Most investor updates are written as a compliance exercise. A metrics table, a list of wins, a vague "we're making progress" narrative, and a delayed send when the month looks bad. Investors recognize the pattern immediately - and it costs more trust than you realize.

The investor update is one of the highest-leverage activities a founder at the $5-50M ARR stage consistently underinvests in. Done well, it shortens your next fundraise, activates your investor network, and builds a longitudinal operating record that proves you can think and communicate like an operator, not just a builder.

Key takeaways

- The MRR Waterfall: Aggregate growth hides whether your business is healthy or leaking.

- Bad News First: Leading with misses builds more trust than burying them in highlights.

- Runway Reality: Calculating runway on gross cash out instead of net burn is a red flag.

- The "Asks" Section: Two specific monthly asks convert passive readers into active help.

- Consistency > Format: A timely, predictable monthly update beats a delayed quarterly deck.

What an investor update actually is - and what it is not

An investor update is a regular email communication from a founder to the full cap table - including angels, seed funds, and non-board VCs - that summarizes operating metrics, key decisions, progress against goals, current constraints, and specific asks for help.

It is not a board update. Board updates are formal presentations in scheduled board meetings with slide decks, financial statements, and structured strategic discussion. Those happen with directors who have governance rights and fiduciary duties.

The investor update reaches the people who are not in the room for board meetings - the angels who wrote your first check, the seed partner who passed on leading Series A but still holds a position, the strategic investor who has a network you want access to. These people know nothing about your trajectory unless you tell them.

This distinction matters for tone and length. A board deck is a working document. An investor update is a communication. It should read in under five minutes, require no attachments, and be structured so an investor scanning it in between meetings can extract the signal.

The update has two jobs:

- Keep your investor network informed well enough to be useful when you need them.

- Build a 12-18 month operating record that investors review before your next round closes.

The second job is what most founders underestimate. Before a Series A or B closes, every firm reviewing the deal will re-read the last year of updates. They are not just checking the numbers - they are checking whether your narrative held up, whether you called problems early or buried them, and whether the person who sent those updates is the person they want to compound with. NFX's research on founder-investor dynamics confirms this directly: the updates sent during difficult periods are the ones investors remember most when deciding whether to re-engage.

The cadence that matches your stage

Monthly is the default from seed through Series A. The founders who skip during hard months train investors to expect silence when things are difficult - exactly when consistent communication matters most.

The rule: if you have investors, you send monthly updates. A missed month because "things are complicated" is a missed month where investor confidence erodes quietly.

The six-section structure that works

There is no mandatory format, but there is a structure that consistently produces the right outcomes: investors stay informed, the asks section generates action, and the longitudinal record serves the next raise. Here is what it looks like.

Section 1: The one-sentence summary

Write this last. It should capture the state of the business in 30 words.

"We closed [Month] at $[X] ARR ([+X%] MoM), with [X] net new customers, [the most important event - positive or negative], and our primary focus for the next 30 days is [specific initiative]."

This sentence determines whether the investor reads the rest carefully or skims. If the business had a bad month, say so here. Investors who scan the opening and find only good news before discovering a problem three paragraphs down lose more trust than the problem itself would have cost.

Section 2: The metrics table

This is the core of every update. Keep the format identical every month. Investors read these comparatively - a metric that disappears without explanation raises a flag.

Minimum table at any stage:

The MRR waterfall is not optional. Aggregate MRR growth hides whether your business is healthy or structurally leaking. A business adding $80K new MRR while churning $75K is not growing - it is a leaking bucket. As ChartMogul's SaaS retention research across 2,100+ businesses found, contraction MRR alone can represent up to 40% of all MRR lost - a drag that is completely invisible if you only track the net line. Investors will calculate net new MRR from the ARR change themselves, and they will wonder why you did not show your work.

Section 3: What happened and why

Two to three sentences describing the main operating event of the month. Not a list of activities - a narrative about what actually drove the numbers.

- What was the main thing that happened?

- What caused it?

- What does it mean for next month?

Founders over-engineer this section. They list every initiative, every meeting, every feature shipped. Investors do not need a complete log. They need the signal. Three sentences that answer those three questions are more useful than twelve bullets that do not.

Section 4: What is not working (do not skip this)

This is where trust is built or destroyed.

State the current biggest constraint or miss. Be specific - not "sales is slower than expected" but "our average sales cycle for deals above $25K ACV extended to 67 days in [Month], up from 43 days in [Prior Month]. We believe the cause is [X] and we are addressing it by [Y]."

Founders who include this section consistently build a track record of operational honesty. Founders who omit it when things are hard teach investors that the updates are marketing, not information.

Experienced investors are not surprised by hard months. They are surprised by founders who hide them.

Section 5: Focus for next month

One to three bullets describing what will define success in the next 30 days. Specific enough that the investor can check progress against it at the start of next month's update.

Not: "grow faster."

Instead: "Close [Company A] and [Company B] currently in final negotiation" or "hit 85% activation rate for [Month] cohort before the 30-day mark."

This section creates accountability across update cycles. When your next update references these goals - hit or missed - investors see that you track what you say, not just what happened. Over twelve months, that pattern builds a credibility asset that compounds at the next raise.

Section 6: Asks

The most underused section in almost every investor update.

Investors have networks, pattern-matching across portfolios, and specific functional expertise. A concrete ask converts a passive reader into an active helper. Limit to two or three per update - more than that and none get acted on.

Effective ask format:

- "A warm introduction to a VP of Operations at a 200-500 person SaaS company using Salesforce, evaluating workflow automation in Q3." (Named profile, specific use case.)

- "We are evaluating two employment lawyers for an option pool restructure. Would appreciate a referral if you have worked with someone reliable for this."

- "Hiring a Head of Revenue Operations. If you know someone coming off a similar role at $20-50M ARR SaaS, I'd appreciate the connection."

Vague asks generate nothing. "Any introductions to potential customers" generates nothing. A named profile with a specific context generates introductions.

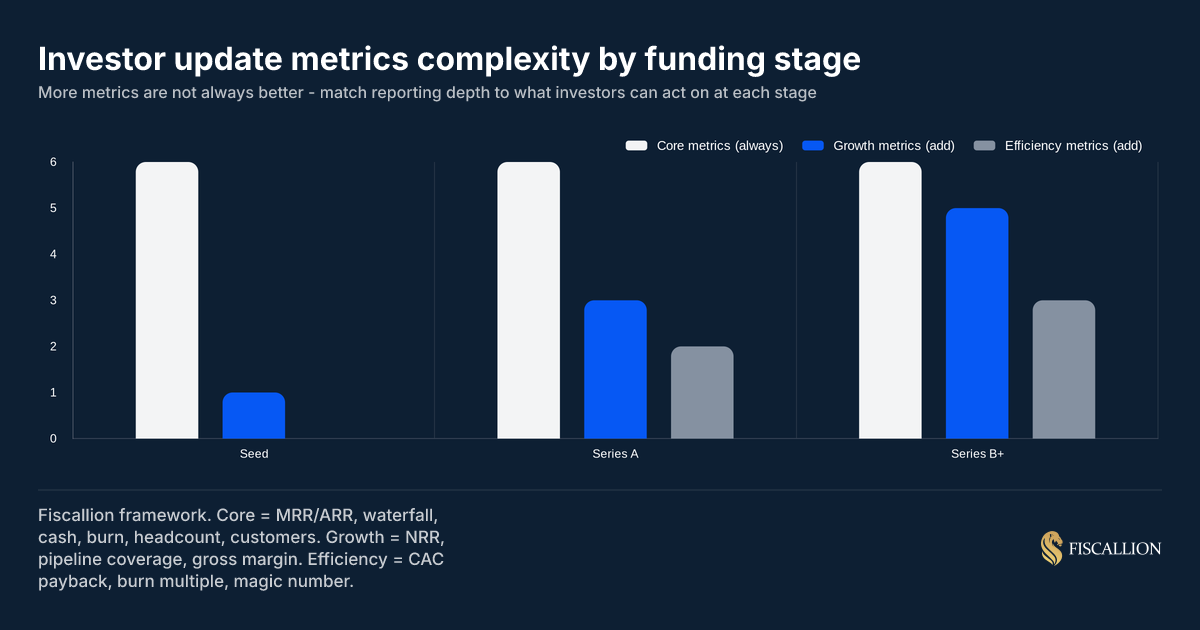

Which metrics belong at each stage

Not every metric belongs in every update. Reporting the same five metrics from pre-seed to Series B makes the update look like it was built for a smaller business. Add metrics as the business adds the complexity they reflect.

Core metrics: always present

These belong in every update from seed forward:

Add at Series A

These metrics become relevant when you have enough history to show trends and enough investors asking about capital efficiency:

NRR deserves specific attention. SaaS Capital's annual benchmarking research shows that NRR benchmarks vary significantly by ACV - higher ACV products with longer sales cycles and dedicated account management show structurally higher NRR than SMB-focused products. Knowing which cohort you belong to is required context before your NRR number means anything to a Series A investor. For a deeper breakdown of what these benchmarks mean at your specific ARR stage, our net revenue retention benchmark guide for SaaS companies walks through the numbers by ACV tier and pricing model.

On CAC payback: the trend direction across quarters matters more than any single quarter's number. If payback is extending while ACV stays flat, that is an acquisition efficiency signal worth explaining - not hiding. Our CAC payback period guide for SaaS covers how to calculate it correctly and the benchmarks by segment that apply.

Add at Series B+

The burn multiple warrants a note. David Sacks, who introduced the metric at Craft Ventures, defines it as net burn divided by net new ARR - a direct measure of how much cash you are spending to generate each dollar of new recurring revenue. A burn multiple above 2x at Series B signals that growth is expensive relative to the capital deployed. Below 1x is exceptional. Most Series B investors will benchmark your number against this framework whether you include it or not.

The principle is not comprehensiveness - it is that each metric you add should reflect a genuine operational reality the investor can act on. Adding NRR before you have 12 months of cohort history produces a number without context. Adding burn multiple before Series A creates noise in an update that should be signal-dense.

At Fiscallion, when we build investor reporting infrastructure for $5-50M ARR companies, the most common problem is not that founders report too few metrics - it is that they pull numbers from three different systems manually each month, the definitions drift between updates, and the resulting table looks precise but is not. Consistent metrics require consistent data infrastructure, and that is a prerequisite to consistent communication.

How to handle a bad month without losing credibility

The instinct when a month goes sideways is to delay ("I'll send it when we have better news") or to minimize ("growth was slower than expected due to market conditions"). Both are mistakes. Both cost more trust than the underlying miss.

The structure for a difficult update

When results were genuinely bad, change the structure slightly. Lead with the headline directly:

- State the result without softening. "We missed our MRR target by $18K. New business came in at $31K against a $49K plan."

- Give the specific root cause - not a systemic excuse. "Three enterprise deals forecast to close slipped to [Next Month] due to procurement delays. One SMB deal churned six weeks in after the primary champion left."

- Describe what you are doing about it - concrete and time-bound. "We added a procurement checklist to all deals above $20K ACV to identify multi-stakeholder dependencies earlier. We restructured SMB onboarding to ensure activation before the 30-day champion review."

- State what you are not changing. "We are not changing our ICP or pricing. The enterprise opportunity is intact - this was execution lag, not a product-market fit signal."

Handling this transparency correctly comes down to a fine line between operational control and chaos. When delivering bad news, your primary goal is to show that while you didn't escape the problem, you fully understand it.

Investors who receive this kind of update during a bad month come away more confident in the founder, not less. The ones who receive a vague, delayed, or positive-framed update when they can see from the numbers that something went wrong are the ones who start asking for more frequent check-ins and begin treating the founder as a risk factor in the deal.

The test is simple: would you rather have an investor find out about the problem from your update, or from the delta between this month's ARR and last month's?

The mistakes that quietly undermine trust

Changing the metrics you report

If ARR growth slows and the next update features a new engagement metric instead, investors notice. They interpret it as a founder who changed the scorecard because the original scorecard was unflattering.

Replacement move: Report the same core metrics every month. If you genuinely believe a metric no longer represents the business, say so explicitly - name the replacement, explain why, and include both for a transition period.

Experienced growth investors review past updates to see if your transparency holds up under pressure. The moment a founder swaps a hard financial metric for a soft engagement number, investors recognize the pattern immediately.

Sending updates only when things are good

Investors recognize the pattern. Monthly updates during strong growth, silence during flat or declining periods - the absence becomes its own signal. A missed month communicates "things are bad and I don't want to tell you." An on-time update during a hard month communicates "I am on top of this."

Replacement move: Set a fixed send date (e.g., the first Tuesday of the following month) and treat it as a hard deadline regardless of what the numbers show.

Calculating runway on gross burn

Runway should always be calculated on net burn: cash out minus revenue in. Reporting "24 months of runway" based on gross burn overstates your position. When investors model your runway against current revenue, the discrepancy signals either financial misunderstanding or deliberate inflation of the number.

As a16z's framework for navigating down markets makes clear, raising capital with less than 12 months of runway sends a negative signal and weakens your negotiating position - making runway visibility a fundraising input, not just an operational metric.

Replacement move: Define runway explicitly in the update. "We have $3.2M in cash, net burn of $280K/month, equaling 11.4 months of runway at current rate." Remove any ambiguity about which figure you used. Our startup runway calculation guide covers the common calculation mistakes and how to present the number in a way investors can immediately trust.

Reporting gross MRR without churn

A business adding $80K new MRR while churning $75K is not growing. Reporting only new MRR or gross ARR without the churn component is either a calculation mistake or a deliberate omission. Investors will calculate net new MRR themselves from the ARR delta. For the full breakdown of why each waterfall component matters - and how expansion MRR in particular compounds differently from new logo growth - see our expansion MRR guide.

Replacement move: Always show the waterfall. New + expansion - contraction - churn = net new MRR. Show your work.

Writing updates only your internal team could parse

Jargon-heavy updates with internal shorthand ("NorthStar-v2 activated for cohort 7B") tell investors nothing about business health. The update should be written for someone who is not in your weekly team meeting.

Replacement move: Write the update as if the reader knows the business structure but not the internal terminology. Every acronym and internal name needs a one-phrase definition the first time it appears.

Burying the asks or omitting them entirely

The most common structural failure in investor updates. Founders summarize the month, then add a vague note at the end ("let us know if you can help!"). Nothing gets acted on.

Replacement move: Treat the asks section as a product decision. What are the two highest-value actions an investor could take in the next 48 hours? Make those the asks. Be specific enough that an investor can respond with a name or a yes/no.

A copy-ready investor update template

Use this as a starting point. Adapt the metrics table to your stage. Remove the annotations before sending. The goal is an update that reads in under five minutes and requires no attachments.

Subject: [Company Name] - [Month Year] Update

Opening sentence:

We closed [Month] at $[X] ARR ([+X%] MoM), with [X] net new customers, [one key event - good or bad], and our focus this month is [specific initiative].

BY THE NUMBERS - [MONTH YEAR]

WHAT HAPPENED

[2-3 sentences: the main operating event of the month, what caused it, and what it means for next month. Not a list of activities.]

WHAT IS NOT WORKING

[1-2 sentences: the current biggest constraint or miss. Be specific. State the metric, the magnitude, the probable cause, and the response.]

NEXT MONTH

- [Goal 1: specific and checkable next month]

- [Goal 2: specific and checkable next month]

- [Goal 3: optional, only if genuinely high priority]

ASKS

- [Specific warm introduction with named profile and use case]

- [Specific referral, knowledge request, or tactical help]

The investor update is not difficult to write well. It is difficult to write consistently - especially during the months when the numbers make you want to delay it. That is exactly the discipline that separates founders who close their next round faster from those who re-explain a 14-month silence before a term sheet.

What makes investor updates harder than they look: the data problem

The structural difficulty of consistent investor updates is not the writing. It is the data.

At the $5-25M ARR stage, MRR lives in Stripe or Chargebee. Pipeline lives in HubSpot or Salesforce. Cash and burn live in QuickBooks or Xero. Customer count lives in your CRM. Headcount lives in a spreadsheet someone updates when they remember to. Assembling these numbers manually at month-end takes two to four hours and introduces definition drift - the same metric calculated slightly differently from month to month.

When the definition drifts, the longitudinal record breaks. An investor comparing this month's MRR to six months ago is comparing different calculations - and they will eventually notice. This is the same fragmentation problem we cover in our SaaS revenue forecasting framework - the systems disagree, the billing source is correct, and the model built on the wrong input produces the wrong decisions.

The fix is not hiring a full-time analyst to build a monthly pack. It is building the data infrastructure that connects these systems with consistent definitions, so the metrics table is a 20-minute write, not a four-hour assembly. That is what Fiscallion's KPI dashboard and reporting service is built to deliver: a single source of truth across your billing, CRM, and financial systems so your investor update reflects what actually happened, defined the same way every month.

That kind of consistency is what makes the longitudinal record credible - and the longitudinal record is the asset that closes faster.

Your investor update is an operating record, not a newsletter

The investor update is a decision-grade communication tool, not a compliance obligation.

Done well - on time, consistently structured, with the MRR waterfall, a diagnosed lowlight, and two specific asks - it builds investor relationships that pay off in introductions, warm follow-on interest, and a faster close on your next round. Done poorly, or not at all, it trains investors to discount whatever they hear from you next.

The template in this guide is a starting point. The only version that matters is the one you send, on time, every month, regardless of what the numbers look like.

If you want the data infrastructure that makes consistent investor reporting sustainable - without assembling four spreadsheets every month-end - book a working session with the Fiscallion team. We will audit your current metrics definitions, identify where definition drift is happening across systems, and build the reporting layer that makes monthly updates a 20-minute exercise, not a four-hour one.