Conflating bookings with revenue is one of the most expensive reporting mistakes a scaling SaaS company can make. It rarely happens because the terms are hard to define; it happens because leadership teams use them interchangeably in conversation. When bookings, billings, and recognized revenue are treated as synonyms, every downstream calculation corrupts. Runway models baseline against cash that hasn't been collected, headcount scales against revenue that hasn't been earned, and board narratives drift away from GAAP reality.

This guide delivers the CFO-level discipline required to isolate all three metrics, align your tracking systems, and ensure your strategic decisions match your actual financial position.

Key takeaways

- Bookings are the total value of contracts signed in a period. They are a leading indicator of future revenue, not revenue itself. Treat them as a sales performance metric.

- Billings are invoices sent. They affect your cash flow and deferred revenue balance but do not equal recognized revenue.

- Revenue (GAAP recognized revenue) is earned only when the performance obligation is fulfilled under ASC 606. It is the number that belongs on your income statement.

- The bookings-to-revenue ratio tells you whether your sales pipeline is outpacing delivery. A ratio above 1.0 signals growth momentum. A ratio declining toward 1.0 signals a pipeline slowdown.

- The 3-3-2-2-2 rule is a venture-scale ARR trajectory benchmark, not a universal target. It implies 200% YoY growth in the tripling years, which describes the top tier of venture-backed SaaS companies.

- Confusing these three metrics does not just create reporting noise. It causes founders to misread cash position, overhire into assumed revenue, and walk into board meetings with numbers investors will immediately challenge.

What we'll cover

- The three metrics defined and distinguished

- How each flows through your financial statement

- How to calculate bookings, billings, and revenue

- How to calculate and interpret the bookings-to-revenue ratio

- What the 3-3-2-2-2 rule is and what it demands from your trajectory

- Common mistakes and the decisions they break

- A practical metrics dashboard outline

Three metrics, three different signals

Founders at $5M–$50M ARR typically have some version of all three metrics tracked somewhere — in a CRM, a billing system, and an accounting platform. The problem is that they rarely sit in the same model, defined consistently, with a single owner accountable for the inputs.

The result: "revenue" conversations where three people in the same room are each quoting a different number, all of them technically correct.

Here is how to keep them distinct.

Bookings: the contract is signed, the work has not started

A booking is the total contracted value of a signed agreement. It records a customer commitment, not an economic event. The moment a contract is executed, the full value becomes a booking — regardless of when the invoice goes out, when cash arrives, or when the service is delivered.

For a $36,000 three-year enterprise contract signed in January, the booking is $36,000 in January. Nothing else has happened yet from an accounting perspective.

Types of bookings to track separately:

The most common mistake: reporting total TCV bookings as a proxy for ARR momentum. A single three-year deal worth $150K TCV looks like $150K in bookings — but it only contributes $50K to ARR.

According to Aleksandar Stojanovic, CEO & Founder at Fiscallion, this is exactly where the psychological trap springs shut. "The engineering and headcount burn gets scaled to the bookings story, while the cash and recognized revenue that actually support that burn lag far behind," Stojanovic explains.

To prevent booking hype from corrupting internal resource allocations, he implements a strict internal rule: celebrate the grand total bookings numbers externally and to the board, but anchor all absolute headcount and burn decisions entirely to recognized monthly revenue and verified cash position.

Billings: the invoice goes out

Billings are the dollar amount invoiced to customers in a period. For annual contracts paid upfront, billings hit in full at the start of the contract. For monthly subscribers, billings equal one month of the contract value.

Billings affect:

- Cash flow — when you collect determines your actual cash position

- Accounts receivable — if the invoice is issued but unpaid, it sits here. For a deeper look at how to manage that gap and protect runway, the accounts receivable management guide for SaaS startups covers DSO, collections, and cash flow mechanics.

- Deferred revenue — when cash arrives before service delivery, the unearned portion sits on the balance sheet as deferred revenue

Billings are not the same as cash collected (customers may pay late) and not the same as recognized revenue (service must still be delivered). They occupy the middle position in the flow from commitment to cash to earnings.

Revenue: the service is earned

Revenue — specifically GAAP-recognized revenue — is recorded only after your performance obligation is fulfilled. Under ASC 606, that means when you have delivered the promised service or product.

For a $12,000 annual subscription starting January 1, you recognize $1,000 per month regardless of when cash arrives. This is the number that belongs on your income statement, informs your gross margin calculation, and drives your ARR figure when annualized consistently.

Deferred revenue is the balance-sheet consequence of collecting cash before earning it. When a customer pays $12,000 upfront for a 12-month subscription, you receive the cash, record it as deferred revenue, and recognize $1,000 per month as you deliver the service. For a full treatment of how that deferred balance builds, flows, and interacts with your cash position, see the deferred revenue in SaaS guide.

For a deeper look at how ASC 606 governs when and how you record this, and the specific five-step framework that applies to SaaS contracts, the mechanics are covered in the revenue recognition in SaaS guide.

How each metric flows through your financial statements

This is the part most financial conversations skip — which is why the same confusion recurs.

This explains why a company can show strong bookings growth, a healthy deferred revenue balance, and still face a cash crunch — if billing cycles are misaligned with expense timing or if payment terms allow 45-60 day delays on annual invoices.

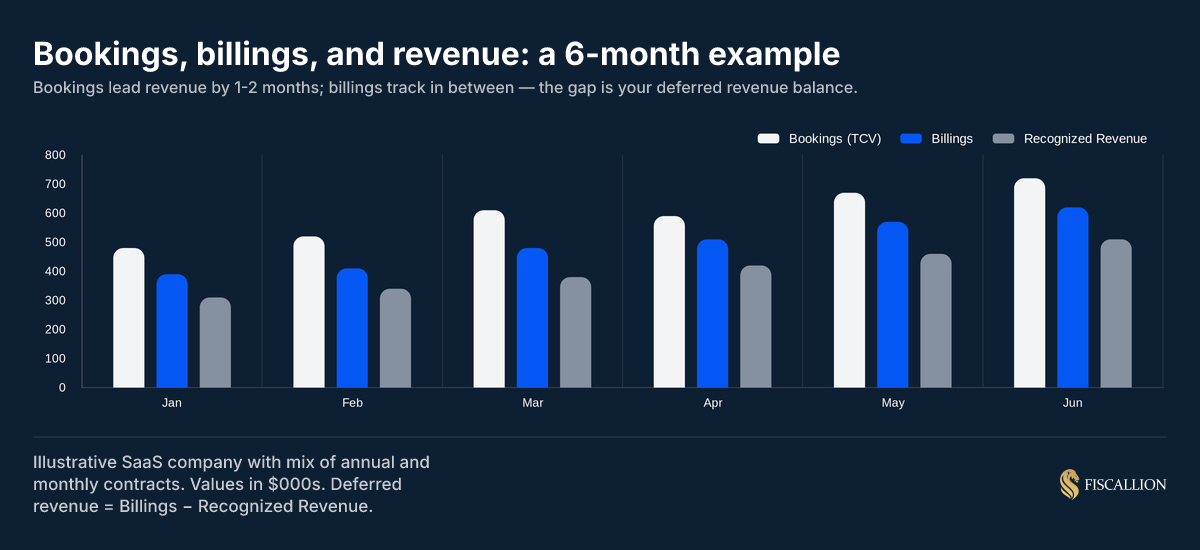

The chart above illustrates how the three metrics move in relation to each other over a six-month period for a company with a mix of annual and monthly contracts. Bookings lead the series, billings track in the middle, and recognized revenue follows — the gap between billings and revenue is your deferred revenue balance at any point in time.

How to calculate each metric

Calculating bookings

Period bookings = Sum of all new contract values signed in the period

For a mixed contract portfolio, calculate separately:

- New bookings (ACV of new customer contracts)

- Expansion bookings (incremental ACV from upgrades)

- Renewal bookings (ACV of renewed contracts)

- Net new bookings = New + Expansion - Contraction - Churned bookings

Practical pitfall: Multi-year contracts inflate TCV bookings relative to ACV bookings. Always report both, and be explicit about which one you're quoting in a board deck or investor update. Investors pricing ARR growth will normalize to ACV.

Calculating billings

Period billings = Sum of all invoices issued in the period

For SaaS businesses with a mix of billing terms:

- Monthly subscribers: billings = 1 month of contract value per account

- Annual upfront: billings = full annual contract value at the start of the contract

- Multi-year: billings depend on payment schedule (annual installments vs. full TCV upfront)

Practical pitfall: Companies that shift their billing mix — for example, by pushing customers toward annual plans to improve cash flow — will see billings grow faster than recognized revenue. That is expected and healthy. The deferred revenue balance grows with it. The mistake is treating the billings growth as a revenue acceleration.

Artificially accelerating your cash inflows by locking up multi-year contract payments upfront can mask flat consumer demand. Unless your finance model maps the exact month this frontloaded capital rolls off, you risk running face-first into a devastating liquidity gap.

Calculating revenue (GAAP recognized)

Period revenue = Sum of contract value earned in the period based on service delivery

For a subscription SaaS product:

- Monthly subscriber paying $1,200/year on a monthly plan: $100 revenue per month

- Annual subscriber paying $12,000 upfront: $1,000 revenue per month over 12 months

- Multi-year contract with $36,000 TCV: $1,000 revenue per month over 36 months

Practical pitfall: Usage-based pricing components complicate this. Revenue recognition under a usage model requires estimating usage — which introduces variability the other models do not. If you have a material usage-based component, the recognition method needs to be explicitly defined and consistently applied. KPMG's handbook on revenue for software and SaaS covers how variable consideration and usage-based arrangements are handled under ASC 606.

For a practical grounding in how bookkeeping and accounting handle the deferred revenue mechanics and COGS classification separately — and why conflating those two functions creates gaps — the SaaS bookkeeping vs. accounting breakdown is worth reading.

The bookings-to-revenue ratio: what it tells you and how to calculate it

The bookings-to-revenue ratio, also called the book-to-bill ratio, compares new business secured against revenue recognized in the same period.

Bookings-to-revenue ratio = Total bookings / Total recognized revenue (same period)

Example calculation

- Q1 ACV bookings: $480,000

- Q1 recognized revenue: $310,000

- Bookings-to-revenue ratio: $480K / $310K = 1.55

A ratio of 1.55 means you are signing new business 55% faster than you are recognizing it — a strong signal of future revenue growth, assuming conversion rates and onboarding timelines stay stable.

How to interpret the ratio

What the ratio does not tell you: it does not distinguish between new bookings and renewal bookings. A high ratio driven entirely by renewals means your sales engine has stalled even while the number looks good. Break it down by booking type before drawing conclusions.

Factors that move the ratio

Sales cycle length: Enterprise deals with 3-6 month sales cycles create a natural lag — bookings precede revenue by the length of the implementation period plus the recognition lag. A ratio of 1.5+ can be structurally normal for an enterprise-motion company and not signal exceptional demand.

Billing terms: Moving customers to annual upfront billing increases billings without accelerating recognized revenue. The ratio will rise as a byproduct of billing term changes, not sales acceleration. Isolate that effect before drawing conclusions.

Seasonal patterns: If your market has Q4 enterprise budget cycles, bookings spike in October-December and revenue catches up in Q1-Q2. Compare your ratio to the same quarter in the prior year, not the prior quarter.

Contract mix: An increase in multi-year TCV bookings inflates the numerator relative to a stable monthly revenue base. ACV-normalized bookings are a more stable basis for the ratio at companies with variable contract lengths.

What is the 3-3-2-2-2 rule of SaaS?

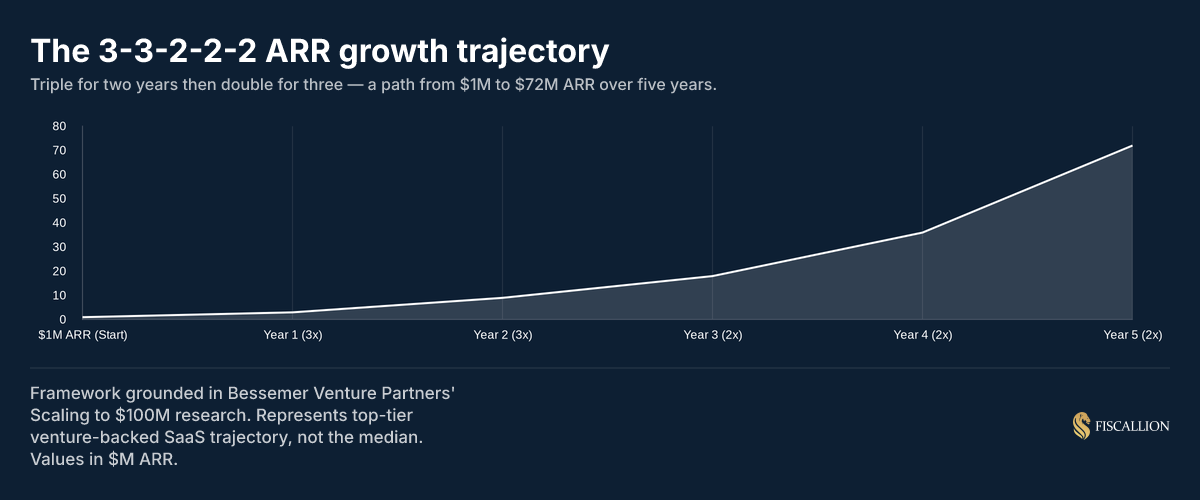

The 3-3-2-2-2 rule is a revenue growth trajectory benchmark used primarily in venture-backed SaaS. Starting from approximately $1M ARR, it describes a five-year compounding path: triple ARR for two consecutive years, then double it for three consecutive years.

The ARR path it implies:

The framework comes from Bessemer Venture Partners' research on companies that scaled to $100M ARR. It represents the top tier of venture-backed SaaS performance — not the median. Bessemer's data shows the average ARR growth rate across their cloud portfolio at the $1–10M range was approximately 200%, declining to roughly 60% at $50M+ ARR.

What the rule actually demands

The tripling years require 200% YoY ARR growth. That means a company at $3M ARR must add $6M net new ARR in a single year. Achieving that with, say, 15% annual logo churn means the new logo acquisition engine has to cover the churn hole and then generate $6M in net new ARR on top of it. That level of growth is not a function of effort — it requires product-market fit at scale, a repeatable acquisition motion, and strong gross revenue retention operating simultaneously.

The doubling years require 100% YoY ARR growth. At $9M ARR, that means adding another $9M in a year. That is still aggressive — equivalent to growing from zero to $9M in a single year from a standing start.

Most companies at $5M–$50M ARR are not on this trajectory. According to SaaS Capital's 2025 benchmarking report — based on data from over 1,000 private B2B SaaS companies — the median growth rate across all private B2B SaaS registered 25% in 2024, down from 30% in 2023. Equity-backed companies median growth came in at 25%. Neither is close to 200%. The 3-3-2-2-2 rule is calibration for the top few percent of venture-backed SaaS, not a median expectation, and it is not a benchmark bootstrapped companies should hold themselves to.

Where the rule is useful — and where it is not

Useful for:

- Calibrating whether your current growth rate is consistent with a venture-scale outcome

- Reverse-engineering what sales capacity, NRR, and CAC payback are required to hit each step

- Pressure-testing a fundraising narrative with a trajectory a Series B or C investor will immediately check against

Not useful for:

- Setting hiring or spending targets without first validating your unit economics

- Justifying burn multiples above 2x on the grounds that you are on a 3-3-2-2-2 path

- Bootstrapped companies optimizing for capital efficiency and sustainable margins

For a full treatment of the 3-3-2-2-2 benchmarks by ARR band, including how NRR and burn multiple interact with growth rate at each stage, the ARR growth rate benchmark article walks through the numbers the Fiscallion team uses with $5M–$50M ARR clients.

How the 3-3-2-2-2 rule evolved from T2D3

The older T2D3 framework (triple, triple, double, double, double) assumed a starting point of $2M ARR and was built for the low-cost-of-capital environment that characterized 2015-2021. The 3-3-2-2-2 version is functionally the same trajectory but calibrated to a lower starting base and a more capital-efficient environment.

The key difference in practice: 3-3-2-2-2 companies are expected to tighten CAC payback periods to under 12 months during the growth phase, whereas T2D3-era companies routinely accepted 18-24 month paybacks. The growth target is similar. The efficiency expectation is not.

Booking value vs. revenue value: the specific question of deferred revenue

A common point of confusion in financial reporting: a customer signs an annual contract for $120,000, pays upfront, and you record $120,000 in cash. The question that breaks boardroom conversations is: how much of that $120,000 is "revenue"?

On the day the cash arrives, the answer is: none of it — yet.

- Cash received: $120,000 (balance sheet, cash)

- Deferred revenue: $120,000 (balance sheet, liability)

- Recognized revenue, Day 1: $0

- Recognized revenue per month: $10,000 (as service is delivered)

The $120,000 contract value is the "booking value." The recognized revenue accrues at $10,000/month. After three months, you have recognized $30,000 of the $120,000 booking value. The other $90,000 is still deferred.

This distinction matters enormously for three decisions:

- Cash flow planning: You have the cash, but the income statement has not caught up. Your runway calculation should use cash, not recognized revenue, when assessing immediate coverage.

- Gross margin calculation: COGS tied to service delivery is being incurred monthly. If you front-load COGS (onboarding, implementation) but back-load revenue recognition, your early-month gross margins will be depressed.

- Churn accounting: If that customer cancels in month 4, you have recognized $40,000. The remaining $80,000 of deferred revenue is returned (as a refund or credit). Your ARR decreases, your churn rate increases, and your deferred revenue balance decreases — all simultaneously.

The three-statement model is the structure that makes these relationships visible and trackable. The three-statement model guide for startups covers how to connect bookings, billings, deferred revenue, and recognized revenue across the income statement, balance sheet, and cash flow statement in a single model.

What to do next: six actions ordered by impact

1. Audit your definitions and confirm single ownership (Finance, immediate)

Check whether "bookings," "billings," and "revenue" are defined identically in your CRM, billing system, and accounting tool. In most $5M–$50M ARR companies, they are not. Assign a single owner for each metric's definition and input.

2. Build a bookings-to-recognized revenue bridge (Finance, 1–2 weeks)

For each active contract: contract value, billing date, monthly recognition schedule, deferred revenue balance, and remaining revenue to be recognized. This bridge should live in your financial model and update monthly.

3. Normalize bookings to ACV before reporting (Sales + Finance, immediate)

If you are reporting TCV bookings in board decks or investor updates, add an ACV column. Multi-year deals inflate TCV by 2-3x relative to ACV. Investors will normalize to ACV to assess ARR momentum.

4. Separate booking types in your CRM (Sales ops, 2–4 weeks)

Tag each contract as new, renewal, expansion, or non-recurring. Your bookings metric should roll up each type separately. A combined bookings number that mixes all four types tells you very little about which part of the engine is working.

5. Track the bookings-to-revenue ratio quarterly, with context (Finance, ongoing)

Add the ratio to your quarterly board deck alongside the components — not just the ratio itself. Show the trend over four quarters. Explain anomalies (a Q4 enterprise deal spike, a billing term change, a large renewal concentration).

6. Validate the 3-3-2-2-2 benchmark against your actual ARR band (Finance + CEO, quarterly)

If you are at $10M ARR growing at 35%, you are not on a 3-3-2-2-2 trajectory — and your capital deployment, hiring plan, and investor narrative should reflect that honestly. The 3-3-2-2-2 framework is useful for calibration, not for justifying spending patterns that require that trajectory to make economic sense. Use SaaS valuation multiples benchmarks to understand how investors will price your actual growth rate.

Common mistakes and the replacement moves

Mistake 1: Reporting bookings in the revenue line

This happens most often in companies where the CRM feeds directly into a top-level "revenue" dashboard. A $200K TCV enterprise deal closes in Q3, shows up in the dashboard as "$200K revenue this quarter," and everyone congratulates the sales team.

The recognized revenue for that deal in Q3 might be $16,700 (two months of a 12-month contract at $100K ACV). The rest is deferred.

Replacement: Revenue in your financial model and board reporting always refers to GAAP-recognized revenue. Bookings live in a separate sales performance section. The two numbers are both reported, both labeled clearly, and never combined.

Mistake 2: Planning headcount based on bookings, not revenue

A common sequence: Q4 bookings surge. CEO uses the bookings total to justify an accelerated hiring plan starting January. Recognized revenue will not catch up until Q2 or Q3. Cash from annual contracts may have arrived, but income is not yet earned. If churn is running above expectations, some of those bookings will not fully recognize.

Replacement: Headcount planning should be grounded in recognized revenue trajectory and cash runway — not bookings. Use bookings as a leading indicator for capacity planning (you will need more CSMs as contracts onboard), but validate each hire against the recognized revenue that will fund it.

Mistake 3: Using the bookings-to-revenue ratio without segmenting booking type

A ratio of 1.4 looks healthy. But if 80% of those bookings are renewals, the ratio is telling you that your existing base is stable — not that new logo growth is strong. New logo bookings may be flat or declining, completely masked by a renewal surge.

Replacement: Break the ratio into new logo bookings vs. total bookings separately. Track new ACV bookings as a standalone metric, distinct from renewals and expansions. A strong NRR benchmark helps distinguish between retention-driven and acquisition-driven growth.

Mistake 4: Treating high deferred revenue as a revenue cushion

Deferred revenue is a liability, not a safety net. It represents an obligation you still have to fulfill. If customers who have prepaid cancel at higher rates than expected, your deferred revenue balance declines as you either refund or credit them — and your ARR falls simultaneously.

Replacement: Model deferred revenue alongside gross revenue retention. A deferred revenue balance that is growing while GRR is slipping is a warning sign, not a positive signal.

Mistake 5: Applying 3-3-2-2-2 as a universal benchmark

The 3-3-2-2-2 trajectory is sometimes used in board decks to signal ambition rather than as a grounded forecast. If your growth rate is 35% YoY at $12M ARR, calling out a 3-3-2-2-2 path in a fundraising narrative without the unit economics to support it will create more skepticism than confidence.

Replacement: Use the 3-3-2-2-2 benchmark to diagnose your position relative to the venture-scale path — and to make explicit the trade-offs if you are not on it. "We are not on a 3-3-2-2-2 trajectory; we are targeting 60% YoY growth with a 1.2x burn multiple and 110% NRR" is a more credible investor story than a trajectory claim that the numbers do not support.

Your bookings, billings, and revenue dashboard: a working outline

Most $5M–$50M ARR companies have pieces of this data in multiple systems. The goal is one model where all three metrics are defined consistently and the relationships between them are visible.

Every cell in this table needs an owner, not just a data source. The difference between a metrics dashboard that improves decisions and one that produces reporting overhead is whether someone is accountable for the input definition — not just the output number.

Frequently asked questions

What is the difference between bookings and revenue?

Bookings represent the total value of contracts a customer has committed to. Revenue is the amount you have actually earned by delivering your service under those contracts. A $60,000 two-year contract is $60,000 in bookings and $2,500 per month in recognized revenue. The booking is recorded when the contract is signed; revenue is recorded as the service is delivered, typically monthly.

What is the difference between booking value and revenue?

Booking value is the total contracted dollar amount — often TCV (total contract value) or ACV (annual contract value) — agreed to in a signed contract. Revenue is the portion of that booking that has been earned and recognized on the income statement. For a 12-month contract, booking value and total recognized revenue will ultimately be equal at the end of the term. During the term, recognized revenue will always be less than or equal to the booking value.

What is the 3-3-2-2-2 rule of SaaS?

The 3-3-2-2-2 rule describes a five-year ARR growth trajectory for venture-backed SaaS: triple ARR for years one and two, then double it for years three, four, and five. Starting from $1M ARR, it produces a path to $72M ARR over five years, implying 200% YoY growth during the tripling phase and 100% during the doubling phase. It is grounded in Bessemer Venture Partners' research on companies that reached $100M ARR. It represents the top tier of the distribution, not a median expectation.

How do you calculate the bookings-to-revenue ratio?

Divide total bookings in a period by total recognized revenue in the same period. Example: $600K in Q2 ACV bookings divided by $400K in Q2 recognized revenue = 1.5x ratio. A ratio above 1.0 indicates your pipeline is growing faster than you are recognizing revenue. The ratio should be tracked quarterly, broken out by booking type (new vs. renewal vs. expansion), and compared to the same quarter in the prior year to control for seasonal effects.

Mapping the relationship: commitment, invoicing, and earned income

Bookings, billings, and revenue are three distinct signals about three different stages of the same customer relationship: the commitment, the invoice, and the earned income. Using any one as a substitute for another produces a distorted picture of where the business actually stands.

The practical consequences of that distortion surface in predictable failure modes: runway forecasts built on commitments rather than cash, and hiring plans justified by revenue that hasn't yet been recognized under ASC 606.

The correction is definitional discipline: separate metrics, separate owners, separate treatment in every model and every communication. That structure is what allows bookings growth to mean what it is supposed to mean — a signal of future revenue, not current earnings.

At Fiscallion, the first diagnostic step with any new $5M–$50M ARR client is to audit how these three numbers are defined across their CRM, billing tool, and accounting system. In most cases, they are different. The fix takes days. The clarity it produces is immediate.

Audit your metrics definitions and forecasting model — and leave the engagement knowing exactly which inputs are fragile and which assumptions need an owner.