Qualified small business stock, or QSBS, can turn a portion of your exit into money the federal government never taxes. For a founder or early employee at a C corporation, that is not a footnote. It is one of the largest single line items in your personal balance sheet planning, and it depends entirely on decisions you make years before any acquisition or IPO conversation starts.

Most founders treat QSBS as a legal detail their lawyer handles at incorporation and then forget about. That is the mistake. QSBS status has to survive years of fundraising, entity changes, and gross asset growth, and it can be silently forfeited by decisions that have nothing to do with taxes on the surface, like raising a bridge round at the wrong valuation or converting from an LLC too late. This piece gives you the decision-grade version: what QSBS is, how to calculate your exclusion, how to interpret your eligibility as your company scales past $5M and toward $50M ARR, and what to check before your next round or exit.

Key takeaways

- QSBS (Section 1202 stock) lets non-corporate shareholders exclude federal capital gains tax on qualifying C corporation stock, up to the greater of a flat dollar cap or 10 times your basis.

- The One Big Beautiful Bill Act (OBBBA), signed July 4, 2025, raised the per-issuer exclusion cap from $10 million to $15 million and the corporate gross asset ceiling from $50 million to $75 million for stock issued after that date.

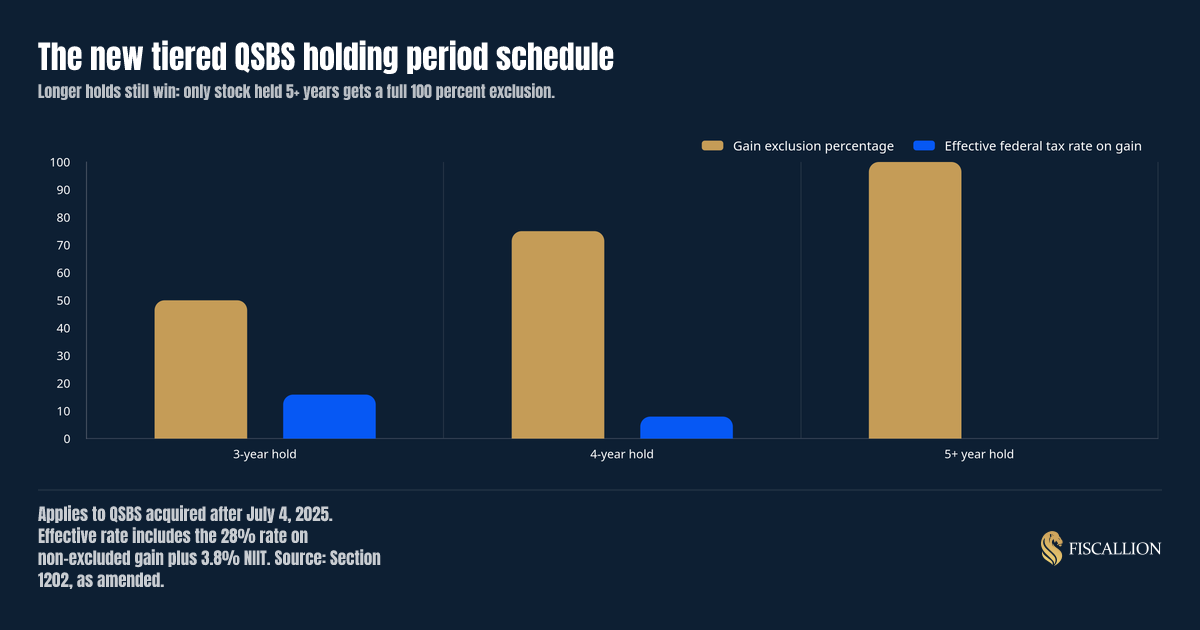

- OBBBA also introduced a tiered holding period: 50% exclusion at 3 years, 75% at 4 years, and 100% at 5 years or more, replacing the old all-or-nothing 5-year cliff for newly issued stock.

- Eligibility is tested at issuance and must hold for substantially all of your holding period. A late-stage bridge round, an entity conversion, or crossing the gross asset threshold can disqualify shares issued afterward.

- QSBS is a founder and early-employee planning question, not just a legal formation checkbox. It belongs in the same forecasting conversation as your cap table, your 409A, and your runway model.

What we'll cover

This article walks through the mechanics of QSBS in order: what qualifies, how the exclusion is calculated under the new OBBBA rules, how to interpret your eligibility at different stages of growth, what actions to take now, the mistakes that quietly kill QSBS eligibility, and a practical checklist you can run before your next financing round.

What QSBS actually is and why it matters for a scaling SaaS company

QSBS is short for qualified small business stock, defined under Section 1202 of the Internal Revenue Code. If you or your early employees hold stock that meets the requirements, you can exclude some or all of the capital gain from federal tax when you sell.

For a SaaS company, this usually applies to:

- Founders' common stock issued at incorporation or an early priming round.

- Stock issued to employees exercising incentive stock options, if the underlying shares qualify.

- Preferred stock issued to early investors, including seed and Series A investors, if the issuing entity is a qualifying C corporation.

The exclusion is not a loophole. It is a deliberate policy incentive, in place since 1993, meant to reward long-term ownership in small, active operating companies rather than short-term trading or passive investment vehicles. That is also why the rules exclude certain business types outright: professional services (law, accounting, consulting, financial services), banking, insurance, farming, hotels, and a handful of other categories. Most SaaS and software businesses fall outside those exclusions and qualify, provided the corporate-level tests are met.

Here is the requirement checklist at the entity level:

| Requirement | Standard |

|---|---|

| Entity type | Domestic C corporation (not an LLC, S corp, or foreign entity) |

| Gross assets | Aggregate gross assets under $50M (pre-OBBBA) or under $75M (post-OBBBA), at all times before and immediately after the stock issuance |

| Business activity | Active conduct of a qualified trade or business, using at least 80% of assets in that business |

| Excluded industries | No health, law, accounting, consulting, financial services, banking, farming, mineral extraction, or hospitality businesses |

| Stock origin | Acquired at original issuance directly from the corporation, in exchange for cash, property, or services (not purchased on a secondary market) |

And at the shareholder level:

| Requirement | Standard |

|---|---|

| Taxpayer type | Non-corporate: individuals, trusts, and pass-through entities like LLCs taxed as partnerships |

| Holding period | At least 3 years for stock issued after July 4, 2025 (tiered exclusion); more than 5 years for stock issued on or before that date |

| Continuity | Stock must qualify as QSBS for substantially all of the holding period |

If your company has raised past $50M in aggregate gross assets and issued its stock before July 5, 2025, that stock likely lost QSBS eligibility going forward at the moment your balance sheet crossed the threshold. Stock already issued while you were under the cap generally keeps its status; new stock issued after crossing the old $50M line typically does not qualify, unless it now falls under the new $75M ceiling introduced by OBBBA for post-July 4, 2025 issuances.

How to calculate your QSBS exclusion

The exclusion has two layers: how much of the gain you can exclude (the percentage), and how much gain qualifies for exclusion at all (the dollar cap).

Step 1: Determine your applicable exclusion percentage.

This depends on when the stock was issued and how long you held it.

| Stock issuance date | Holding period required | Exclusion percentage |

|---|---|---|

| On or before July 4, 2025 | More than 5 years | 100% |

| After July 4, 2025 | At least 3 years, less than 4 | 50% |

| After July 4, 2025 | At least 4 years, less than 5 | 75% |

| After July 4, 2025 | 5 years or more | 100% |

Step 2: Determine your dollar cap.

The exclusion is capped, per taxpayer per issuer, at the greater of:

- A flat dollar limit: $10 million for stock acquired on or before July 4, 2025, or $15 million for stock acquired after that date (indexed for inflation starting in 2027), or

- 10 times your adjusted basis in the QSBS you are selling that year.

The 10x basis rule matters more than founders expect. If you paid very little for founders' stock at incorporation (a common and correct move), your basis might be $10,000. Ten times that is only $100,000, far below the flat cap. In that scenario, the flat dollar limit, not the basis multiple, is what protects your exclusion. Investors who paid a meaningful price per share for preferred stock may find the 10x basis calculation exceeds the flat cap, especially on large checks into high-growth rounds.

Step 3: Calculate the tax on the non-excluded portion.

Gain that is not excluded is taxed at 28% (not the standard 20% long-term capital gains rate) plus the 3.8% net investment income tax. That produces these effective rates:

| Holding period (post-OBBBA stock) | Exclusion | Effective federal rate on the gain |

|---|---|---|

| 3 years | 50% | 15.9% |

| 4 years | 75% | 7.95% |

| 5+ years | 100% | 0% |

Worked example. A founder holds QSBS issued in August 2025, purchased for $50,000 at incorporation. The company sells in an acquisition six years later for a gain of $18 million.

- Holding period exceeds 5 years, so the exclusion percentage is 100%.

- The dollar cap is the greater of $15 million or 10x basis ($500,000). The flat cap of $15 million applies.

- $15 million of the $18 million gain is excluded from federal tax entirely.

- The remaining $3 million is taxed at standard long-term capital gains rates (not the 28% rate, since that higher rate applies specifically to the non-excluded portion of gain under the tiered 3-4 year exclusions, not to gain above the cap under the 100% tier). Consult your tax advisor on the exact characterization of the excess.

This is the kind of number that changes how a founder thinks about exit timing, secondary sales, and even whether to split shares across a spouse or trust to access multiple per-issuer caps.

How to interpret QSBS eligibility as you scale past $5M ARR

QSBS is not a one-time qualification. It is a status that has to survive your company's growth trajectory, and that trajectory is exactly what puts most $5-50M ARR SaaS companies at risk.

If you are under $50M in gross assets right now: any stock issued today likely qualifies, assuming your entity and business activity tests are met. This is the highest-leverage window to issue equity, whether through new hires, option grants, or additional founder stock, because every share issued now can lock in QSBS treatment before your balance sheet grows further.

If you are between $50M and $75M in gross assets: stock issued after July 4, 2025 can still qualify under the new $75M ceiling, even though it would have failed the old $50M test. This is a direct, practical benefit of OBBBA: it widened the window for growth-stage companies raising larger rounds to keep issuing QSBS-eligible stock.

If you are approaching or past $75M in gross assets: new stock issuances stop qualifying going forward. This does not retroactively disqualify shares issued while you were under the cap, but it means every new hire, every new option grant, and every new investor check from this point forward misses the exclusion. This is a forcing function, not a footnote: it changes the math on whether to raise a large round now versus staging capital, and it changes how you think about equity compensation design for new hires.

A note on gross assets versus valuation. Founders frequently confuse the QSBS gross asset test with company valuation. They are different. Gross assets means cash plus the adjusted basis of the corporation's property, not your Series B valuation or your enterprise value multiple. A company can be valued at $300 million with a small cash balance and modest fixed assets and still sit under the $75 million gross asset ceiling. This is why the test needs to be run on your balance sheet, not your cap table.

Rollover relief under Section 1045. If you need liquidity before your holding period matures, Section 1045 allows a tax-free rollover of QSBS gain into new QSBS, provided you reinvest within 60 days of the sale and have held the original stock for at least six months. This is useful for early secondary sales or partial liquidity events during a later financing round, without forfeiting the exclusion outright.

What to do next: a decision checklist for founders and finance leads

QSBS planning is not something to defer until a term sheet lands. By then, most of your leverage is gone. Here is what to check now, especially if you are heading into your next board meeting, financing round, or acquisition conversation.

- Confirm your entity type today. If you are still an LLC or converted late from one, QSBS eligibility on early equity may already be compromised. Get a written confirmation from counsel on your C corp conversion date and its effect on the holding period clock.

- Run the gross asset test on your actual balance sheet, not your valuation. Ask your finance lead or outside accountant to calculate aggregate gross assets before your next primary round closes, not after.

- Time large capital raises with QSBS windows in mind. If a large round would push you over the $75M gross asset ceiling, consider whether staging the raise, or issuing additional stock just before close, preserves eligibility for a larger set of shareholders.

- Document issuance dates precisely. The holding period clock starts at issuance, and tacking rules under the OBBBA prevent converting older, pre-enactment stock into the new, shorter 3-year tiers through exchanges. Keep a clean record for every option exercise and stock grant.

- Model the exclusion into your personal and company-level exit planning, not just your legal docs. Your board deck and your personal wealth planning are usually run by different people who never compare notes. That gap is where QSBS value gets lost. At Fiscallion, we treat QSBS status as part of the same decision-grade FP&A model we build for runway and headcount, because an exit-stage tax outcome is still a forecasting input, not an afterthought.

- Revisit eligibility with every new priced round. A down round, a bridge, or a SAFE conversion can each affect the gross asset calculation and the entity structure. Do not assume day-one eligibility holds automatically through Series C.

Common mistakes and the better move

Mistake: treating QSBS as a law firm checkbox handled once at incorporation.

QSBS eligibility is a continuous test, not a one-time filing. The better move: review QSBS status at every financing event, the same way you review your cap table and 409A valuation, because gross assets and entity structure both shift with every round.

Mistake: confusing company valuation with the gross asset test.

Founders assume a $200 million valuation automatically disqualifies the company. It does not. The better move: calculate aggregate gross assets, cash plus adjusted basis of property, directly from the balance sheet before assuming disqualification.

Mistake: waiting until the acquisition LOI to ask whether stock qualifies.

By the time a deal is on the table, the holding period and issuance date are already fixed. There is no fixing a five-year clock with three months left before close. The better move: build QSBS review into fundraising prep and annual equity planning, not deal diligence.

Mistake: assuming all preferred stock qualifies the same way as founders' common stock.

Investors who bought in at a high price per share can have different exclusion math than a founder with near-zero basis, because the 10x basis alternative behaves differently at different valuations. The better move: calculate the exclusion cap separately for each shareholder class using both the flat limit and the 10x basis test.

Mistake: treating a late C corp conversion as a minor legal cleanup step.

If your company started as an LLC and converted to a C corp mid-life, the QSBS holding period generally starts at the conversion, not at the company's founding. The better move: confirm your conversion date and communicate it clearly to every equity holder, since it directly changes when their 3, 4, or 5-year clock actually starts.

Mistake: assuming your CFO-level tax planning happens automatically inside your accounting stack.

QSBS decisions sit at the intersection of legal structuring, cap table management, and forecasting, three functions that rarely talk to each other at a $5-50M ARR company without a full finance org. The better move: bring QSBS review into the same cadence as board reporting and forecasting, where trade-offs across capital raised, dilution, and tax exposure get modeled together instead of debated separately after the fact.

A practical asset: your QSBS eligibility snapshot

Before your next board meeting or financing round, run this five-line snapshot with your finance lead or outside counsel:

| Check | Your answer |

|---|---|

| Current aggregate gross assets (cash + adjusted basis of property) | $____ |

| Entity type and C corp conversion date (if applicable) | ____ |

| Earliest QSBS issuance date and current holding period | ____ years |

| Applicable exclusion percentage at today's date | ____% |

| Dollar cap available: greater of flat limit or 10x basis | $____ |

Keep this snapshot updated every time you close a round. It takes fifteen minutes with the right numbers on hand and prevents the far more expensive conversation that happens when a buyer's counsel discovers a gap during acquisition diligence.

Conclusion

QSBS is one of the few places in the tax code where a structural decision made years in advance, not a clever transaction at exit, determines whether a founder keeps millions more of their own gain. The OBBBA changes made in 2025 widened the opportunity: a higher $15 million cap, a larger $75 million gross asset ceiling, and a tiered holding period that rewards patience without demanding a rigid five-year all-or-nothing bet.

None of that changes the underlying discipline required. QSBS eligibility has to be tracked continuously, tested against your actual balance sheet rather than your valuation, and built into the same forecasting conversation you already run for runway, headcount, and capital allocation. Treating it as a one-time legal formality is the single most common way founders lose access to an exclusion worth millions.

If your cap table, entity history, and gross asset position have never been reviewed together against Section 1202, that gap is worth closing before your next round closes it for you. Audit your metrics definitions and forecasting model with Fiscallion, and make QSBS part of the decision-grade FP&A discipline you already run for cash, runway, and growth trade-offs.