Most founders treat the startup acquisition process as a legal event that starts when a term sheet lands. It is not. By the time an inbound offer or a banker's outreach reaches your inbox, the outcome is already half decided by whether your financials, unit economics, and forecasts can withstand scrutiny.

This article breaks down what a startup acquisition process actually involves, how buyers calculate what to offer, how to read the signals in an early conversation, and where deals lose value or die outright. The recurring theme: the founders who get the best price and the fastest close are the ones who treated their finance function as decision infrastructure long before a buyer showed up.

Key takeaways

- A startup acquisition process runs 6 to 12 months from serious preparation to close, but the deal is priced on data you should have been producing for the last 12 to 18 months, not the last 6 weeks.

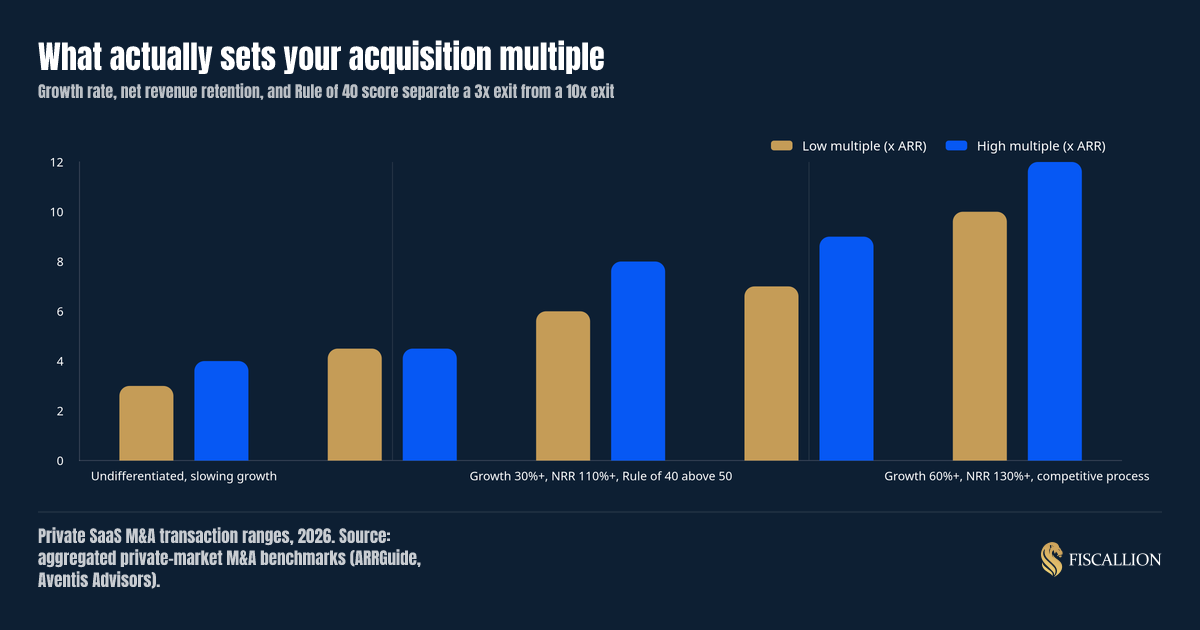

- Your ARR growth rate, net revenue retention (NRR), and Rule of 40 score do more to set your multiple than your product story. Private SaaS multiples in 2026 range from roughly 3x to 12x ARR depending on these three inputs.

- Diligence does not test your metrics. It tests whether your metrics definitions are consistent, documented, and reproducible across finance, sales, and the board deck.

- 30 to 40 percent of M&A deals fail or get re-traded during diligence, and the cause is almost always undisclosed or inconsistent financial and legal information, not a change of heart.

- The single highest-leverage move before engaging a buyer is a financial data room and forecasting model built to survive a quality of earnings (QoE) review, not a board meeting.

What we'll cover

- What the startup acquisition process actually is, and where it starts before you notice

- How long each phase takes and where deals stall

- How buyers calculate what to pay: the metrics that set your multiple

- How to interpret early signals so you know whether you have real leverage

- What to do in the 90 to 180 days before you engage a buyer

- The mistakes that cut price or kill deals, and the better move for each

- A practical acquisition-readiness checklist you can run against today

What the startup acquisition process actually is

A startup acquisition is a transaction where a buyer takes ownership of your company or its assets, structured as an asset sale, a stock sale, or a merger. The structure changes your tax exposure, what liabilities travel with the deal, and how much of the headline price you actually keep. Get counsel involved on structure early. It matters as much as price, sometimes more.

Deals begin one of two ways:

- Inbound interest. A corporate development contact or product leader starts a conversation framed as partnership or integration. It often is not. Acquirers frequently use "partnership" framing deliberately, because it lowers your guard while they gather intelligence on your metrics, roadmap, and customer base.

- A proactive, run process. You or a banker approach multiple buyers at once to create competitive tension. Data on dual-track processes (M&A run alongside a live funding round) consistently shows better pricing and terms than negotiating with a single counterparty, because no serious acquirer wants to lose a deal they have already invested time in.

Either path moves through the same core phases: preparation, outreach and NDAs, indication of interest, management presentations, a letter of intent (LOI), confirmatory due diligence, the definitive purchase agreement, and closing. What differs is how much of the preparation phase you have already done by the time real conversations start.

Why this matters for a $5-50M ARR company specifically

At this stage, you are past the point where a buyer will hand-wave your numbers. You are also usually not big enough to have a controller, a QoE-tested data room, or a CFO who has run a sale process before. That gap between "the size where diligence gets serious" and "the finance infrastructure to survive it" is exactly where deals lose value. It is the same gap Fiscallion exists to close on the forecasting and reporting side, independent of whether an acquisition is even on the table yet.

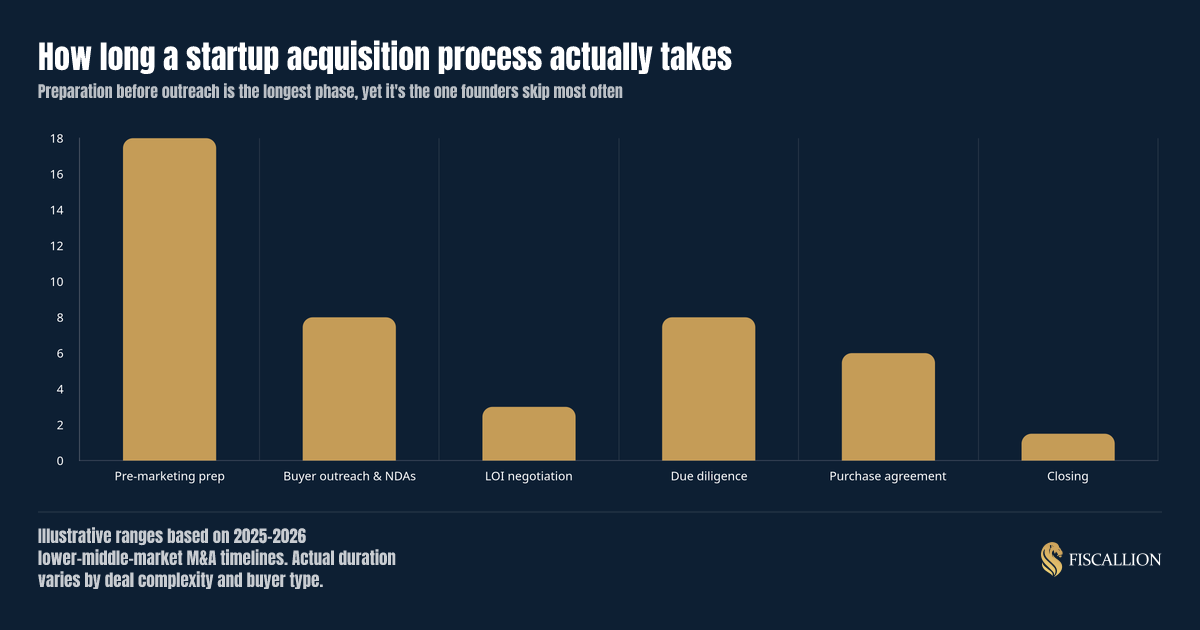

How long the process takes, and where it actually stalls

Founders ask this question expecting a simple number. The honest answer has two layers: the formal process from serious buyer engagement to wire transfer, and the preparation work that precedes it and determines how that formal process goes.

The formal process, once a buyer is seriously engaged, typically runs 6 to 9 months. But 18 to 24 months of preparation work, done quietly, in the background, while you keep running the company, usually separates a clean process from a messy one.

A few things worth naming from that timeline:

- Preparation is the longest phase and the one founders skip. Cleaning up the cap table, documenting IP assignment, standardizing revenue recognition, and building a defensible financial model takes months, not a sprint week before a data room opens.

- Your leverage peaks before exclusivity. Once you sign an LOI, most deals include an exclusivity window (commonly 60 to 90 days) during which you cannot shop the deal elsewhere. That is when your negotiating position weakens the fastest, so the terms you lock in the LOI matter more than founders expect.

- Diligence is where deals die or get re-traded. Roughly 30 to 40 percent of M&A deals fail or get renegotiated during diligence because of information that was undisclosed, inconsistent, or simply never assembled in the first place. According to the Axial Dead Deal Report, the leading causes of broken LOIs in 2025 were non-QoE diligence findings (25.3%) and quality of earnings discrepancies (21.3%) — together accounting for nearly half of all post-LOI failures. Deals with at least one re-trade event take roughly two months longer to close than clean deals.

How buyers calculate what to offer

This is the part most founders under-invest in understanding, and it is the part where Fiscallion's point of view differs from a generic M&A guide: valuation is not a single number you negotiate up. It is a formula buyers run, and three inputs dominate it. We cover those inputs in depth in our guide to SaaS valuation multiples, but the table below shows what matters most in an acquisition context.

| Metric | What it signals to a buyer | Why it moves the multiple |

|---|---|---|

| ARR growth rate | How fast the business compounds without the buyer's help | Below 15% growth, most buyers switch to EBITDA-based pricing entirely, treating you as a cash flow asset, not a growth asset |

| Net revenue retention (NRR) | Whether existing customers are a stable base or a leaking bucket | NRR below 95% and buyers start modeling revenue decline into the offer; above 120% and the multiple can roughly double |

| Rule of 40 score (growth rate + profit margin) | The trade-off between growth and capital efficiency | A 10-point improvement in Rule of 40 correlates with roughly a 1.1x increase in EV/Revenue multiple |

Here is how those inputs translate into actual private-market SaaS multiples in 2026:

The spread matters more than the median. Two companies at the same ARR can close 3x apart on multiple, and the difference is rarely the product. It is growth durability, retention quality, and whether the business generates cash or burns it while growing. McKinsey's research on the Rule of 40 confirms this: top-quartile SaaS companies generate nearly three times the EV/Revenue multiples of bottom-quartile peers, and barely one-third of software companies sustain a Rule of 40 score over time. Their separate analysis of net revenue retention and B2B tech valuation found that top-quartile NRR companies trade at a median 24x EV/Revenue versus 5x for bottom-quartile — a gap driven almost entirely by retention quality.

How to calculate where you sit before a buyer does it for you

Run this exercise before any acquisition conversation, not during one:

- Calculate trailing 12-month ARR growth. Use ending ARR, not bookings, and be consistent about what counts as ARR (exclude one-time services, be explicit about usage-based revenue treatment).

- Calculate NRR on a cohort basis. Take your revenue from customers who existed 12 months ago, and measure what they are paying now, including expansion, contraction, and churn. A single blended number hides which cohorts are actually expanding. Our NRR benchmark guide breaks down the 2025 benchmarks by ACV segment and ARR stage, so you can compare against the right peer set rather than a public-company median that does not apply to your business.

- Calculate your Rule of 40 score. Add YoY revenue growth rate to EBITDA margin (or free cash flow margin, if that is the more honest number for your business). Do this on a GAAP or accrual basis, not cash basis, because that is what a buyer's QoE firm will reconstruct anyway.

- Map yourself against the multiple table above. Be honest about which row you are actually in, not which row your board deck implies.

This is precisely the exercise we build with founders inside a forecasting model review, because it is the same underlying discipline that also answers "what's our runway" and "can we make this hire." Acquisition readiness is a downstream output of good FP&A, not a separate project you start six months before a sale.

How to interpret what you're seeing in early conversations

Numbers alone do not tell you whether a specific conversation is real or exploratory. Watch for these signals.

Signs the interest is serious:

- The buyer asks for specific cohort or unit economics data, not just a headline ARR number.

- They involve a corporate development function, not just a product or partnerships contact.

- They propose a timeline and want to talk about structure (asset, stock, or merger) early.

- They ask what you would need to see to consider a deal, rather than only pitching you on theirs.

Signs you're being used for intelligence, not a deal:

- Every conversation stays in "partnership" language even after multiple meetings.

- They want your metrics and roadmap but resist sharing anything specific about their own plans or timeline.

- There is no path to a decision-maker, only a rotating cast of individual contributors.

If you cannot tell which mode you are in, slow down. Loop in your board, get a management-level view of your own numbers in order first, and consider at least an initial conversation with an M&A attorney before you share anything beyond public information. Your leverage is highest right now, before a buyer has learned where your soft spots are.

What to do in the 90 to 180 days before you engage a buyer

You do not need a banker to start this work. You need a finance function that produces defensible numbers on a predictable cadence. Our due diligence checklist for startups covers the full document-level preparation, but the items below are the ones that specifically move acquisition outcomes.

- Reconcile your metrics definitions across every deck. If your board deck, your CRM, and your finance system define ARR, NRR, or CAC differently, a buyer's diligence team will find the gap and use it to justify a lower offer or a re-trade.

- Move from cash-basis to accrual-basis reporting if you have not already. Buyers and their QoE advisors will rebuild your P&L on an accrual basis regardless. Doing it yourself first means you control the narrative instead of reacting to their version. As Grant Thornton explains, a quality of earnings analysis is not a financial audit — it is a transaction-focused review that normalizes reported earnings for economic sustainability, and the adjustments it produces can materially change the EBITDA figure your deal is priced on.

- Build (or rebuild) a 12 to 18 month cash flow and runway forecast with explicit assumptions. Not a single-point projection. A range, with the assumptions behind churn, expansion, hiring, and pricing made visible, so a buyer sees a management team that understands its own model rather than one presenting a number it cannot defend.

- Document customer concentration and contract terms. Change-of-control provisions in your top customer contracts can materially affect deal certainty. Know which contracts have them before a buyer finds out during diligence.

- Assign clear functional ownership of recurring explanations. If every answer about churn, pipeline, or margin lives only in the founder's head, buyers price in owner-dependency risk. Move that knowledge into documented reporting owned by named people.

- Get your cap table fully diluted and current. Messy cap tables, missed consents, and incomplete IP assignments are among the most common reasons deals stall or die, and none of them are hard to fix if you start early.

Common mistakes and the better move

| Mistake | What it costs you | Replacement move |

|---|---|---|

| Treating legal and financial cleanup as "paperwork" to handle later | Lower price, longer diligence, or a dead deal when issues surface late | Treat data room readiness as an economic decision, not an admin task, starting 12+ months out |

| Presenting a single-point revenue forecast | Buyers discount it because it looks like a pitch, not a model | Present a range with explicit assumptions on churn, expansion, and hiring, the same discipline used in board reporting |

| Negotiating with one buyer only | Weaker terms across price, escrow, and indemnification | Run even an informal dual-track process; competitive tension is the most reliable lever on both price and terms |

| Letting metrics definitions vary between the board deck, CRM, and finance system | Diligence finds the inconsistency and reprices the deal or triggers a re-trade | Standardize metric definitions once, document them, and use the same definitions everywhere |

| Losing negotiating leverage by signing an LOI before terms are fully aligned | Leverage drops sharply once you're in exclusivity | Push to resolve economic terms, not just headline price, before signing the LOI |

| Keeping key operational knowledge only in the founder's head | Buyers price in owner-dependency risk and discount the offer | Document recurring explanations and assign functional owners before outreach begins |

| Waiting until a term sheet arrives to build a real forecast | Scrambling under diligence pressure, mistakes, credibility loss | Build and stress-test your forecasting model well before any acquisition conversation starts |

Research from Wharton reinforces how preventable most of these failures are: studies suggest 70-90% of deals underperform expectations, and the root causes trace back to identifiable mistakes in diligence, synergy assessment, and integration — not market timing or bad luck. A separate Fortune analysis of 40,000 deals over 40 years puts the failure rate at 70-75%, with the same conclusion: the causes are structural and addressable before the LOI, not after.

The practical asset: a finance-side acquisition readiness checklist

Use this as a gate before you engage seriously with any buyer, inbound or proactive. For the full document-level version, see our due diligence checklist for startups.

Financial

- Three years of P&L, balance sheet, and cash flow statements, reconciled to accrual accounting

- Current-year monthly actuals vs. budget, with variance explanations

- ARR, NRR, and CAC calculated on documented, consistent definitions across finance, sales, and the board deck

- Cohort-level revenue retention analysis, not just a blended NRR figure

- Customer concentration breakdown, with contract-level detail on any customer above 10% of revenue

- A 12 to 18 month cash flow and runway forecast built on explicit, stated assumptions

Legal and cap table

- Fully diluted cap table, current and reconciled to option grants and board minutes

- Complete IP assignment documentation from every founder, employee, and contractor

- Material contracts flagged for change-of-control provisions

- No unresolved litigation or unaddressed regulatory exposure

Operational

- Org chart with named owners for the explanations buyers will ask for repeatedly (churn, margin, pipeline)

- Documented technical architecture, key dependencies, and security posture

- A clear answer to what breaks if the founder is unavailable for two weeks

If more than a handful of these items are missing or live only in someone's memory, you are not ready to engage a serious buyer yet, no matter how attractive the inbound interest looks this quarter.

Conclusion

A startup acquisition process rewards the same discipline that good FP&A rewards every month of the year: consistent metrics definitions, a forecast built on stated assumptions instead of hope, and financial data that holds up when someone outside the company tries to break it. The deal terms, the multiple, and the speed to close are downstream of that discipline, not separate from it.

Most $5-50M ARR companies do not have a banker problem or a lawyer problem when a deal stalls. They have a decision-quality and forecasting problem that was already there before the acquisition conversation started, and diligence is simply the moment it becomes visible to someone with leverage over the price.

If you want a clear read on whether your metrics definitions and forecasting model would survive that kind of scrutiny today, audit your metrics definitions and forecasting model with Fiscallion before a buyer, or your board, forces the question.