When a fundraise gets messy or the board starts pressing for better numbers, most SaaS founders rush to hire a full-time CFO. That is usually a mistake. You don’t have a headcount problem; you have a decision-quality problem. Shoving a traditional corporate finance leader into a growth-stage subscription business will give you cleaner slides, but it won't fix your underlying data strategy.

Understanding what a SaaS CFO actually does - and how those responsibilities differ from a traditional finance leader - is the starting point for making the right call.

Key takeaways

- A SaaS CFO's core work is not bookkeeping or compliance. It is translating MRR movements, CAC payback, and runway math into decisions the leadership team can act on.

- The four-face model (steward, operator, strategist, catalyst) describes what CFOs do in theory. In practice, early-stage SaaS companies need the strategist and catalyst faces long before they need the steward.

- Full-time CFO compensation at the Series A-B stage runs $180K-$320K in base salary plus equity. A fractional model delivers the same strategic output for $5K-$15K per month - without the full-time cost.

- Most companies between $5M and $30M ARR need CFO-level thinking, not a full-time CFO headcount. The gap between those two things is where decision quality breaks down.

What a SaaS CFO actually does (versus what the title implies)

A CFO title at a $300M public company and a CFO title at a $15M ARR SaaS company describe fundamentally different jobs. The compliance work, SEC reporting, and treasury complexity of an enterprise finance function don't exist at Series B. What does exist - and what most scaling SaaS companies get wrong - is the absence of a single owner for forward-looking financial decisions.

A SaaS CFO's job is to keep the business from making decisions blind. That means owning the financial model, connecting operational metrics to cash flow, and making trade-offs legible to the CEO and board. It is not primarily about the close, the audit, or producing a deck.

Subscription architecture fundamentally changes the finance function, requiring metrics a traditional corporate CFO rarely handles:

- Revenue recognition under ASC 606, including deferred revenue treatment for annual and multi-year contracts

- MRR bridge construction (new, expansion, contraction, churn) as a live management tool - not a monthly report

- CAC payback period as a capital allocation input, not just a benchmark number

- Net Revenue Retention (NRR) as the primary leading indicator of revenue quality

- Runway modeling with scenario branches tied to hiring plan, churn assumptions, and pipeline conversion

None of these are accounting functions. They are decision-support functions. That distinction matters when you are deciding whether to hire, when to hire, and what level of finance leadership your stage actually requires.

The top 5 responsibilities of a SaaS CFO

1. Financial planning and runway management

The CFO owns the financial model - not as a static spreadsheet updated once a quarter, but as a live instrument that reflects current assumptions about growth, burn, headcount, and capital. A well-structured SaaS financial model tracks the actual timing of cash in and out, and surfaces at least three scenario branches: base, upside, and downside.

Runway management means maintaining at least 12-18 months of cash visibility at any point. It also means running scenario branches: what happens to runway if Q3 pipeline converts at 60% instead of 80%? What does hiring two AEs in Q2 do to CAC payback? The CFO answers those questions before the leadership team needs to ask them. Harvard Business Review's analysis of CFO scenario planning makes a direct case that scenario planning is no longer a periodic exercise - it is an ongoing operating discipline for finance leaders.

2. SaaS metrics ownership and unit economics

A SaaS CFO defines, calculates, and defends the metrics the company runs on. That includes:

- MRR and ARR with consistent recognition logic across billing, CRM, and accounting

- CAC split by channel and cohort - not a blended average

- LTV modeled as a range with churn assumptions stated explicitly

- CAC payback period as a capital efficiency signal (12 months = healthy; 18-24 months = manageable; 30+ months = a cash problem)

- NRR / NDR as the single best indicator of product-market fit in the existing base

The mistake most companies make is treating these as reporting metrics. A SaaS CFO treats them as decision inputs. When CAC payback is rising, you examine channel mix and sales cycle length - you don't just note the trend and move on. OpenView Partners' research on common CAC payback period mistakes documents the most frequent calculation errors that cause companies to misread their own capital efficiency.

3. Board and investor reporting

A critical piece of forward-looking board management is knowing how to steer conversations away from highly speculative, ungrounded financial exercises that are often weaponized to suppress valuations. True alignment happens when you focus on actual market comparables.

The CFO's job is to translate the numbers into trade-offs: "We can hit the ARR target while maintaining 14 months of runway, or we can invest in an enterprise sales motion now and land at 9 months. Here are the assumptions behind each path."

The fundamental test of executive financial reporting is whether it simply records the past or actively shapes upcoming strategic choices. If a presentation requires nothing more than a passive nod from directors, it fails to utilize their time effectively

Boards at Series A-C ask two questions: Is the business performing against plan? What should we decide next? The CFO answers both.

4. Fundraising strategy and capital allocation

Raising capital is a finance-led process. The CFO builds the financial model for the data room, owns the assumptions in the investor narrative, and manages the diligence process. Getting a fractional CFO engaged at least 90 days before a fundraise is not a luxury - it is table stakes for a clean, credible process.

Capital allocation decisions - whether to invest in PLG infrastructure, hire a field sales team, or extend runway - require explicit trade-off models. The CFO builds those models and presents them with assumptions named, not buried.

5. Compliance, controls, and audit readiness

This is the steward function: making sure the books are closed accurately, revenue is recognized correctly, and the company can survive an audit or acquisition diligence without surprises.

Revenue recognition under ASC 606 is particularly complex for SaaS businesses with multi-year contracts, usage-based billing, or bundled service elements - all of which require careful treatment of performance obligations and deferred revenue schedules.

At earlier stages, this often means managing the relationship with an external accounting firm and maintaining clean chart of accounts hygiene. At later stages - Series C and beyond - it means building internal controls that satisfy investors and preparing for a potential audit or SOX-adjacent compliance framework.

This responsibility matters, but it is the floor of a CFO's job, not the ceiling. Treating compliance as the primary CFO output is one of the most common hiring mistakes at $10M-$25M ARR.

Many growth-stage businesses jump straight into a heavy, expensive executive hire before their internal reporting foundation is actually mature enough to support it. The reality of what is truly missing at this stage comes down to infrastructure.

The four faces of a SaaS CFO

Deloitte's four-faces framework is the most widely cited model for understanding CFO role scope. It describes four distinct modes a CFO operates in, each with a different audience and output. Here is how each face applies specifically to a scaling SaaS company.

Most early-stage SaaS companies hire for the steward first - they want clean books and compliance. The actual leverage is in the strategist and catalyst faces, which require someone who understands SaaS business models well enough to translate activity into capital decisions.

What a fractional CFO does for a SaaS company

A fractional CFO provides CFO-level strategic finance on a part-time basis - typically 10 to 40 hours per month depending on scope. The engagement covers everything a full-time CFO would own strategically, without the full-time cost.

For a SaaS company at $5M-$30M ARR, a fractional CFO typically covers:

- Financial model ownership - building and maintaining the three-statement model with scenario branches

- MRR bridge and cohort analysis - tracking revenue quality over time, not just totals

- Board deck preparation - translating metrics into the trade-off framing the board needs

- Fundraising support - financial model, data room, and diligence management

- Headcount and hiring model - connecting team growth to burn rate, runway, and unit economics

- Pricing and margin analysis - identifying where gross margin is being compressed and by what

The fractional model works because most SaaS companies at this stage don't need daily CFO involvement. They need rigorous thinking applied to the right decisions at the right cadence - monthly model updates, quarterly board materials, and pre-raise preparation when the time comes.

CFO salary benchmarks: full-time versus fractional

The compensation gap between full-time and fractional CFO models is significant - but so is the difference in what you get.

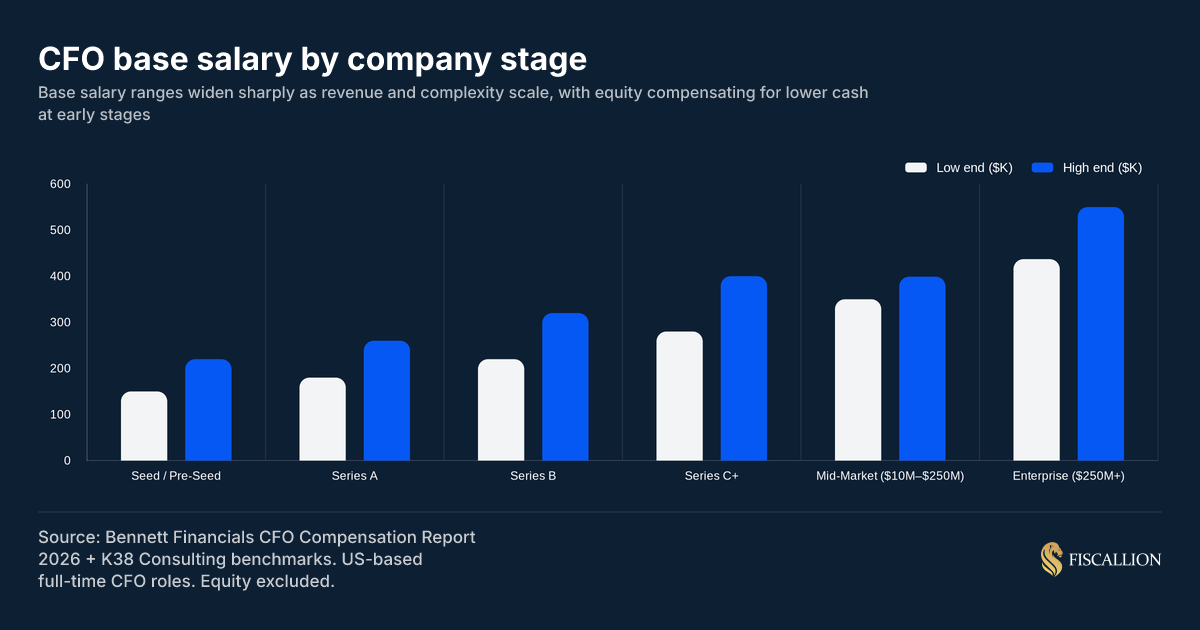

Full-time CFO base salary by stage

Base salary is only part of the picture. A full-time CFO package at Series A-B also includes:

- Annual bonus: 20-40% of base salary, tied to ARR growth, EBITDA, and cash flow targets

- Equity: 0.5-1.5% of fully diluted shares, vesting over four years with a one-year cliff

- Benefits, executive perks, and PTO: typically an additional $25K-$50K in annual value

A Series B SaaS company hiring a full-time CFO should budget $300K-$450K in total cash compensation plus meaningful equity dilution. That is the right investment if the business genuinely requires daily CFO-level leadership - complex multi-entity structure, active M&A, or pre-IPO preparation. Bennett Financials' CFO Compensation Report provides stage-by-stage benchmarks across startup, mid-market, and enterprise roles.

Fractional CFO cost comparison

The economics are clear: a $10K-$15K/month fractional engagement gives you 12-18 months of CFO-level output for the cost of roughly 2-3 months of a full-time hire's salary.

The trade-off is availability and depth of context. A fractional CFO is not on Slack daily. If your business has reached a stage where financial decisions are being made every day that require CFO judgment - active M&A, a complex capital structure, or a team of 10+ in the finance function - a full-time hire is the right move.

For most SaaS companies between $5M and $25M ARR, the fractional model covers the actual need.

When the CFO role becomes a hiring decision

Three conditions usually indicate you've outgrown the fractional model:

- Capital complexity - you are managing multiple debt facilities, investor SPVs, or a convertible note stack that requires daily attention

- Org scale - you have a finance team of 5+ people who need a dedicated internal leader

- Pre-IPO or M&A process - an active transaction requires full-time presence, SEC knowledge, and personal accountability to investors

Before those conditions exist, adding a full-time CFO adds cost and reporting polish without fixing the underlying decision-quality problem. The org gets better slides, not better decisions.

The more direct question: does your business have clean, assumption-owned financial models? Does your board get a trade-off framing instead of just a metrics update? Does every significant hiring or pricing decision run through a model before it's made?

If the answer to any of those is no, a fractional CFO engagement will resolve more of the problem than a full-time hire will.

Common mistakes and the better move

Mistake: Hiring a controller and calling them a CFO.

A controller owns the close, accounts payable, and audit readiness. That is the steward function. It does not include financial modeling, board framing, or capital allocation analysis. If you need forward-looking decision support, a controller title and scope won't get you there.

Better move: Separate the roles clearly. Let a strong controller own the close. Bring in a fractional CFO for the strategist and catalyst work. They are not the same job.

Mistake: Updating the financial model quarterly instead of monthly.

A model that's 90 days stale does not support the decisions being made this week. When runway assumptions are built on outdated churn or pipeline data, your board conversations are built on guesswork.

Better move: Establish a monthly model refresh cadence with named owners for each input: marketing owns CAC inputs, sales ops owns pipeline conversion, finance owns the close.

Mistake: Treating NRR as a reporting metric instead of a leading indicator.

Net Revenue Retention tells you the health of your existing customer base. If NRR is declining, it signals that expansion is slowing or churn is accelerating - often before it shows up in top-line ARR. Most SaaS companies report it; few use it to trigger a segmentation review or pricing adjustment. SaaS cohort analysis is the mechanism for diagnosing which segments or cohorts are driving the decline.

Better move: Set NRR thresholds that trigger specific reviews. If NRR drops below 100%, it triggers a cohort analysis by segment and contract type within 30 days - not a note in the next board deck.

Mistake: Presenting board materials as a history lesson.

A board deck that walks through trailing metrics - ARR up 12%, churn flat, headcount at 47 - answers "what happened?" but not "what should we decide?" The CFO's most important board contribution is the framing of what the data means for the next 90 days.

Better move: End every board financial section with a decision prompt. "Based on current burn and Q3 pipeline confidence, we recommend extending runway 90 days before committing to the enterprise sales hire. Here is what changes that recommendation."

A practical SaaS CFO responsibilities checklist

Use this checklist to audit whether your current finance function is covering the full CFO scope or leaving gaps.

Steward

- Financials close within 10 business days of month-end

- Revenue recognized correctly under ASC 606

- Deferred revenue schedule maintained and reconciled

- Audit-ready books: clean chart of accounts, minimal manual adjustments

Operator

- Monthly board/management reporting published on a fixed cadence

- Three-statement financial model updated monthly

- Cash flow forecast updated with actuals vs. plan variance noted

- AP/AR tracked with DSO monitored

Strategist

- 12-18 month runway modeled with at least two scenario branches

- CAC and LTV tracked by channel and cohort - not blended

- Headcount decisions run through a model before approval

- Capital allocation trade-offs documented before major investment decisions

Catalyst

- Finance metrics shared with department heads on a monthly cadence

- Sales, marketing, and CS leads know their unit economics

- Pricing decisions are informed by gross margin and CAC payback analysis

- Board materials frame choices, not just history

The bottom line: Buy the thinking, not the headcount

The CFO role in a SaaS company is not primarily about the close. It is about translating the business into decision-ready numbers - runway, unit economics, trade-offs, and capital allocation. That work requires someone who understands subscription revenue models, owns assumptions in the financial model, and prepares the board to make choices rather than just absorb history.

Most $5M-$30M ARR SaaS companies don't need a full-time CFO yet. They need CFO-level thinking applied at the right cadence. A fractional model covers that gap at a fraction of the cost, provided the engagement has clear scope and real ownership of the financial model.

If your board meetings consistently end with "great update" instead of a decision, the problem is not your metrics. It is the framing. That is a CFO responsibility - and fixing it does not require a $300K full-time hire to start.

Want to audit your current finance function against the full SaaS CFO scope? Book a working session with Fiscallion and we'll map where the gaps are and what it would take to close them.