount a company that clears neither growth nor profitability thresholds.

Step 5: Stress-test the number against your cash runway.

A high theoretical valuation means little if your runway forces you to sell under time pressure. Model your runway under a no-new-financing scenario and compare it to your expected deal timeline. If your runway is shorter than your realistic time to close, you are negotiating from weakness before the first call happens.

How to interpret where you actually stand

Run your numbers through this lens before you talk to anyone about a sale.

| Signal | What it means | Read this way |

|---|---|---|

| NRR above 110%, GRR above 90% | Retention-driven growth, low churn risk | You can be patient. Multiple expansion favors waiting for the right buyer. |

| NRR 95-105%, flat growth | Stable but not compounding | Acquisition at a mid-range multiple is realistic. IPO is unlikely without a growth reacceleration story. |

| NRR below 95%, high CAC payback | Structural retention problem | Fix retention before entering any process. A weak NRR story surfaces in diligence and kills deals late, after you have spent months on process. |

| Runway under 12 months, no clear path to profitability | Negotiating leverage is gone | You are a distressed seller, not a strategic one. Buyers know it and price accordingly. |

| Runway 18+ months, Rule of 40 above 30 | Optionality intact | You control timing. This is the position to be in before you start any conversation. |

The pattern across all five rows is the same: optionality is the actual asset you are protecting. A founder with 18 months of runway and clean retention data can walk away from a lowball offer. A founder with 8 months of runway cannot, regardless of how good the underlying business is.

This same optionality logic explains why the "90% of startups fail" statistic gets misapplied so often. It describes a full lifecycle across a broad population, not the odds facing a disciplined, revenue-generating SaaS company today.

Most of that attrition happens in years two through five, concentrated among pre-revenue and pre-product-market-fit companies. A company at $5-50M ARR with a working sales motion and retained customers has already cleared the stage where most of that failure curve occurs.

What to do next to build exit optionality

Start 18-24 months before you want the option to sell, not the quarter a term sheet shows up.

- Move to cohort-level reporting now. Board decks that show blended ARR and blended churn hide the retention story buyers actually price. Break customers into cohorts by signup quarter and segment, and track NRR and GRR at that level.

- Close the gap between cash and accrual accounting. Buyers and their diligence teams work in accrual terms. If your books are still cash-basis, the transition takes months, not weeks, and it should not happen for the first time during an active process.

- Build a 3-scenario runway model, not a single-line forecast. Model base, downside, and no-new-financing cases side by side. This is the same discipline behind a defensible board deck: it frames the trade-offs instead of just reporting last quarter's actuals.

- Fix customer concentration before it shows up in a data room. If any single account is above 10-15% of ARR, start diversifying now. This is a multi-quarter fix, not something you can explain away in a diligence call.

- Get one clean valuation opinion 12+ months before you plan to sell. Not to negotiate against, but to understand which of the three or four levers above moves your multiple the most for your specific business.

If your board or leadership team is debating whether to bring on a full-time CFO to run this process, consider the actual gap first. Most $5-50M ARR companies do not have a CFO problem; they have a decision-quality and FP&A problem. A full-time CFO hire adds cost and reporting polish, but it does not automatically fix a forecasting model that has never been stress-tested or a unit economics story that has never been broken into cohorts. That is the specific gap Fiscallion Finance closes: CFO-level judgment on exit readiness, cash, and trade-offs, without the fixed cost of a full finance org before you need one.

Common mistakes and the better move

Mistake: Treating CAC/LTV as a single clean number for the data room.

A single blended LTV:CAC ratio invites scrutiny, because buyers know it hides variance across segments. The better move: present LTV:CAC as a range by cohort and acquisition channel, with the assumptions stated explicitly. A range you can defend beats a point estimate that collapses under one follow-up question.

Mistake: Waiting for a term sheet before cleaning up the numbers.

By the time a buyer is in diligence, you have no time left to fix retention, reduce concentration, or rebuild a credible forecast. The better move: run the exit-readiness checklist below annually, whether or not you plan to sell that year. Optionality compounds the same way retention does.

Mistake: Letting the board deck report history instead of framing the decision.

A deck that shows last quarter's metrics without a recommendation forces the board to guess what management thinks the next move should be. The better move: every board update should state the trade-off explicitly, for example slower growth with 18 months of runway versus faster growth with 10 months, and recommend one.

Mistake: Modeling one valuation number instead of a range tied to levers.

A single number invites founders to anchor on best-case assumptions and get disappointed later. The better move: model three scenarios (base, upside from fixing retention, downside from a slower market) so the range itself becomes a planning tool, not just a wish.

Mistake: Hiring a full-time CFO purely to look exit-ready.

Adding headcount and polish does not fix a forecasting model that has never been pressure-tested against a real scenario. The better move: get the FP&A discipline right first, whether through a fractional CFO, an outsourced finance partner, or an internal analyst working from a decision-grade framework. Add permanent headcount once the complexity justifies the fixed cost.

A practical exit-readiness checklist

Run this checklist this quarter, independent of whether you plan to sell this year.

- Cohort-level NRR and GRR calculated and tracked monthly, not just at board meetings

- Customer concentration below 15% in any single account, with a plan if you are not there yet

- Accrual-based financial statements, reconciled monthly

- A 3-scenario cash runway model (base, downside, no-new-financing)

- Rule of 40 score calculated and tracked quarterly

- A category-adjusted valuation range refreshed at least annually

- Board materials that state a trade-off and a recommendation, not just historical metrics

- A documented answer to "what happens if we do not raise or sell in the next 18 months"

If more than two of these are unchecked, your exit timeline is being decided for you by circumstances rather than by you. That is the gap to close first, before any conversation with a banker or acquirer.

Frequently asked questions

What is a common exit strategy for startups?

The most common exit strategy for a venture-backed or bootstrapped SaaS company is a strategic acquisition, where a larger company buys the business for its product, customer base, or team. This applies far more often than IPO, which is realistic only for a small number of companies that reach durable scale, typically above $100M ARR with strong growth and profitability. For companies in the $5-50M ARR range, acquisition is the default path to plan around, and the valuation depends heavily on net revenue retention and margin quality rather than ARR size alone.

Is it true that 90% of startups fail?

The 90% figure is directionally accurate but frequently misapplied. It comes from research tracking venture-scale, innovation-stage startups across their full lifecycle, not all small businesses and not specifically profitable SaaS companies with real customers and revenue. US Bureau of Labor Statistics data shows a very different picture for all businesses: roughly 20% fail in year one and about 49% by year five. The 90% figure applies to a narrower, higher-risk population chasing venture-scale outcomes. A SaaS company at $5-50M ARR with positive unit economics and disciplined cash management is in a fundamentally different risk category than the population that 90% statistic describes, and treating it as your personal odds of failure is a category error.

What is the 5 year exit strategy?

A 5-year exit strategy is a plan that targets a sale, IPO, or other liquidity event within roughly five years of founding or of a specific funding round, and it is common in venture-backed companies where investors expect a return within a fund's typical 7-10 year lifecycle. In practice, this means working backward from year five: by year three or four, the company needs cohort-level retention data, a credible growth and margin trajectory, and clean financials that could support diligence. The discipline is the same regardless of the exact year: build the finance infrastructure early enough that an exit becomes a choice you make on your terms, not a scramble triggered by a term sheet or a runway crisis.

What are the four exit strategies?

The four common startup exit strategies are: acquisition (strategic M&A), where a larger company buys the business for its product or customer base; IPO, where the company lists on a public market, typically only realistic at significant scale; acquihire, where a buyer is primarily interested in the team rather than the business itself, with minimal revenue credit; and private equity buyout or secondary sale, where a PE firm or growth investor buys control or a partial stake, usually rewarding profitability and retention over raw growth rate. Most $5-50M ARR SaaS companies should plan primarily around acquisition, treat IPO as a longer-term possibility only if metrics support it, avoid steering toward acquihire, and consider a PE or secondary path if founder liquidity without a full sale is the actual goal.

Conclusion

An exit strategy is not something you negotiate in the final quarter before a sale. It is the compounding result of cohort-level retention discipline, a defensible cash and runway model, and board reporting that frames trade-offs instead of reciting history.

The founders who control their exit timeline are the ones who treated FP&A as decision infrastructure years before a banker ever asked for a data room. The founders who get forced into a rushed sale are the ones who waited for the deadline to build the discipline.

If you are within 12-24 months of wanting real exit optionality and are not confident your cohort economics, runway model, and board reporting would survive a buyer's scrutiny today, audit your metrics definitions and forecasting model before you start any conversation with an acquirer or banker.