Most founders lose equity to the option pool before they lose it to investors. The mechanism is invisible unless you model it - and most term sheets are written to stay that way.

Getting the startup equity pool right requires three separate decisions: how large to make it, whether it sits pre-money or post-money, and how to manage it as a budget across rounds rather than as a per-grant approval queue. Each decision compounds. A mistake on any one of them - an oversized pool accepted without a hiring plan, a pre-money structure not questioned, a pool used without tracking burn - adds real dilution cost that cannot be recovered.

This article gives you the decision framework for all three.

What you'll learn

- How the option pool shuffle silently transfers founder equity to investors before a round closes

- How to size your pool using a bottoms-up hiring plan instead of accepting benchmark percentages

- How to negotiate pool structure (pre-money vs. post-money) and what it's worth in ownership terms

- How to manage the pool as a budget with a burn rate, reserve target, and refresh cadence

- The five most common pool mistakes at Series A through Series C, and the replacement move for each

What a startup equity pool actually is (and isn't)

An equity pool - formally called an employee stock option pool or ESOP - is a block of shares reserved for future grants to employees, advisors, and key contractors. It sits on your cap table as authorized but unissued shares.

Three things are true of every equity pool that most explanations skip over:

1. The pool is counted in your fully diluted share total immediately. Ungranted options dilute existing shareholders the moment the pool is created, not when options are granted or exercised.

2. The pool comes out of the common shareholder side. This is the core of the option pool shuffle: when a pre-money pool is created or expanded, it dilutes founders and employees - not the incoming investor.

3. Unused options do not automatically revert. At exit, ungranted shares in the pool typically convert and benefit all shareholders proportionally. Founders created the dilution, but investors captured some of the benefit from the shares that were never used.

Who gets equity from the pool (and who doesn't)

The founder/investor distinction matters because it shapes who bears pool dilution. When the pool expands, only common stockholders pay for it under a pre-money structure.

How the option pool shuffle works (with the math)

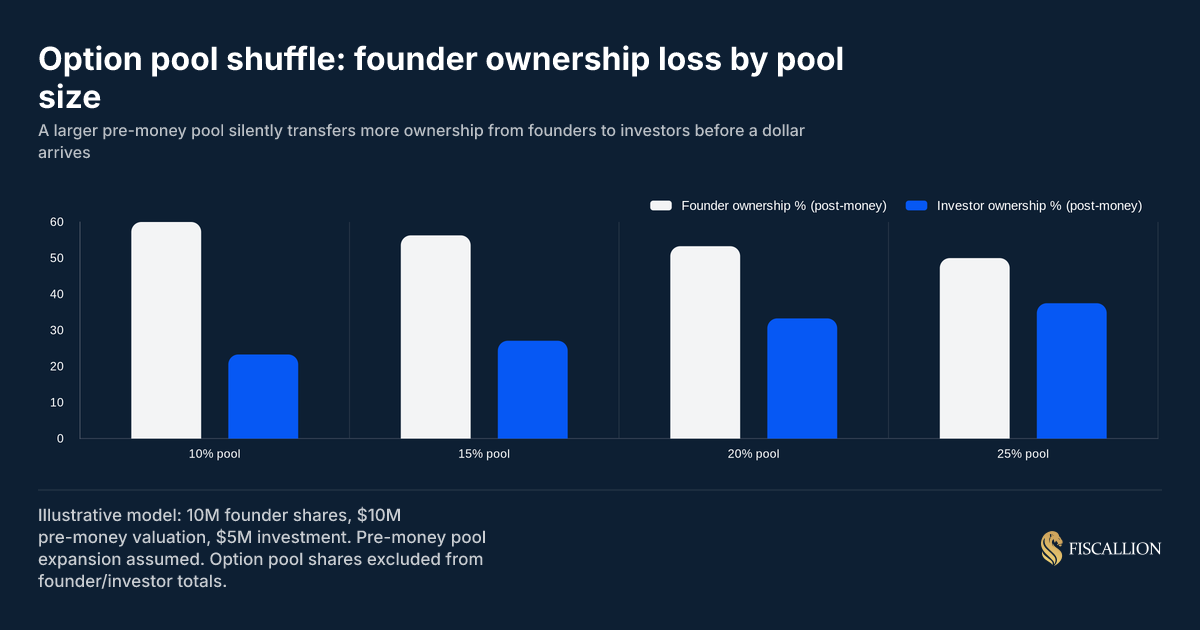

The option pool shuffle - a term coined by Venture Hacks - is the mechanism by which investors require the option pool to be created or expanded inside the pre-money valuation. This means founders absorb that dilution before the investor's capital arrives. Cooley GO's guide to negotiating the option pool puts it plainly: a higher valuation paired with a larger pre-money pool can leave founders with less ownership than a lower valuation with a smaller pool.

Here is the concrete math. Assume 10 million founder shares, a $10 million pre-money valuation, and a $5 million investment.

The headline valuation is identical in all three scenarios. But the founder's effective price per share drops from $1.00 to $0.74 when a 20% pre-money pool is added. The investor's ownership jumps by 5 percentage points - earned not through a lower valuation, but through a structural mechanic that goes unmodeled in most term sheet reviews.

The additional trap: investors routinely request pools that are larger than actual hiring needs. Any ungranted options sit on the cap table as phantom dilution until exit, at which point the cancelled shares benefit all shareholders proportionally - including the investor who pushed for the oversized pool in the first place. Seward & Kissel's analysis of the option pool shuffle frames this precisely: if employees have been appropriately equitized and the expansion is forward-looking, all shareholders - including the new investor - should bear their proportionate share of the dilution.

The post-money structure shifts who bears the cost

A pre-money option pool is a backdoor discount for investors. It forces founders to absorb 100% of the future hiring dilution before a single dollar hits the bank account. Requesting a post-money pool top-up ensures that future dilution is split equitably across everyone on the cap table—which is why understanding the pre-money vs. post-money valuation breakdown is your most critical leverage point before signing.

How to size your equity pool correctly

The single most common mistake is accepting a round-number pool percentage from the investor without building the math that justifies a lower number.

The right size is the equity needed to hire the specific roles on your plan between now and your next funding round - nothing more. Adding a 10-15% buffer for opportunistic hires and promotion refreshes is reasonable. Adding an extra 8 points because "Series A companies usually have a 20% pool" is unnecessary dilution.

Step 1: Build a bottoms-up hiring plan

List every role you plan to hire in the next 12-18 months. Assign an equity grant range to each based on seniority and stage. Add the totals. Cooley GO's option pool negotiation guidance recommends building an option budget based on post-closing percentages - it typically yields a credible pool that is meaningfully lower than the abstract percentage investors assume is standard.

Sum your planned grants. Add 10-15% buffer. That is your pool size request.

Step 2: Account for what is already granted

If you already have an existing pool with outstanding grants, the incremental refresh request should cover only the gap between available ungranted shares and planned future grants.

Example:

- Current pool: 12% of fully diluted shares

- Already granted: 8%

- Available headroom: 4%

- Hiring plan requires: 9%

- Incremental refresh needed: 5% (not 12%)

Investors will often propose a full pool replacement. A well-modeled bottoms-up plan makes it far harder to justify a pool that is twice your documented need.

Step 3: Check top-down benchmarks

Use benchmark data as a sanity check, not a target.

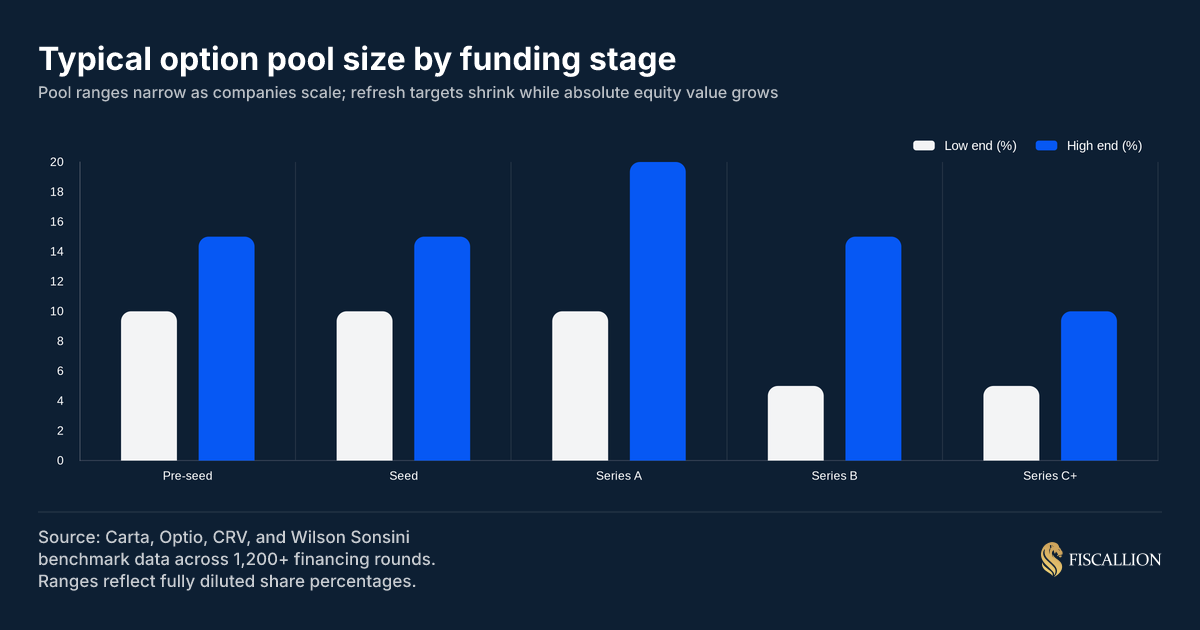

According to Carta's option pool sizing guide - drawn from data across more than 53,000 startups on their cap table platform - the right pool size is almost always a function of your specific hiring plan, not a stage-based benchmark. Their H2 2024 State of Startup Compensation report also shows that average equity packages have stabilized after a 37% decline from peak 2022 levels, meaning the competitive grant environment is less heated than it was two years ago. Series A pools typically land in the 15-20% range, but the right number for your round depends entirely on your specific hiring plan, the seniority of roles, and your geography. US pools tend to run 2-5 percentage points larger than European equivalents at the same stage.

If your bottoms-up plan produces a number significantly lower than the investor's request, that gap is your negotiating leverage - and it is legitimate leverage because it is backed by a documented hiring plan, not a preference.

How pool dilution compounds across rounds

A pool created at seed is not a one-time event. Each subsequent round dilutes the existing pool alongside founder equity. If the pool is topped up at each round on a pre-money basis, the dilution compound effect is significant. This is the same compounding mechanism that makes equity dilution so costly when it goes unmodeled across rounds.

A simplified three-round path illustrates this:

By Series B, the founder's 100% has become roughly 36% - with a meaningful portion of that compression coming from pool mechanics rather than investor economics. The ungranted pool at each stage does not return to founders at refresh; it resets on new terms that typically benefit the incoming round investor.

This is why treating the pool as a multi-round budget is essential. At Fiscallion, we build equity pool modeling directly into the headcount and runway planning framework - not as a separate cap table exercise - because the pool is a capital allocation decision, not an HR administration task.

Managing the pool as a budget between rounds

Most teams track pool grants. Fewer teams track pool burn rate. Almost none of them model pool exhaustion timing the way they model cash runway.

Here is the framework:

Track gross pool burn rate

Gross pool burn = total options granted per quarter / total pool size

This tells you the rate at which you are consuming the pool. If you granted 2% of the pool in a quarter and have 24% remaining, your gross burn suggests roughly 12 quarters - or 3 years - before the pool runs dry. But that math assumes no new hires with larger grants, which is usually wrong.

Track net pool burn rate

Net burn adjusts for forfeited grants from departures. When an employee leaves, unvested options return to the pool. According to Carta's H2 2024 compensation data, combined voluntary and involuntary job departures declined to their lowest levels since mid-2021 - but high turnover companies still see net burn run significantly below gross burn, giving a false picture of available headroom.

Track both. If gross and net burn diverge sharply, you have a retention problem, not a pool management problem.

Set a reserve target by stage

Do not let the pool reach zero before your next raise. Running out of equity before the next round forces a mid-cycle pool expansion with worse terms than a planned top-up at close.

Reserve targets by stage:

- Series A through B: Keep at least 7-8% ungranted heading into the next round conversation

- Series B through C: Keep at least 5-6% ungranted

- Series C onward: Keep at least 3-4% ungranted

These are minimums. If your hiring plan shows the pool reaching 3% in 9 months and your next round is 14 months away, you have a structural problem that needs to be addressed - either through a board-approved interim expansion, aggressive grant reduction, or an accelerated fundraise timeline.

Model refresh grants separately

Retention grants - sometimes called refreshers - are additional grants given to employees who are approaching or past the end of their original vesting period. The industry-standard vesting structure - 4 years with a 1-year cliff, then monthly vesting - means a meaningful cohort of early employees will approach full vest at the same time, creating a predictable retention risk that needs to be budgeted in advance.

A common refresh cadence: annual grants of 25-50% of the original grant, beginning in year 3 of employment. Budget this separately from new hire grants so the pool model stays accurate.

Five common equity pool mistakes (and the replacement move)

Mistake 1: Accepting the investor's pool percentage without a hiring plan

The investor proposes 20%. You accept it because "that's normal for Series A." The result is 5-8 percentage points of unnecessary founder dilution.

Replacement move: Build a 12-18 month bottoms-up hiring plan before the term sheet conversation. Present it as the supporting document for your pool size request. Most investors will not push back against a well-modeled plan. Y Combinator's Series A term sheet guidance is explicit that pool size is a negotiated point - a forward-looking hiring plan is your best argument for keeping it smaller than the investor's opening ask.

Mistake 2: Not modeling the pre-money pool impact on your cap table

The headline valuation looks right, so you stop there. You discover the real ownership picture after the round closes.

Replacement move: Model three scenarios on the cap table - no pool expansion, pre-money pool, and post-money pool - before responding to any term sheet. The effective price per share and your post-close ownership percentage will differ materially across them. Understanding equity dilution mechanics at this level of precision is non-negotiable before signing.

Mistake 3: Not asking for a post-money pool structure

Post-money pools are negotiable. Founders who do not ask do not get them.

Replacement move: Explicitly request a post-money pool structure. Frame it as sharing the dilution equitably across all shareholders. Some investors will decline; many will accept a partial concession - such as a smaller pre-money pool with the remainder created post-money. The NVCA's Model Term Sheet - the most widely referenced standard in US venture financing - treats the pool size and structure as a negotiated field, not a fixed convention.

Mistake 4: Over-granting equity to early advisors and contractors

Advisory equity tends to be granted generously in the first 12-18 months, often without vesting milestones tied to meaningful introductions or outcomes. This depletes the pool faster than planned hires without generating commensurate value.

Replacement move: Cap advisor grants at 0.10-0.25% for early-stage advisors, with a 12-24 month vesting schedule and clear deliverable triggers. Board-approved structures for startup equity compensation should govern all advisor grants, not informal conversations.

Mistake 5: Treating the pool as infinite until it isn't

Teams grant freely through Series A, run the pool to 2-3% available, and then realize they cannot offer competitive grants to the senior hires needed for Series B execution.

Replacement move: Set pool burn rate reporting in your quarterly finance review. Treat available pool headroom the same way you treat runway. If you cannot hire your next VP Engineering without exhausting the pool, that is a board-level capital allocation conversation - not a future problem.

Pre-closing checklist: before you accept any option pool term

Use this before responding to any term sheet that includes an option pool provision.

- Does the term sheet specify pre-money or post-money pool?

- Have I built a bottoms-up 12-18 month hiring plan with roles and grant amounts?

- What percentage does the plan actually require (not what the investor proposes)?

- Have I modeled my ownership % under pre-money vs. post-money pool scenarios?

- What is my effective price per share after the pool expansion?

- Have I explicitly asked for a post-money structure?

- What is my current ungranted pool headroom before the refresh?

- Does the incremental expansion proposed cover the gap - or overshoot it?

- What is the ungranted pool likely to be heading into the next round?

This checklist is not sophisticated finance. It is the minimum rigor required before accepting terms that affect permanent equity ownership. Most founders who lose unnecessary ownership at Series A do so not because they lack leverage but because they did not run the numbers before the conversation.

Understanding how the pool fits into your broader cap table management structure gives you the full picture - pool mechanics, dilution sequencing, and the downstream impact on Series B terms. And when you are modeling startup valuation methods alongside pool scenarios, the interaction between pre-money valuation, pool size, and price per share becomes the most consequential calculation in the term sheet.

The founder’s playbook for equity protection

The startup equity pool is not a benefit program. It is a capital allocation decision with compounding effects across every subsequent round.

The three things worth internalizing before your next financing:

1. Size the pool from a hiring plan, not a benchmark. A documented 12-18 month plan gives you legitimate ground to negotiate the pool size down - which is worth real ownership percentage points.

2. Model the pre-money vs. post-money impact before you respond to any term sheet. The difference is not cosmetic. At a $10M pre-money raise with a 20% pool, founders can lose 5-7 percentage points to the shuffle without the headline valuation changing.

3. Manage pool burn rate the way you manage cash burn. Equity is a finite resource. Running out between rounds forces a mid-cycle expansion on worse terms than a planned top-up at close.

The founders who retain the most equity over a multi-round path are not the ones who negotiated the highest valuation. They are the ones who modeled the dilution mechanics and made the structural asks before the term sheet was signed.

If you are heading into a priced round or Series A and want to model the pool impact on your cap table before the conversation starts, book a working session with Fiscallion. We build the model with you, not after the fact.