The gap between the dollar amount raised on a SAFE and its fully diluted impact on your cap table causes more Series A surprises than almost any other early-stage decision. The instrument is simple. The consequences compound quietly until the priced round forces a reconciliation

This guide covers SAFE notes from the ground up: what the instrument actually is, how it calculates at conversion, the difference between pre-money and post-money structures, what happens when the company doesn't make it, and the questions you need to answer before issuing one. By the end, you'll have enough clarity to negotiate terms, model the dilution, and present the structure honestly to your board.

Key takeaways

- A SAFE (Simple Agreement for Future Equity) is not a loan. It converts to equity at a future priced round, acquisition, or liquidity event, with no interest accruing and no maturity date.

- The valuation cap and discount rate are the two mechanisms that determine how much equity an investor receives at conversion. Modeling these before you sign matters more than negotiating the headline check size.

- Post-money SAFEs are now the market standard (87% of rounds in 2024 per Carta). They give investors ownership certainty but concentrate dilution directly on the founding team.

- If the company fails before conversion, SAFE holders typically sit behind all creditors and preferred shareholders - meaning they often recover nothing.

What a SAFE note actually is

A SAFE - Simple Agreement for Future Equity - is a contractual right for an investor to receive equity in your company at a later date, triggered by a specific event. The investor writes a check today. No shares change hands. No interest accrues. There's no maturity date forcing repayment.

The conversion happens when a triggering event occurs. The most common triggers are:

- A priced equity round (typically a Series A or later)

- An acquisition of the company

- A dissolution or wind-down

Y Combinator created the SAFE in 2013 as a faster, simpler alternative to convertible notes for early-stage deals. It stripped out the loan mechanics — maturity dates, interest rates, default provisions — and left just the equity conversion right. That simplicity is what drove adoption. In 2018, YC updated its standard SAFE templates to the post-money format, anchoring the market shift that followed.

By Q1 2025, SAFEs accounted for a record 90% of all pre-seed rounds on the Carta platform. At that stage of the market, it has become the default instrument for angel and seed fundraising.

The SEC's Common Startup Securities resource provides a plain-language overview of where SAFEs sit in the broader financing landscape — useful context before signing your first one.

SAFE vs. convertible note: the structural difference

A convertible note is a loan. It carries an interest rate (typically 5–8% annually), a maturity date (often 18–24 months), and if no qualifying round occurs before maturity, the company technically owes that principal back to the investor. That creates pressure that SAFE notes do not.

The absence of a maturity date makes SAFEs simpler to manage. But it also means the conversion timeline is entirely dependent on whether the company raises a priced round. A convertible note forces a resolution. A SAFE can sit on your cap table indefinitely - which is fine when everything goes to plan, and complicated when it doesn't.

The two terms that control your dilution

There are two mechanisms inside a SAFE that determine how much equity the investor receives when the note converts. Both need to be modeled before you sign.

Valuation cap

The valuation cap is a ceiling on the price at which the SAFE converts. It protects the investor from losing the benefit of their early risk if the company's valuation rises significantly between the SAFE issuance and the priced round.

Example: An investor puts in $500,000 on a SAFE with a $6M valuation cap. Your Series A prices the company at $20M pre-money. The SAFE converts as if the company were valued at $6M - giving the investor significantly more shares per dollar than the Series A investors.

If there were no cap, the investor would simply convert at the Series A price, receiving the same share price as a new investor who took no early risk. The cap is the financial compensation for taking that risk.

Discount rate

The discount rate gives SAFE investors a percentage reduction on the share price paid by investors in the triggering round. A 20% discount means the SAFE investor pays $0.80 for every $1.00 the new round investors pay.

When a SAFE includes both a cap and a discount, the investor converts using whichever mechanism produces a lower share price - whichever is more favorable to them.

Conversion price formula

For a SAFE with a valuation cap, the conversion price is:

Conversion price = Valuation cap ÷ Company capitalization at conversion

For a SAFE with a discount only:

Conversion price = Priced round share price × (1 - discount rate)

The conversion price determines how many shares the investor receives:

Shares issued = SAFE investment amount ÷ Conversion price

The lower the conversion price, the more shares the investor receives per dollar invested - and the more your ownership dilutes. YC's official post-money SAFE primer walks through the full conversion math with worked examples worth reviewing alongside this.

Pre-money vs. post-money: why this decision matters more than the cap

Most founders spend their negotiation energy on the valuation cap number. The pre-money vs. post-money question gets less attention, but it controls how dilution is distributed when multiple SAFEs convert in the same round.

Pre-money SAFE

With a pre-money SAFE, the conversion calculation is based on the company's capitalization before any SAFE investments are included. This means all SAFE investors in the round dilute each other, as well as the founders. The investor's final ownership percentage is unknown until the priced round closes.

The upside for founders: dilution from multiple SAFEs is spread across all parties, not concentrated solely on the founding team.

The downside: investors dislike the uncertainty, which is why pre-money SAFEs have become significantly less common.

Post-money SAFE

With a post-money SAFE, the investor's ownership is fixed as a percentage of the post-money valuation cap - and that ownership stake is known immediately, not at future conversion.

Each new SAFE issued under a post-money structure does not dilute existing SAFE investors. It dilutes the founders. Every check you add to the round directly reduces your stake.

Relying on the headline percentage of a post-money instrument masks the true compounding impact that sequential fundraising runs have on common equity. Because early positions are fixed, every subsequent check scales up the effective dilution rate born exclusively by the core founding team.

The math is clear: At a $10M post-money valuation cap, a $500,000 SAFE locks in 5% ownership for that investor. A second $500,000 SAFE locks in another 5%. Together, they've claimed 10% of your company before your Series A closes.

The market has moved firmly to post-money

As of Q3 2024, 87% of all SAFEs on the Carta platform were post-money structures - up from 43% at the start of the decade. YC's update of its standard templates to the post-money format anchored this shift.

The implication for founders is direct: you can't fight the post-money standard. What you can do is negotiate the valuation cap carefully, model each check's dilution impact before accepting it, and track cumulative SAFE obligations as a liability on your cap table from day one.

What you're actually giving up at conversion

The clean way to think about SAFE dilution is to model your pro forma cap table before you raise the priced round - not after.

Here is a worked example with a single post-money SAFE converting into a Series A:

Setup:

- Founders own 10,000,000 shares

- SAFE investor A: $500,000 at $10M post-money cap (= 5% ownership locked in)

- SAFE investor B: $500,000 at $10M post-money cap (= 5% ownership locked in)

- Series A: $3M investment at $15M pre-money valuation

- New option pool: 2,000,000 shares created at Series A

Post-Series A cap table:

The founders entered the process at 100% and exit the Series A close at roughly 60%. The option pool expansion at Series A is often where founders are surprised - the new pool typically comes out of founder shares, not investor shares, making the effective dilution steeper than the SAFE terms alone suggest.

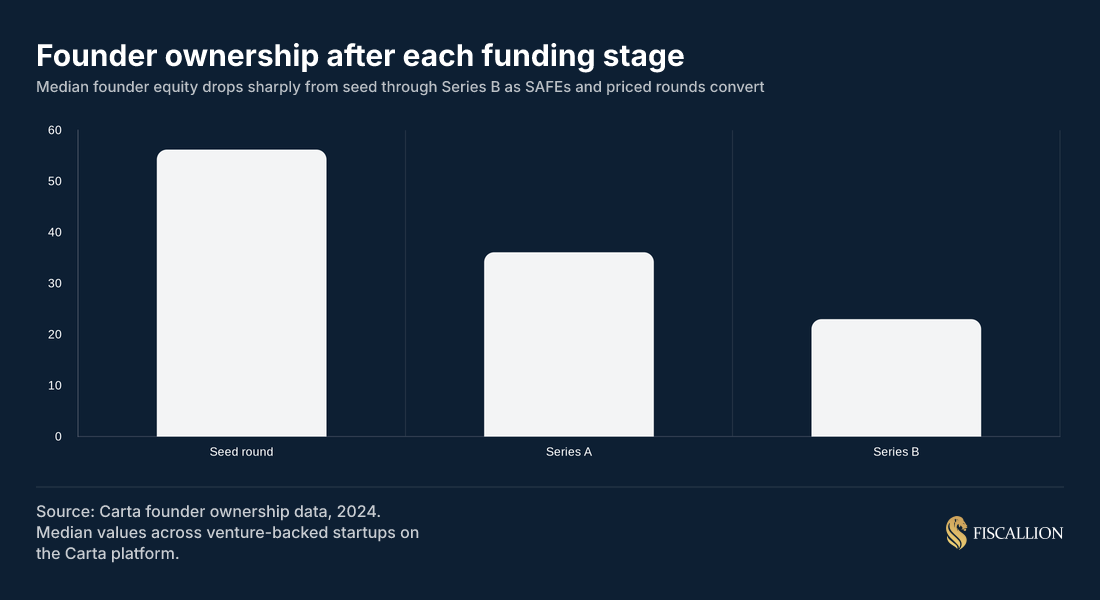

Industry data from Carta's Founder Ownership Report reinforces how compounding this is across rounds:

At seed, the median founding team holds 56.2% of the company. By Series A, that's 36.1%. By Series B, it's 23%. The slope of that decline is shaped heavily by how SAFEs were structured and how many were issued.

This compounding effect — SAFE dilution stacking on top of option pool expansion stacking on top of new round dilution — is why equity dilution in startups deserves a standalone model, separate from whatever cap table tool your lawyer uses. Understanding the mechanics of each dilution event in sequence is the difference between a cap table that surprises you at Series A and one you walk in having already presented.

When to use a SAFE note

SAFEs work well in specific situations. They're not the right tool for every raise.

Use a SAFE when:

- You're at pre-seed or seed stage and a priced round would require negotiating a valuation you can't support yet with data

- Speed matters - SAFEs close faster than priced rounds and require significantly less legal overhead

- You're running a rolling close with multiple angel investors, where opening and closing a priced round for each check isn't practical

- You want to defer governance negotiations (board seats, information rights, protective provisions) to the priced round

Don't use a SAFE when:

- You're within weeks of a priced round - it's cleaner to bring investors directly into that round

- Your investor base expects debt protections that a SAFE doesn't provide

- Your cap table already carries multiple SAFEs at different caps - adding more increases conversion complexity and can surprise new Series A lead investors

- The amount being raised is large enough to warrant a priced round on its own

TechCrunch's reporting on what makes a cap table uninvestable is worth reading here — the patterns that kill Series A conversations almost always trace back to SAFE issuance decisions made without modeling the downstream impact.

One practical note: SAFEs don't grant voting rights, board seats, or information rights at issuance. That doesn't mean investors won't ask for them separately. Make sure any side letters or information rights agreements are documented - undocumented side arrangements create the same cap table complications as poorly structured SAFE terms.

What happens to a SAFE note if the startup fails

SAFE notes are not debt. That distinction matters most when the company doesn't make it.

In a bankruptcy or dissolution scenario:

- Secured creditors (banks, lenders) are paid first

- Unsecured creditors (vendors, employees owed wages) are paid next

- Preferred stockholders receive their liquidation preferences

- Common stockholders receive whatever remains

- SAFE holders - because the SAFE never converted to equity - are treated as unsecured equity claimants with no preference

In most startup failure scenarios, there are insufficient assets to cover secured creditors, let alone reach SAFE holders. The practical outcome is that SAFE investors typically recover nothing in a wind-down. The SEC's investor bulletin on SAFE note risks is explicit on this point: SAFE investors may be last in line and receive nothing if the company fails.

This is the investor's fundamental risk when signing a SAFE at the pre-seed or seed stage. They are not protected by debt covenants or liquidation preferences the way preferred shareholders in a priced round would be. The valuation cap and discount rate are the upside reward for taking that exposure - but if the company fails before conversion, neither term provides any protection.

For founders, the implications are:

- You have no personal obligation to repay SAFE investors - unlike a loan, there is no personal guarantee (absent fraud or specific contractual terms)

- The SAFE liability disappears with the entity in a proper dissolution - it does not follow you as an individual

- Multiple open SAFEs at dissolution create legal complexity - consult counsel before dissolving a company with unconverted SAFEs outstanding to ensure proper investor notification and process

In an acquisition scenario before conversion:

If the company is acquired before a priced round triggers SAFE conversion, SAFEs typically convert immediately before close - or the acquisition agreement specifies a cash settlement. Whether the investor profits depends on the acquisition price relative to the SAFE's valuation cap. At a high acquisition price, cap holders benefit significantly. At a low-price or distressed acquisition, they may receive cents on the dollar - or nothing if proceeds are absorbed by creditors.

The 4 Ps of due diligence as it relates to SAFE-backed companies

When investors conduct due diligence on a SAFE-stage company, the framework most diligence professionals apply is the 4 Ps: People, Philosophy, Process, and Performance.

People: Who is leading the company and what is their track record? At the SAFE stage, this is often the dominant criterion because there is limited financial history. Investors assess founder quality, domain expertise, and team composition as proxies for execution probability.

Philosophy: What is the investment thesis underlying the business? Does the market opportunity make sense given the product approach? Is the company's view of how value is created coherent and defensible?

Process: How does the team make decisions? Is there evidence of disciplined product development, structured GTM motion, or repeatable revenue generation? For SaaS founders raising on a SAFE, this is increasingly relevant even at seed - investors want to see a model, not just a deck.

Performance: What early evidence exists that the approach is working? Conversion rates, early MRR, net revenue retention in pilot cohorts, engagement data. At the SAFE stage this is necessarily limited - but what exists needs to be credible.

Note that Performance is the fourth criterion, not the first. Most experienced diligence professionals hold the view that if the first three Ps are in place, performance data tends to follow. The risk of focusing your SAFE fundraising narrative too narrowly on early numbers is that it distracts from the people-and-philosophy thesis that actually moves decisions at this stage.

For founders preparing to raise on a SAFE and anticipating diligence, the practical preparation work mirrors what you'd do for a full institutional raise. A clean cap table, organized corporate documents, clear financial model assumptions, and documented unit economics position you to move quickly when diligence starts. This connects directly to the kind of financial organization work outlined in Fiscallion's due diligence checklist for startups.

The 50-100-500 rule and when SAFEs stop being appropriate

The 50-100-500 rule is a maturity framework popularized by technology analyst Alex Wilhelm. It identifies three thresholds at which a company has generally moved beyond the early startup phase:

- $50M in annual revenue - indicating a validated, economically viable business model

- 100 or more employees - indicating the organization has grown past informal coordination and requires structured management

- $500M in company valuation - indicating meaningful investor confidence in scale potential

The rule is a heuristic, not a definition. But it's relevant to SAFE note use for a specific reason: SAFEs are designed for early-stage companies that cannot yet support a priced round. Once you've approached or crossed any one of these thresholds, the instrument and its associated informality are no longer fit for purpose.

At $15–20M ARR with a financing history of multiple unconverted SAFEs, the cap table complexity, investor relations obligations, and financial reporting expectations from sophisticated investors require priced equity - not another rolling SAFE close.

For SaaS founders in the $5–50M ARR range, the 50-100-500 framework is less a celebration milestone and more a signal that financial infrastructure needs to scale in parallel. SAFE-era cap table informality does not survive contact with institutional investors running proper diligence. If your revenue or team is approaching any of these thresholds and you still have unconverted SAFEs outstanding, model the conversion math now. Don't wait for the Series A data room to reveal the surprise.

Common mistakes founders make with SAFE notes

These are the five common SAFE mistakes and how to avoid them.

Issuing multiple SAFEs at different caps without modeling aggregate dilution

Each SAFE issued at a different cap creates a different conversion price at the priced round. Founders often calculate dilution for each note in isolation. The actual dilution is cumulative and compounds in ways that aren't obvious until the cap table is modeled in full.

The replacement move: Build a pro forma conversion model before closing each SAFE. Show the post-conversion cap table at a range of Series A valuations: conservative ($8M pre-money), base ($15M pre-money), and optimistic ($25M pre-money). Know your ownership under each scenario before you sign.

Treating individual seed checks as separate, self-contained instruments frequently blindsides founding teams once an institutional round forces an aggregate equity reconciliation. Without a live conversion model running multiple pricing scenarios, cumulative dilution math can quietly erode the executive team's equity stake before formal negotiations even begin.

Treating the "simple" in SAFE as meaning consequence-free

The SAFE is simple as a document. It is not simple in its financial consequences. Founders sometimes treat SAFE fundraising as informal or low-stakes precisely because the paperwork is light.

The replacement move: Run every SAFE issuance through your cap table model, regardless of check size. A $100K check at a $4M cap on a post-money SAFE is not immaterial.

Not disclosing the full SAFE stack to Series A investors early

Incoming institutional investors will request a full cap table as part of diligence. If they discover unconverted SAFEs they weren't aware of during term sheet negotiations, it creates friction and erodes trust. TechCrunch's analysis of seed-stage fundraising expectations notes that transparency on the SAFE stack is now effectively a baseline expectation from Series A leads.

The replacement move: Include a SAFE conversion schedule in your investor materials from the first conversation. Show the fully diluted cap table post-conversion under your target raise assumptions. Transparency here is not a risk - it's a credibility signal.

Confusing the valuation cap with a priced valuation

A $10M SAFE valuation cap is not the same as a $10M valuation. It is the maximum conversion price. If your Series A prices at $8M pre-money - below the cap - the SAFE converts at that $8M price, which is actually more dilutive to you than if you'd priced at $15M.

The replacement move: Stop using the cap number in your investor conversations as a stand-in for your company's value. Use your cap for what it is: a conversion ceiling, not a valuation anchor.

Issuing a SAFE when a priced round is weeks away

Issuing a SAFE when you're close to a priced round creates an instrument that converts almost immediately, adding legal complexity and investor coordination overhead without the benefits of a longer-runway SAFE.

The replacement move: If a priced round is within 60 days, bring late-arriving investors directly into that round rather than issuing a separate SAFE.

SAFE note checklist before you sign

The SAFE is a light document with compounding consequences. Most problems trace back to decisions made without running the conversion math first. Use this checklist before signing or issuing any SAFE, not after.

For founders:

- Is this pre-money or post-money? (It should be post-money at current market standards)

- What is the valuation cap, and how does it compare to your current fair market value?

- What is the total SAFE stack? List all existing SAFEs, caps, and amounts

- Have you run a pro forma cap table at three Series A price scenarios?

- Does the option pool expansion happen before or after SAFE conversion? (It matters - the standard structure is "pre-money" for the option pool, which increases effective dilution)

- Are there any side letters granting information rights, pro-rata rights, or MFN provisions?

- Have you shared the full SAFE stack with your existing investors and board?

For the SAFE terms themselves:

- Is the triggering event clearly defined? (Minimum financing threshold, event-specific conversion terms)

- Does the SAFE include a most-favored-nation (MFN) clause? If yes, understand its mechanics before issuing lower-cap SAFEs to later investors

- Is there a pro-rata right granting investors the right to participate in future rounds?

- Does the SAFE specify what happens at dissolution vs. acquisition vs. priced round?

A SAFE is one of the lighter documents in the startup financing stack. That lightness is a feature - until it creates a gap in your financial model. Run the math first. The 20 minutes it takes to model conversion scenarios will surface more decision-relevant information than any amount of negotiation over the headline cap number.

You can download the YC standard SAFE documents directly to review the operative terms before engaging counsel.

What comes next after the SAFE stage

Once you've issued SAFEs and started building toward a priced round, your finance infrastructure needs to grow in parallel. The cap table alone isn't the issue - the connected problems are runway visibility, a coherent three-statement model, and a board reporting structure that can hold the SAFE-to-equity conversion story clearly.

That transition - from SAFE-era informality to institutional-grade financial operations - is exactly where most Series A-bound founders feel the gap. The solution isn't hiring a full-time CFO the moment you close. It's building the model and the decision cadence before you need it, so the Series A process doesn't expose you.

Understanding your startup runway calculation alongside your SAFE obligations is the minimum viable financial picture for a company approaching its first priced round. And if you're thinking about the structural modeling underneath all of it - the P&L, balance sheet, and cash flow linkages - Fiscallion's three-statement model guide for startups covers the build from the ground up.

If your SAFE stack is growing and you want to pressure-test the conversion math before your next board conversation, book a working session with Fiscallion.

Model conversion first - the rest follows

A SAFE note is a clean instrument when you use it deliberately. It lets you raise capital before you can support a priced round, defers valuation negotiation to a point where you have more data, and closes faster than almost any other structure.

The problems aren't in the document - they're in the gaps between the document and the decisions around it. Founders who treat SAFEs as a funding shortcut without modeling the conversion impact, fail to disclose the full stack to incoming investors, or don't track cumulative dilution obligations are setting up surprises at Series A.

The three decisions that matter most:

- Model before you sign. Run the post-conversion cap table at three valuation scenarios before closing each SAFE.

- Disclose the full stack early. Every investor in your priced round should know the full SAFE picture from the first conversation.

- Know what the instrument does when things go wrong. SAFE holders sit at the bottom of the capital structure in a wind-down. Issue responsibly, to investors who understand that exposure.

The "simple" in SAFE describes the paperwork. It doesn't describe the consequences.