Deferred revenue touches almost every decision that matters - runway forecasting, board reporting, pricing, and headcount capacity. Yet most founders treat it as an accounting formality rather than a planning tool.

This article gives you the full picture: what deferred revenue is, why it shows up as a liability, how it interacts with cash flow and runway, and what it signals when it moves in the wrong direction. By the end, you will know exactly how to use it in FP&A - not just how to define it for an auditor.

Key takeaways

- Deferred revenue is a liability, not a revenue boost. Cash collected from annual prepays sits on the balance sheet until you deliver the service.

- The gap between your cash balance and your recognized revenue is where most runway forecasting errors live.

- Deferred revenue growth is a positive signal - but only when renewal rates hold and margins don't erode from delivery costs.

- The Rule of 40, the 3-3-2-2-2 benchmark, and SaaS capitalization rules all interact with how you recognize and report deferred revenue.

What we'll cover

- What deferred revenue is and why it is classified as a liability

- How ASC 606 governs revenue recognition in SaaS

- The balance sheet and cash flow mechanics

- How to calculate and track it month over month

- What the 3-3-2-2-2 rule and Rule of 40 have to do with deferred revenue

- Whether SaaS costs are capitalized or expensed

- Common FP&A mistakes and the corrective moves

- A deferred revenue tracking template you can build today

Deferred revenue is a liability because you still owe the service

Deferred revenue - sometimes called unearned revenue - is cash you have collected for a product or service you have not yet fully delivered. Under US GAAP, that creates an obligation. Until you deliver, the money is not yours to recognize as revenue.

For a SaaS company, the most common trigger is an annual subscription paid upfront. A customer pays $24,000 in January for a 12-month contract. You do not recognize $24,000 in January. You recognize $2,000 per month as you deliver the service. The remaining $22,000 at the end of January sits on the balance sheet as a current liability.

This matters for three reasons beyond compliance:

- Cash ≠ revenue. Your bank account may show a strong January, but your income statement does not. Founders who confuse the two build burn models on the wrong number.

- Renewal risk is baked in. The liability will unwind - either through recognized revenue or through a refund if the customer churns. Deferred revenue is future revenue only if you retain the customer.

- Deferred revenue is a forecasting asset. Because it represents contracted, pre-paid service delivery, it gives you a floor on near-term recognized revenue before counting a single new deal.

How annual vs. monthly billing changes the deferred balance

Monthly plans create almost no deferred revenue because the billing period and the service delivery period are the same. The moment you shift even a fraction of your ARR to annual prepay, your deferred balance grows quickly.

If you are pushing customers toward annual plans to improve cash efficiency - a correct instinct - your deferred revenue balance will rise. The key question is whether your FP&A model reflects that correctly.

How ASC 606 governs revenue recognition in SaaS

The Financial Accounting Standards Board's ASC 606 standard, effective since 2018 for private companies, requires you to recognize revenue when - and only when - you satisfy a performance obligation. For SaaS, that is typically a ratable, straight-line recognition over the subscription period.

The five-step ASC 606 model:

- Identify the contract. Is there a signed agreement, accepted order, or enforceable commitment?

- Identify the performance obligations. For a SaaS subscription, the primary obligation is continuous access to the platform. Setup fees, professional services, and training may be separate obligations.

- Determine the transaction price. Include variable consideration, discounts, and refund estimates.

- Allocate the price to obligations. If you bundle a subscription with onboarding, you need to allocate the contract value based on standalone selling prices.

- Recognize revenue as obligations are satisfied. For a subscription, this happens ratably over the term.

Termination clauses create a compliance trap. If your contract allows the customer to cancel at any time and receive a pro-rata refund, the noncancelable portion of the contract is what gets accounted for under ASC 606. A monthly cancel-anytime contract is effectively a month-to-month contract for recognition purposes - even if customers almost never cancel. This directly affects how much deferred revenue you can legitimately carry.

Non-refundable upfront fees require judgment. If you charge a setup or onboarding fee that does not represent a distinct standalone deliverable, that fee must be recognized over the subscription term, not at contract start. As Aprio's analysis of ASC 606 adoption notes, many early-stage SaaS companies get this wrong and overstate revenue at deal close — particularly when implementation fees are waived and contract consideration must be reallocated across performance obligations based on standalone selling prices.

The deferred revenue waterfall: how the balance moves

The cleanest way to track deferred revenue is through a monthly waterfall that shows four lines:

If you run this waterfall alongside your ARR bridge, you get a coherent picture of where your revenue is coming from - new bookings, renewals, expansions, or the release of prior-period deferred balances.

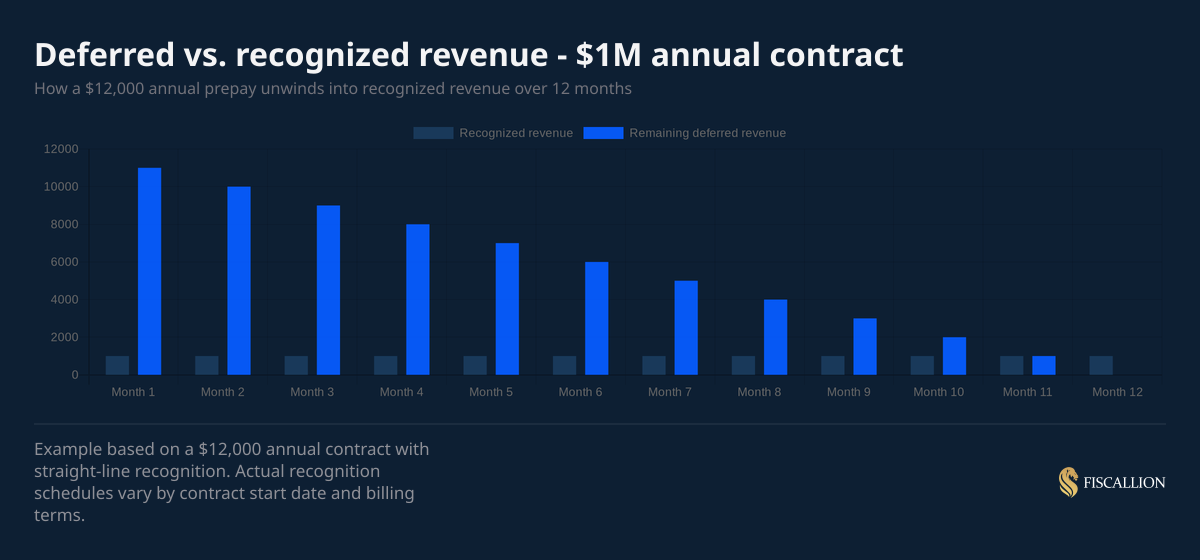

The chart above shows a single $12,000 annual contract unwinding over 12 months. Scale this to your full annual cohort and the deferred balance at any point tells you how much contracted revenue is still ahead of you.

Where deferred revenue appears on your financial statements

The cash flow statement treatment is where most founders get confused. If your deferred balance grew by $500,000 this quarter, that $500,000 shows up as a positive line in operating cash flow - even though you haven't earned it yet. This inflates operating cash flow relative to what your income statement shows. Investors who track free cash flow will often normalize for this.

Is SaaS capitalized or expensed?

This question comes up in two contexts: costs your customers incur to implement your product, and costs you incur to build it. The answer is different for each.

From the customer's perspective: SaaS implementation costs

Under ASC 350-40, customers implementing a cloud-based SaaS arrangement that is a service contract - meaning they do not control the underlying software - must evaluate which implementation costs to capitalize. KPMG's handbook on software and website costs provides extensive practical guidance on how the three-stage model applies across different implementation scenarios.

The guidance breaks the implementation into three stages:

For your own company, this matters when you are selling to enterprise buyers who scrutinize your pricing against their internal capitalization policy.

From the SaaS vendor's perspective: your own software development costs

Under ASC 350-40 (internal-use software) and ASC 985-20 (software sold to customers), costs you incur to build your platform fall into a similar three-stage model:

- Preliminary and post-implementation: Expensed as incurred

- Application development: Capitalized, then amortized over the useful life (typically 2-5 years)

The practical implication for your FP&A model: if your engineering team is building new product features, a portion of those salaries may qualify for capitalization. This reduces your GAAP operating expenses in the near term but creates an amortization charge over future periods. It also directly affects your EBITDA margin and, therefore, your Rule of 40 score. Note that Baker Tilly's updated guidance on internal-use software reflects 2025 amendments to ASC 350-40 that affect how certain cloud-enabled software costs are staged — worth reviewing if your accounting policy predates those changes.

Contract acquisition costs (CAC) under ASC 340: Commissions paid to close new contracts must be capitalized and amortized over the expected customer benefit period - often the expected customer life or the contract term. This is not optional for companies following US GAAP. Recurly's breakdown of ASC 340-40 is a practical reference for understanding exactly which commission types qualify and how to determine the correct amortization period. If your finance team is expensing all commissions immediately, your income statement is understating the cost of revenue in the closing period and overstating it in future periods.

What is the Rule of 40 for SaaS?

The Rule of 40 is the simplest test of whether a SaaS company is balancing growth and profitability at an acceptable rate. Add your annual revenue growth rate (as a percentage) to your EBITDA margin (as a percentage). If the sum is 40 or above, the company is performing within investor-grade health thresholds.

Formula: Revenue growth rate (%) + EBITDA margin (%) ≥ 40

Interpreting the result

A company growing at 60% ARR and running at -20% EBITDA margin scores 40. A company growing at 15% and running at 28% EBITDA margin also scores 43. Both pass, but they reflect fundamentally different capital strategies and risk profiles. Do not use the Rule of 40 as a standalone pass/fail - use it alongside NRR, gross margin, and CAC payback to understand what is driving the number.

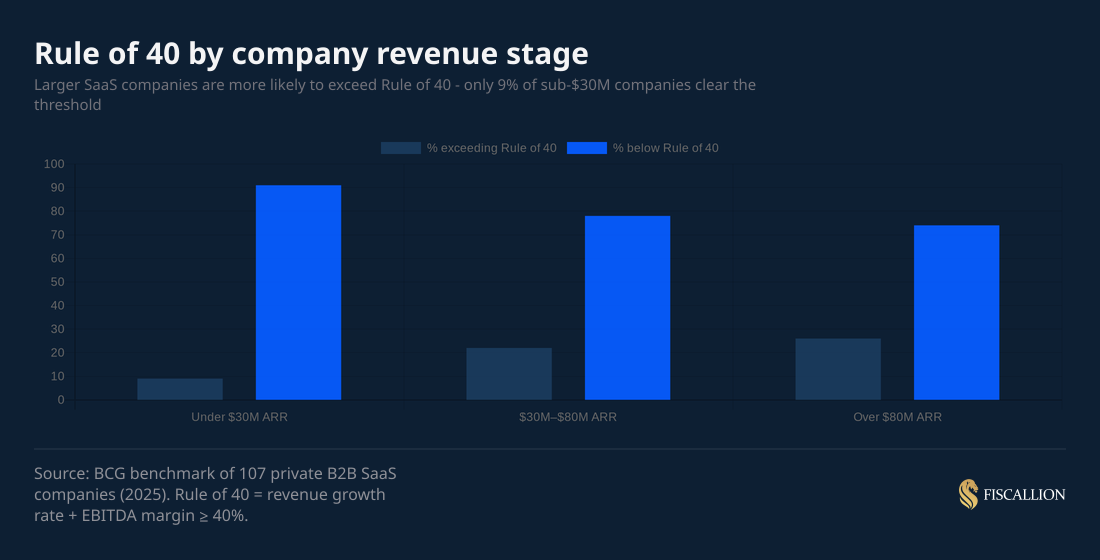

BCG's 2025 benchmark of 107 private B2B SaaS companies found that only 9% of companies under $30M ARR exceeded a Rule of 40 score. That jumps to 26% for companies above $80M ARR. The gap is partly structural - smaller companies carry higher relative sales and marketing expense, higher product R&D as a percent of revenue, and lower gross margins. BCG's analysis also pinpoints that companies with high gross revenue retention (GRR) and lower new-customer ACV — what they call "keepers" — are the cohort most consistently exceeding Rule of 40 targets.

A separate SaaS Capital analysis of private SaaS companies found that Rule of 40 scores have contracted noticeably over the past two years, driven primarily by slowing revenue growth rates rather than margin deterioration. The implication: retention quality matters more than deal size, and growth-rate headwinds are now the primary lever to watch.

How deferred revenue interacts with the Rule of 40

Deferred revenue affects both sides of the Rule of 40 equation:

- Revenue growth rate: If you bill heavily upfront in Q4, your ARR may look strong but recognized revenue - the number used in the growth rate calculation - may lag billings. Companies that shift from monthly to annual billing see a temporary spike in deferred balance that can make YoY growth rates look lower than ARR growth.

- EBITDA margin: Capitalized contract costs (commissions amortized under ASC 340) and capitalized software development reduce current-period GAAP expenses, which inflates EBITDA margin. Understand what is in your EBITDA before benchmarking against the Rule of 40.

What is the 3-3-2-2-2 rule of SaaS?

The 3-3-2-2-2 rule is a revenue growth benchmark for venture-backed SaaS companies. Starting from approximately $1M ARR, you aim to triple revenue for two consecutive years, then double it for three more years. The trajectory points to roughly $72M ARR at the end of year five.

It evolved from the older T2D3 framework (triple, triple, double, double, double), which assumed a $2-3M ARR starting point and heavy upfront capital. The 3-3-2-2-2 model reflects a more capital-efficient environment where investors favor sustainable growth over burn-funded velocity.

What this benchmark actually demands from your finance model

The 3-3-2-2-2 rule is not a marketing narrative - it is a forcing function for financial decision-making. Each year's target creates downstream pressure on:

- CAC payback period: At 3x growth, you are typically adding more new customers than you have ever had. If your CAC payback is 18 months, you will consume significant cash before those customers contribute margin. At scale, payback needs to compress toward 12 months or below.

- Headcount model: Tripling ARR does not mean tripling headcount. If it does, your Rule of 40 collapses. Companies that hit 3x growth efficiently do it through GTM improvements, pricing expansion, and product-led acquisition - not by hiring proportionally.

- Deferred revenue mix: As you close more annual contracts to support growth targets, your deferred revenue balance will grow. If you are funding the business partly on the float from annual prepays, you need to model what happens to cash when renewal rates soften by even 5%.

When the 3-3-2-2-2 rule does not apply to you

This benchmark is built for venture-backed SaaS aiming at institutional exits. If you are:

- Bootstrapped or capital-light with a profitability mandate rather than a growth-at-any-cost target

- Serving a niche vertical with a finite addressable market

- Running a high-services-delivery model where each new customer requires substantial implementation effort

...then the 3-3-2-2-2 trajectory is the wrong reference point. What matters is whether your growth rate is sufficient to sustain margin improvement and remain competitive in your segment - not whether it matches a VC-era template.

How deferred revenue distorts cash flow visibility

This is the most underappreciated FP&A problem in SaaS. Your operating cash flow can look strong when deferred revenue is growing - because cash is coming in faster than revenue is being earned. But that same dynamic reverses when billings slow.

A company came out of a strong Q4 with a large proportion of annual prepay contracts. Cash looked healthy, recognized revenue was holding steady, and the board felt comfortable. What the P&L wasn't showing was that new pipeline generation in January and February was running at 55% of the prior year's rate — a demand problem that the deferred float was masking entirely.

This pattern is not hypothetical. It is what happens when teams track cash or recognized revenue in isolation without connecting the two through a deferred revenue bridge. Runway's step-by-step guide to SaaS revenue forecasting walks through how recognized revenue, billings, and deferred balances need to flow together inside a coherent forecasting model — the same architecture that prevents this kind of runway surprise.

The three-statement model you actually need

If you are between $5M and $50M ARR, your FP&A model should connect these items explicitly:

- ARR bridge - tracks new, expansion, contraction, and churn each period

- Deferred revenue waterfall - tracks opening balance, new deferred, recognized, and closing balance

- Cash flow bridge - connects billings, collections, and cash with the income statement through the deferred revenue movement

When all three are live and reconciled, you can answer the question that boards actually care about: "How much of next quarter's revenue is already in the bank, and how much depends on deals that have not closed yet?"

FP&A actions ordered by decision impact

If you run a SaaS company and you are not currently tracking deferred revenue with this level of precision, here is where to start - ordered by the impact on decisions you make in the next 90 days.

1. Build the deferred revenue waterfall (owner: head of finance or controller)

Create a monthly schedule that shows opening balance, new deferred from billings, revenue recognized, and closing balance. This single schedule resolves most confusion between cash and revenue. If your billing system exports invoice data, this can be automated.

2. Identify every revenue stream that creates a deferred balance (owner: finance + operations)

Annual subscriptions are obvious. But also audit: multi-year contracts, prepaid usage credits, setup fees bundled into ARR, seat commitments invoiced quarterly in advance, and any minimum revenue guarantees. Each creates a deferred obligation with its own recognition schedule.

3. Reconcile your deferred balance against billings and ARR quarterly (owner: finance)

If your deferred revenue balance is not moving in the direction your ARR bridge predicts, something is wrong - either in the billing system, the recognition schedule, or the contract terms. This reconciliation is the equivalent of a bank statement review for your revenue model.

4. Include deferred revenue movement in your board reporting (owner: CEO + finance)

Your board should see three numbers alongside ARR: total billings, ending deferred balance, and the change in deferred from prior period. This connects the deals you closed to the revenue you can actually recognize. It is also the data investors use when modeling your revenue quality.

5. Model the cash impact of shifting billing mix (owner: CEO + finance)

If you are considering moving customers from monthly to annual billing, build a 12-month cash bridge before you decide on the discount to offer. Annual prepay improves cash but increases your refund obligation. The model should show the break-even discount rate and the cash impact at each renewal cohort.

6. Audit your commission capitalization under ASC 340 (owner: controller or external accountant)

If your company follows US GAAP and you are expensing all sales commissions at close, your current income statement does not reflect the economics correctly. Depending on your contract length and average commission rate, this can be a material adjustment.

Here's an example: In a Series B process, the investor's diligence team flagged that the company had been expensing all sales commissions on a cash basis rather than capitalizing them under ASC 606. Restating to correct the treatment improved EBITDA margin by approximately 6 points for the trailing twelve months. But the favorable restatement triggered a harder conversation about what else might need correcting — and added three weeks to the process.

The Aprio ASC 606 and ASC 340 implementation guide covers the most common practical pitfalls — particularly around when commissions qualify for capitalization versus immediate expensing.

7. Stress-test renewal assumptions in your deferred bridge (owner: finance + CEO)

Your deferred balance assumes 100% renewal. Model what happens if 10% of the cohort up for renewal in the next two quarters does not renew. How does that change your recognized revenue forecast for months 4-9? This is not pessimism - it is the scenario your board will ask about during any fundraise.

Common mistakes and the replacement moves

Mistake 1: reporting deferred revenue growth as a revenue win

If your deferred balance grew by $600,000 last quarter, that is a cash inflow, not a revenue event. Reporting it as revenue growth to the board mixes up two completely different signals. Replace this with a billings-versus-recognized-revenue table that shows both numbers side by side.

Mistake 2: using cash balance to estimate runway without adjusting for deferred obligations

Cash in the bank includes prepaid customer payments you still owe service on. If a customer who prepaid $100,000 churns, you owe a refund. Your true runway calculation should subtract the refund exposure embedded in your deferred balance, adjusted for your expected churn rate.

Mistake 3: recognizing setup fees upfront when they are bundled into a subscription contract

If your product requires an implementation or onboarding phase and you charge a fee for it, that fee is part of the subscription performance obligation unless you can separately establish its standalone value. Recognizing it immediately overstates month-one revenue and understates deferred balance.

Mistake 4: treating all deferred revenue as equally high quality

Not all deferred revenue is created equal. A two-year prepay from an enterprise customer with strong product adoption is different from a one-year prepay from a customer who has not logged in since month two. Track deferred revenue by customer health and cohort. This tells you which portion of your future recognized revenue is at renewal risk.

Mistake 5: ignoring the deferred revenue impact on acquisition multiples

When you raise a Series B or run a secondary transaction, acquirers and investors often apply a haircut to deferred revenue on the balance sheet - because they are buying an obligation, not an asset. If you are planning a raise, understand how your deferred balance will be treated in the valuation model. A large deferred balance from annual contracts with strong NRR is a positive signal. A large deferred balance from contracts with high churn at renewal is a liability in every sense.

Deferred revenue tracking template

Use this as the backbone of your monthly close and board reporting package.

DEFERRED REVENUE WATERFALL - [Month / Quarter] Opening deferred revenue balance: $___________ + New deferred revenue created: Annual subscriptions billed: $___________ Multi-year contracts billed: $___________ Prepaid usage credits: $___________ Other (setup fees, etc.): $___________ Total new deferred: $___________ - Revenue recognized from prior deferred:$___________ = Closing deferred revenue balance: $___________ RECONCILIATION

Closing balance - current portion: $___________ (< 12 months remaining)

Closing balance - long-term portion: $___________ (> 12 months remaining) RENEWAL STRESS TEST

Deferred balance at renewal risk (10% churn assumption): $___________

Cash exposure if churn applies: $___________ BOARD REPORTING SUMMARY

Total billings (period): $___________

Total recognized revenue (period): $___________

Change in deferred balance: $___________

Deferred as % of ARR: ___%

This template keeps three audiences aligned: your controller, who needs the accounting reconciliation; your board, who needs the revenue quality signal; and your own planning process, which needs to know how much near-term revenue is already locked in.

Frequently asked questions

What is the 3-3-2-2-2 rule of SaaS?

Starting from approximately $1M ARR, triple revenue in years one and two, then double it for three more years — mapping a path to roughly $72M ARR over five years. It's most relevant for venture-backed companies planning institutional raises. Bootstrapped or niche SaaS businesses should anchor their growth targets to CAC payback and margin structure instead.

Is SaaS capitalized or expensed?

It depends on what cost you're referring to. Software development costs in the application development phase are capitalized under ASC 350-40; preliminary and post-implementation costs are expensed. Sales commissions on contracts longer than one year must be capitalized and amortized under ASC 340 — immediate expensing is not GAAP-compliant. See the full breakdown in the capitalization section above.

What is the Rule of 40 for SaaS?

Revenue growth rate plus EBITDA margin, with 40 or above considered healthy. BCG's 2025 analysis found retention quality matters more than deal size in hitting that threshold. Use it as a directional diagnostic alongside NRR, gross margin, and CAC payback — not as a standalone pass/fail. Full breakdown above.

What is the accounting treatment for SaaS?

Three standards govern most of it: ASC 606 for revenue recognition (ratable over the subscription term), ASC 350-40 and 985-20 for software development costs, and ASC 340-40 for commission capitalization. For companies at $5M–$50M ARR, the priority order is: revenue recognition first, commission capitalization second, software cost allocation third.

Deferred revenue is a planning tool, not an accounting formality

Deferred revenue is not an accounting technicality you hand off to your controller and forget. For a SaaS company between $5M and $50M ARR, it is one of the most information-dense metrics on your balance sheet. It tells you how much future revenue is already committed, where your cash-to-revenue conversion is breaking down, and what your renewal risk exposure looks like in real terms.

The companies that manage it well are not the ones with the cleanest income statements - they are the ones where someone on the leadership team owns the deferred revenue waterfall and connects it to the ARR bridge, the cash model, and the board deck. That connection is what turns financial reporting into a planning tool.

If your current model treats deferred revenue as a line item rather than a decision input, start with the waterfall template above. Get the reconciliation right, then build the stress test. That is the version of the analysis your board wants to see - and the one that gives you the confidence to make hiring, pricing, and runway decisions without second-guessing the numbers.

Audit your metrics definitions and forecasting model - Fiscallion works with Series A to Series C SaaS companies to build the FP&A infrastructure that makes deferred revenue, ARR, and cash flow legible from a single model.