Billings and revenue can both grow in the same quarter while pointing in opposite directions. A company that shifts customers from monthly to annual plans will see billings accelerate, deferred revenue build, and GAAP-recognized revenue hold flat. All three movements are correct. All three mean different things. And if no one in your finance model distinguishes between them, you will make the wrong call on runway, hiring, and board narrative.

This article defines billings precisely, shows you how to calculate it (including the calculated billings formula), explains what billings movements actually signal, and maps the decisions it drives - so you leave with a definition you can act on, not just quote.

Key takeaways

- The Hidden Mix Shift: Faster billings growth looks like a demand spike, but it often just masks changes in your billing mix or contract structures.

- The Definition Trap: Because "billings" sits between revenue and cash, different stakeholders will define it differently unless you enforce a single metric owner.

What we'll cover

- Billings defined - and distinguished from bookings, revenue, and cash

- How billings flow through your financial statements

- The billings formula and the calculated billings formula

- How to interpret billings movements in context

- What billings tell you that revenue does not

- Billing mix and its effect on reported billings

- Common billings mistakes and the replacement moves

- A billings and deferred revenue dashboard outline

Billings defined: the invoice goes out, not the contract or the cash

Billings are the dollar amount invoiced to customers in a period - the formal request for payment. They record a financial event: you issued an invoice. The customer committed to pay when the contract was signed (that is bookings). Cash arrives when the customer pays (that is collections). And you earn the revenue when you deliver the service (that is recognized revenue under ASC 606).

Billings sit between bookings and recognized revenue. For a deeper treatment of how these three signals interact and where each belongs in your model, see the bookings vs. revenue in SaaS guide. They are closer to cash than revenue, because billing precedes collection. But they are not the same as cash - customers may pay late, and payment terms of 30 or 60 days are standard.

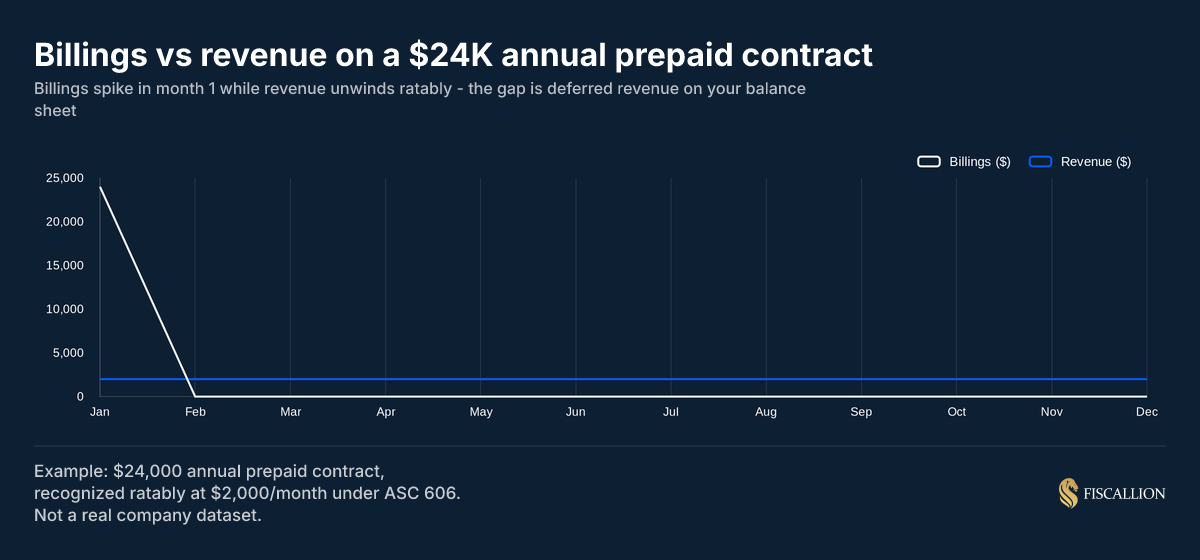

The most important implication: billings for an annual upfront plan hit in full on the first day of the contract. Recognized revenue for that same contract accrues at 1/12 per month. On Day 1, billings = $24,000 and recognized revenue = $2,000. By month 12, total recognized revenue catches up. The gap between them at any point in time is your deferred revenue balance.

How billings flow through your financial statements

When you issue an invoice for an annual subscription paid upfront, three things happen simultaneously on your balance sheet:

- Accounts receivable increases (you are owed money)

- Deferred revenue increases (you have an obligation to deliver service)

- When the customer pays, cash increases and accounts receivable clears

None of those three events touch your income statement. Revenue only moves to the income statement as you deliver service - typically at a straight-line rate over the subscription term. This is the core mechanic of revenue recognition in SaaS under ASC 606.

This is why a company can show strong billings, a growing cash balance, and flat recognized revenue in the same period - and all three are correct. The deferred revenue balance is the connector. It accumulates when billings outpace revenue recognition and unwinds as service is delivered. For a full treatment of how the deferred balance builds, flows through your three statements, and creates FP&A blind spots, see the deferred revenue in SaaS guide.

The reconciliation identity that holds this together:

Billings = Revenue + Change in Deferred Revenue

If your billings were $500K in a quarter and your recognized revenue was $350K, your deferred revenue balance increased by $150K that quarter. If those numbers do not reconcile in your model, your subledger and your general ledger are out of sync.

The chart above illustrates this precisely: on a $24,000 annual prepaid contract, billings hit entirely in month one and recognized revenue flows at $2,000 per month. The declining gap between the cumulative billings spike and the steady revenue ramp is the deferred revenue balance unwinding over twelve months.

The billings formula and how to use it

Direct billings calculation

When you have access to your billing system (Stripe, Chargebee, Recurly, or similar), billings are calculated by summing all invoices issued in the period:

Period billings = Sum of all invoices issued to customers in the period

For a SaaS company with multiple contract types, break this down:

- New customer billings: invoices issued for contracts starting in the period

- Renewal billings: invoices issued at the start of a renewed contract

- Expansion billings: incremental invoices for upsells or seat additions

- Usage-based billings: invoices tied to consumption in the period

Total billings = New + Renewal + Expansion + Usage

The practical pitfall: multi-year contracts with upfront payment. A three-year, $72,000 contract billed entirely in year one will contribute $72,000 to year-one billings. If you are comparing billings across periods, that lump distorts the trend. Normalize these to annual billings - only count the current-year portion - unless you are specifically analyzing cash collection efficiency.

Calculated billings formula

When direct invoice data is not readily available - common when pulling metrics from GAAP financial statements rather than a billing system - use the calculated billings formula:

Calculated billings = Revenue + (Ending deferred revenue - Beginning deferred revenue)

Or equivalently:

Calculated billings = Revenue + Change in deferred revenue

Worked example:

This formula works because the change in deferred revenue captures the portion of billings that has not yet been recognized. Add that back to recognized revenue and you recover the full billings figure.

Important caveat: the calculated billings formula is an approximation. It can be distorted by deferred revenue movements that are unrelated to billings in the current period - for example, refunds, credits, or contract modifications that reduce deferred revenue without reducing billings. Use it as a cross-check, not a replacement for direct invoice data. KPMG's handbook on revenue for software and SaaS covers in detail how variable consideration and contract modifications flow through deferred balances under ASC 606.

When historical ledger adjustments make the aggregate numbers unreliable, Aleksandar Stojanovic, CEO & Founder at Fiscallion, emphasizes that rebuilding billings from the contract and invoice level is the only way to separate the true demand signal from the noise. "The practical method is to rebuild billings... pull out refunds and credits into their own line, isolate mid-contract modifications (upgrades and downgrades) from new-business billings, and present new-business billings as the clean demand signal alongside the adjustments shown separately," Stojanovic outlines.

Providing the board with a clear bridge that isolates new and expansion billings from these standard ledger adjustments ensures they are looking at real commercial traction rather than downstream accounting noise.

How to interpret billings movements

Billings are a leading indicator - they signal what is coming into your revenue pipeline before it hits the income statement. But the signal requires interpretation. Billings growth does not always mean what it looks like.

Billings growing faster than revenue: three interpretations

The most common misread at $5M-$50M ARR companies: billings spike in Q4 because the sales team pushed annual plans to hit targets. Recognized revenue stays flat. The deferred revenue balance grows. Finance interprets it as growth momentum. The CEO hires ahead of it. By Q2, the recognized revenue ramp has not appeared, and the hiring cost is real.

The correction: always show billings and recognized revenue on the same chart, with the deferred revenue balance as a third line. That visual tells the actual story.

Billings declining while revenue holds steady: what it signals

If billings drop in a period but recognized revenue is unchanged, your deferred revenue balance is shrinking. That means you are delivering service on contracts that were already invoiced - and new invoicing is not keeping pace.

Watch for:

- A slowdown in new contract signings (pipeline issue)

- A shift from annual to monthly billing terms (customer preference or sales behavior)

- Higher-than-expected churn in the renewal cohort (GRR signal)

A declining deferred revenue balance is not automatically bad - it can reflect normal unwind of a large contract. But paired with flat or declining billings, it is a leading indicator that revenue will follow downward within two to four quarters. Per SaaS Capital's annual retention benchmarks, median gross revenue retention for private B2B SaaS sits at approximately 89-91% — meaning retention erosion that is still "in range" can mask a billings decline that will surface in recognized revenue one to three quarters later.

Billings as a runway input

Because billings are closer to cash than recognized revenue, they matter directly to cash flow planning. A company with strong annual billing - 70%+ of ARR on annual prepaid plans - will see large billings spikes in the months when most contracts renew, followed by extended periods with low billings. Your cash flow forecast needs to reflect that cycle.

The practical question to answer in your model: in which months do you expect billings to exceed your monthly operating costs? That gap funds your operations between billing spikes. If your renewal concentration is high (for example, 60% of ARR renews in Q4), you may carry high cash balances in Q1 and face genuine cash pressure in Q3 - even if your ARR is stable.

What billings tell you that revenue does not

Recognized revenue is a lagging signal. By the time revenue reflects a change in your business - a drop in new logo signings, a shift in retention, or a pricing change - the decision window has already closed.

Billings move earlier in the cycle. A slowdown in billings this quarter will show up in recognized revenue one to four quarters later, depending on your contract lengths. That lag is where the decision value lives.

Three specific decisions billings inform before revenue does:

1. GTM efficiency: If new customer billings are declining as a percentage of total billings, your acquisition engine is softening. Renewals are masking it. You have a quarter or two to diagnose and respond before revenue feels it.

2. Cash planning: A high-billings quarter generates a cash inflow that you will spend over the next 12 months delivering service. Your cash model should map billings timing to deferred revenue unwind to recognize that the cash is not free - it carries an obligation. This is one of the most common gaps in SaaS revenue forecasting: models built on ARR projections without accounting for how billing timing creates lumpy cash inflows.

3. Pricing and contract term decisions: When you evaluate whether to move customers to annual plans, offer multi-year discounts, or shift to usage-based pricing, the first-order effect shows up in billings. Billings modeling is the right tool for evaluating those trade-offs before they hit the income statement.

Billing mix and its effect on reported billings

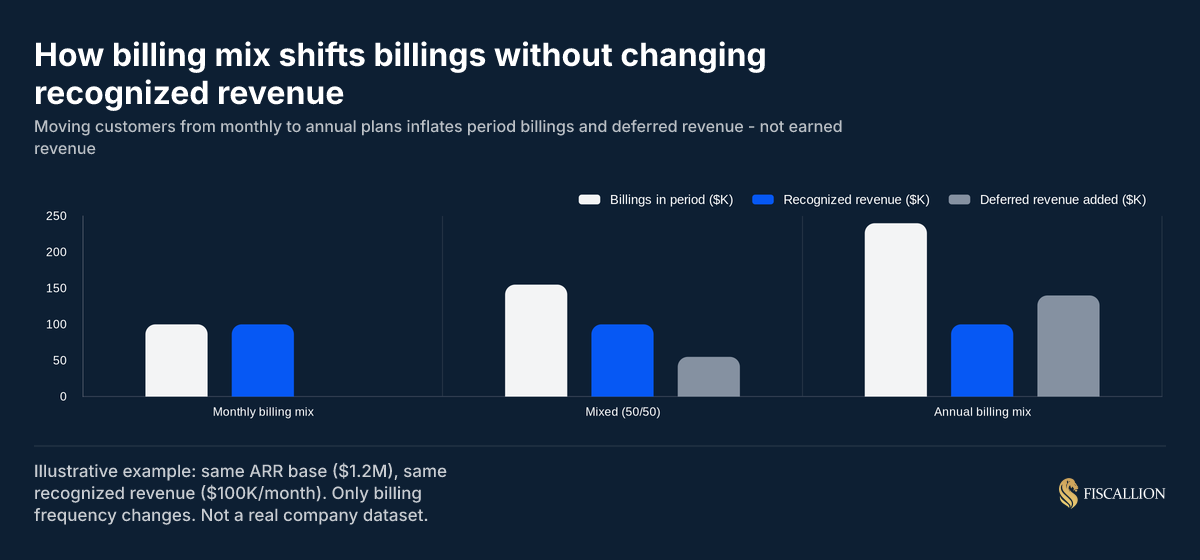

One of the most important and least discussed dynamics in SaaS billings: a company can increase its reported billings significantly without adding a single new customer, simply by shifting its existing base from monthly to annual payment terms.

The chart above makes this concrete. Three companies with identical ARR ($1.2M) and identical recognized revenue ($100K/month) report very different billings depending on their billing mix. The all-annual company bills $240K in a given month; the all-monthly company bills $100K. Same business, same revenue - the billings number diverges by 2.4x.

This has several decision-grade implications:

For fundraising: Public SaaS companies commonly report "calculated billings" as a key growth metric. An investor comparing your billings trend to a public benchmark needs to know your billing mix to make the comparison meaningful. A 30% increase in billings that is entirely attributable to a billing mix shift from monthly to annual is not the same signal as a 30% increase driven by new logo growth. The 2025 KeyBanc Capital Markets & Sapphire Ventures SaaS Survey — the industry's most widely cited private SaaS benchmark — shows ARR growth projected to accelerate from 15% in 2024 to 20% in 2025, but that headline number says nothing about the billing mix driving reported billings at individual companies.

For board reporting: If you shifted 20% of your customer base to annual plans this quarter, your billings will show a spike. Report the cause alongside the number. A board member who sees billings up 35% without the mix context will draw the wrong conclusion about sales momentum.

For your financial model: Billing mix affects working capital. Annual upfront billing generates large, lumpy cash inflows and builds deferred revenue. Monthly billing generates smooth, predictable cash inflows with no deferred revenue buildup. Your cash flow model needs to reflect which regime you are operating in - and what happens if it changes.

Because billing frequency shifts can wildly alter your apparent top-line momentum, your go-to-market incentives must be explicitly designed to prevent artificial metrics manipulation. If your reps can trigger a quarterly cash push just by migrating existing accounts, your true growth trajectory is easily obscured.

The right practice: track billings by billing frequency (monthly vs. annual vs. multi-year) as separate line items. That segmentation is what lets you distinguish demand acceleration from billing policy change.

Types of billings: a reference table

Not all billings are the same, and treating them as a single number obscures what your business is doing.

The most consequential segmentation for decision-making: separate recurring subscription billings from professional services billings. Including professional services in your billings growth figure will inflate the trend during high-onboarding periods and mask a slowdown in subscription ARR growth. Andreessen Horowitz's 16 Startup Metrics makes this point directly — ARR should exclude one-time fees and professional services fees, and the same discipline applies to billings segmentation.

What to do next: five actions ordered by impact

1. Define billings with a single owner (Finance, immediate)

Check whether your billing system, your accounting tool, and your financial model use the same definition. In most $5M-$50M ARR companies, they do not. Assign one person to own the billings definition, the inputs, and the reconciliation to deferred revenue. This takes a day. The clarity it creates is permanent.

2. Reconcile billings to the deferred revenue bridge monthly (Finance, ongoing)

Run the identity check every month close: Calculated billings = Revenue + Change in deferred revenue. If that does not balance, find out why before closing the books. Unreconciled deferred revenue is an audit risk and a model integrity problem.

3. Segment billings by type in your model (Finance + Sales ops, 2-4 weeks)

Build a billings waterfall: new customer, renewal, expansion, professional services, usage. That breakdown is what makes billings a useful management metric rather than a number you report and move on from. Trend each component over at least four quarters.

4. Add billing mix as a tracked variable (Finance, ongoing)

Track what percentage of ARR is on annual vs. monthly vs. multi-year contracts. If that ratio is changing, it will move your billings figure independently of demand. Report the mix alongside the billings trend in board decks and investor updates so the reader can separate signal from billing policy effect.

5. Build a billings-to-cash model for the next 12 months (Finance, 1-2 weeks)

Map your expected billings by month based on contract renewal dates, new logo projections, and anticipated billing mix. Then model the cash receipt timing (accounting for payment terms) and the deferred revenue unwind. That forward view is what gives you real cash flow visibility - not just the current bank balance. For a structured approach to building this, the startup runway calculation guide covers the cash timing mechanics in detail.

Common billings mistakes and the replacement moves

Mistake 1: Treating billings as revenue in top-line reporting

A $120K annual contract invoiced in January frequently shows up as "$120K revenue" in CRM dashboards, when GAAP recognized revenue for that month is actually only $10K.

Replacement move: Reserve the term "revenue" in all external communications, models, and board decks strictly for GAAP-recognized revenue. Report billings separately, label them clearly, and never use them as a top-line revenue proxy.

Mistake 2: Celebrating billings growth that is entirely a billing mix shift

Treating a Q3 billings spike as an operational acceleration signal when it was actually caused by converting existing monthly users to annual prepaid plans.

Replacement move: When reporting any billings increase, explicitly isolate the growth drivers by source: new logo volume, expansion, renewals, or billing mix shift. Only new logos and expansion signal genuine demand growth in the underlying business.

Mistake 3: Using the calculated billings formula without checking deferred revenue accuracy

The formula (Revenue + Change in deferred revenue) relies on your deferred revenue balance being accurate. In many SaaS companies at the $5M-$20M range, deferred revenue is not tracked at the contract level - it is an estimate or a roll-forward from the prior period. An inaccurate deferred revenue balance produces an inaccurate calculated billings figure.

Replacement: Build or verify a contract-level deferred revenue schedule. Each active contract should have: invoice date, billing amount, service start date, service end date, recognized to date, and remaining deferred balance. The sum of those remaining balances should equal your balance-sheet deferred revenue line. The deferred revenue in SaaS guide walks through the exact waterfall structure for tracking this at the contract level.

Mistake 4: Including professional services in billings without flagging it

Implementation, onboarding, and consulting fees are real billings. They are not recurring subscription billings. Including them without segregation inflates the trend during onboarding-heavy periods and understates churn-adjusted ARR growth.

Replacement: Report professional services billings as a separate line. When calculating billings growth rates for investor comparisons or benchmarking, use subscription billings only.

Mistake 5: Ignoring DSO (days sales outstanding) when analyzing billings

Billings are invoices sent. Cash collected follows - but how quickly depends on your payment terms and collections effectiveness. A company with 60-day payment terms and a high billings quarter may not see the cash for two months. If burn rate is high and that cash has been modeled as arriving sooner, the runway math is wrong.

Replacement: Track DSO alongside billings. DSO = (Accounts receivable / Annualized revenue) x 365. If DSO is creeping up while billings hold steady, collections are slowing down. That is a cash flow problem, not a billings problem - but you will not see it unless you track both. The accounts receivable management guide covers DSO benchmarks by customer segment and the collection process that prevents it from drifting. According to a 2024 analysis tracking major SaaS companies, the industry-wide average DSO sits at approximately 54 days - but that average is heavily skewed by large enterprise-focused businesses. If you sell to SMB or mid-market, your target DSO should be materially lower.

Billings and deferred revenue dashboard: a working outline

Most $5M-$50M ARR companies have the raw data for this across Stripe or Chargebee, their accounting system, and their CRM. The gap is a single model where the relationships between these numbers are visible and reconciled.

Every row needs an owner and a consistent definition. The output is only as reliable as the inputs.

Frequently asked questions

Why do billings matter for runway forecasting?

Billings determine when cash arrives. A company with 70% annual billing will collect large upfront payments at contract start or renewal - often in Q4 if its sales cycle follows enterprise budget cycles. Runway is determined by cash timing, not recognized revenue. A billings-based cash model that maps invoices to payment timing to deferred revenue unwind gives a more accurate forward view than a revenue-only model. For how to build that model, the FP&A for startups framework covers the cash timing inputs most forecasts miss.

Is billings the same as ARR?

No. ARR (annual recurring revenue) is a metric derived from the recurring value of active subscriptions, normalized to an annual rate. It is a run-rate measure, not a flow metric. Billings are actual invoices issued in a period - a flow metric. For a monthly subscriber, billings in a period equal one month of contract value. ARR for that subscriber equals their monthly contract value multiplied by 12. They are related but measure different things.

What is a healthy billings growth rate for SaaS?

There is no universal benchmark because billings growth depends on billing mix, contract lengths, and the underlying ARR growth rate. The 2025 KeyBanc Capital Markets & Sapphire Ventures SaaS Survey — now in its 16th year and the most comprehensive private SaaS benchmark — projects ARR growth accelerating from 15% in 2024 to 20% in 2025, with top-quartile performers running meaningfully higher. What matters more than the absolute growth rate is what is driving it - new logo growth, expansion, or billing mix shift - because only the first two reflect demand.

Drive growth by treating billings as an operational metric

Billings measure one specific thing: the invoice your customer received. Not the commitment they made. Not the service you delivered. Not the cash in your account. Each of those is a different number, and mixing them up produces the same error - a top-line figure that looks clean until someone applies it to a decision.

The structural mistake Fiscallion sees repeatedly across $5M-$50M ARR companies is not a definitional gap - most founders understand the distinction in theory. The operational gap is that no one owns the reconciliation. Billings live in the billing tool. Revenue lives in the accounting system. Deferred revenue lives in a spreadsheet maintained by whoever last touched it. Those three sources are rarely verified against each other, and the identity (Billings = Revenue + Change in deferred revenue) is almost never checked monthly.

That reconciliation gap is what causes runway miscalculations, overstated board narratives, and hiring decisions based on cash that was already committed to deliver service.

The fix is mechanical: build the contract-level deferred revenue schedule, run the reconciliation identity monthly, segment billings by type, and assign a single owner to each input. The billings number stops being noise and becomes a leading indicator you can actually act on.

Audit your metrics definitions and forecasting model - and know exactly which inputs are fragile and which assumptions need an owner.