Pro rata rights are the single term that VC investors report being least willing to negotiate away. Not liquidation preferences. Not board seats. Not anti-dilution provisions. Pro rata. According to a Stanford GSB survey of venture investors ranking twelve contractual terms by negotiating flexibility, pro rata rights came out at the bottom - meaning investors are least flexible on this one.

If you are raising a Series A, B, or C, you will grant these rights. The question is how broadly, to whom, and under what conditions. Getting that wrong creates a cap table problem that compounds every subsequent round.

What pro rata rights actually mean

Pro rata rights - sometimes called participation rights or preemptive rights - give an existing investor the right, but not the obligation, to invest in a future financing round in an amount sufficient to maintain their current ownership percentage.

The right does not guarantee a discounted price. It guarantees an allocation. The investor pays the same price per share as any new investor in the round.

Three things this is not:

- It is not a guarantee that the company will offer a new round

- It is not a right to increase ownership beyond the current stake (that is "super pro rata," covered below)

- It is not automatic - investors must actively exercise the right within the notice window or it lapses

These rights are typically documented in a company's Investors' Rights Agreement (IRA) or a side letter. The NVCA Model Investors' Rights Agreement serves as the industry-standard template that most VC-backed companies and their counsel work from. In seed rounds using Y Combinator SAFEs, pro rata rights are absent by default - which is why most institutional seed investors negotiate a separate side letter specifically to capture them.

The formula - and a worked example

The math is straightforward:

Pro rata allocation = current ownership % × new round size

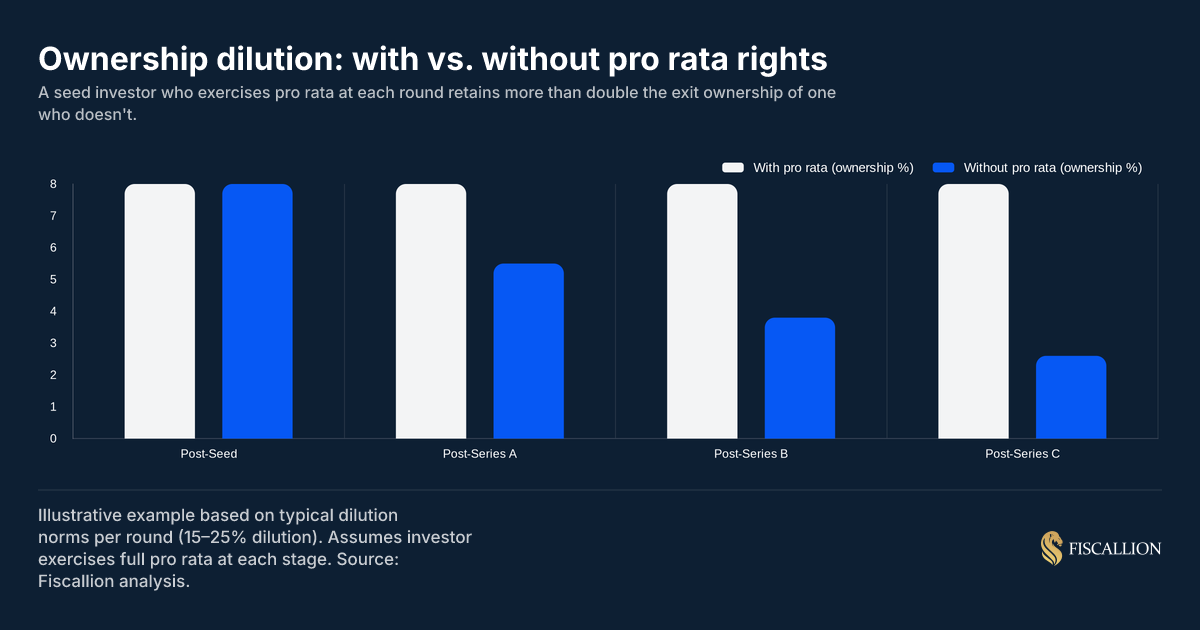

Example: An investor owns 8% of your company after leading your seed round at a $5M post-money valuation. You are raising a $20M Series A.

- Pro rata allocation = 8% × $20M = $1.6M

If the investor exercises this right in full, they invest $1.6M at the Series A price and their ownership stays at approximately 8% post-round (before accounting for the new option pool expansion, which will dilute everyone proportionally).

If they do not exercise, and no one else absorbs that $1.6M gap, the new Series A lead takes a larger slice and your seed investor's 8% drifts down - typically to around 5.5–6% depending on the round's dilution structure.

That drift compounds. An investor who skips pro rata at Series A and Series B can find their 8% seed stake at 2.5–3% by the time the company reaches Series C. The chart below shows exactly how that plays out over multiple rounds.

The founder implication: that dilution does not come from nowhere. When your existing investor exercises pro rata, they are consuming allocation that would otherwise go to new investors. A $20M Series A where three existing investors exercise their full pro rata leaves the new lead with a smaller slice of the round - which affects their willingness to lead at all. For a deeper look at how dilution stacks across rounds - including SAFE conversion and option pool expansion mechanics - see our equity dilution guide for startups.

Major vs. minor pro rata: what the market looks like now

Not every investor gets these rights. The market has developed a clear distinction between major and minor investor pro rata, and the threshold has shifted meaningfully since 2022.

Based on standard NVCA term sheet language and 2024-2025 Cooley/Gunderson deal data.

The post-2022 correction made founders more willing to push back on minor investor pro rata. Counsel now routinely frames this as a cap table hygiene issue: 25 angels each with contractual pro rata rights creates significant administrative friction every round - tracking notice periods, managing waivers, and documenting opt-ins. The negotiation clock slows. Lead investors notice.

The practical outcome: limit formal pro rata rights to major investors only. Define "major investor" explicitly in your IRA with a dollar threshold (typically $250K-$500K seed, $1M+ Series A) or an ownership percentage (typically 1-5%). Anyone below the threshold gets a side letter with softer language or a courtesy allocation - not a contractual right.

Telling an early supporter they won't receive contractual pro rata can feel deeply uncomfortable. However, managing this isn't about shutting them out; it's about framing the decision around institutional constraints rather than personal preference.

What happens to your cap table when investors exercise

Pro rata does not change the size of the round or the total number of new shares issued. It changes who owns them.

Consider a Series B: Your company is raising $15M. You have two existing investors: Investor A (Series A lead, owns 22%) and Investor B (seed, owns 7%). Combined they have pro rata rights on $4.35M of the round.

If both exercise in full, the incoming Series B lead is negotiating for access to only $10.65M of a $15M round. Some institutional funds require a minimum ownership stake of 15-20% to justify leading. At $10.65M, depending on your pre-money valuation, they may not be able to get there.

That is the real cost of broad pro rata rights for founders: reduced competitive tension and a narrower shortlist of potential leads who can write a meaningful check. This is one of several structural constraints that your cap table management framework should model before you open a raise - not after you receive a term sheet.

The counter-argument: when your Series A lead exercises pro rata enthusiastically into your Series B, it sends a powerful signal to incoming investors. The people who know your company best - who sit on the board, see monthly financials, and have visibility into your metrics - chose to put more money in. That endorsement is meaningful, particularly in a fundraising market where outside investors have limited diligence time.

Why investors treat pro rata as non-negotiable: the power law argument

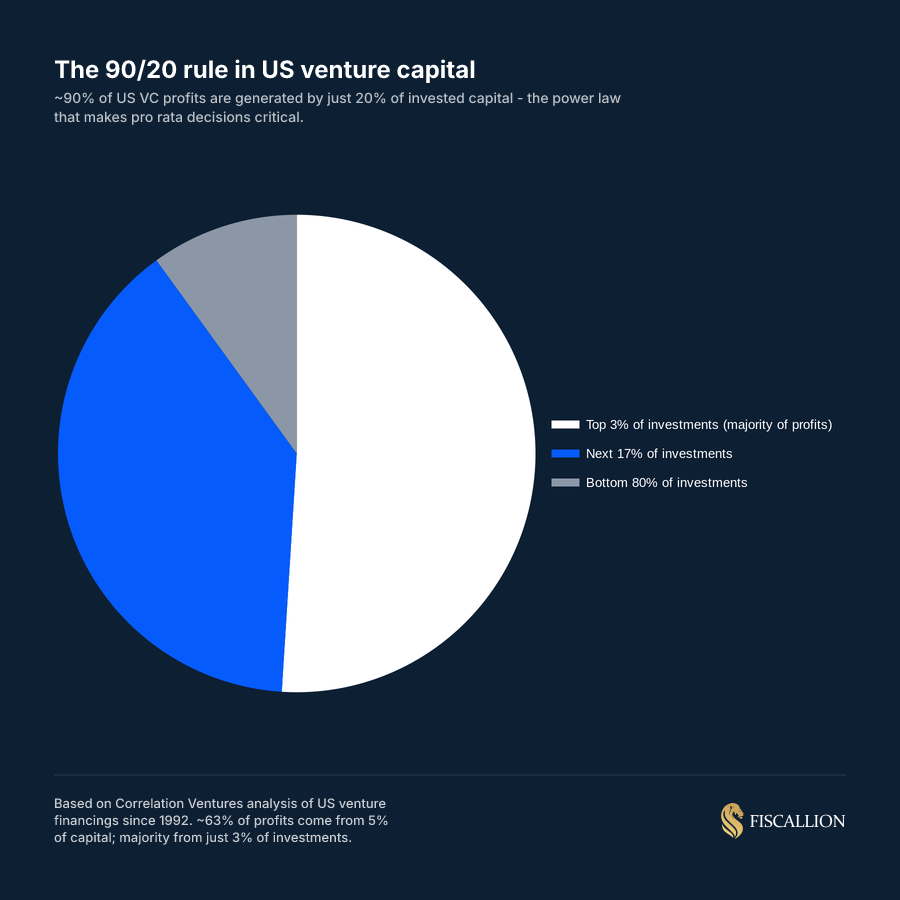

The reason investors fight so hard for pro rata rights comes down to one structural reality about venture capital: returns follow a power law. A small number of investments generate an outsized share of all returns.

Correlation Ventures analyzed US venture financings since the early 1990s and found that approximately 90% of industry profits have been generated by roughly 20% of invested capital - what they call the "90/20 rule." The concentration is even more extreme at the extremes: 63% of profits come from just 5% of invested capital, and a majority of profits come from just 3% of investments.

This distribution is the reason pro rata exists. An investor who correctly identifies one of the top 3% at the seed stage earns far less without pro rata than with it - because every subsequent round dilutes their stake before the exit crystallizes the return.

The math is stark. A seed fund investing $500K for 8% of a company that exits at $500M:

- Without pro rata (diluted to 3% by exit): Return = $15M. MOIC = 30x

- With pro rata exercised at each round ($3M total deployed, maintains 8%): Return = $40M. MOIC = ~13x on deployed but ~80x on initial check

Note the paradox: the MOIC on total deployed capital is lower when you exercise pro rata, but the absolute dollar return is nearly 3x higher. That is why fund-level returns - measured in absolute dollars returned to LPs - depend heavily on pro rata. The investor who maintains ownership in the winner generates a significantly larger check at exit, even if the return multiple on incremental capital is modest.

This is also why Stanford GSB's Ilya Strebulaev reports that investors in VC surveys cite pro rata as the single least negotiable term. Not because the financial theory is airtight (pricing might be fair each round, which theoretically removes the excess return), but because the control and signaling arguments compound the financial math in ways that make exercising feel mandatory.

What the Buffett 70/30 rule means - and what it has to do with this

The 70/30 rule is sometimes referenced in VC contexts but it originates in a completely different framework. Buffett's 1957 letter to investment partners described allocating roughly 70% of capital to "general issues" - undervalued stocks selected on fundamentals - and 30% to "corporate work-outs," meaning special situations like mergers, liquidations, or tender offers where returns depend on a specific event rather than market appreciation.

Over time this morphed in popular discussion into a simpler framing: 70% equities, 30% bonds for balanced portfolio construction. In his 2013 shareholder letter, Buffett described a different split for his wife's trust: 90% S&P 500 index fund, 10% short-term US Treasuries - reflecting his view that long-term equity exposure beats most sophisticated allocation strategies for most investors.

Neither version maps directly to venture capital portfolio construction. But the underlying logic - that you should concentrate resources in your highest-conviction positions and use a reserve allocation for stability or opportunistic deployment - does translate to how a fund thinks about follow-on reserves.

The practical VC parallel: a seed or early-stage fund that deploys capital at 70-80% into initial investments and retains 20-30% for pro rata follow-ons is applying a version of Buffett's reserve logic. The reserve is not speculative - it is held specifically to exercise pro rata rights in the portfolio companies most likely to generate returns.

The 80/20 rule in VC: what it actually means

The 80/20 rule in venture is typically invoked as a portfolio construction heuristic: 80% of a fund's returns will come from 20% of its investments. But as the Correlation Ventures data above shows, the real ratio is closer to 90/20 or even more extreme.

For fund managers, this has a direct implication for reserve allocation. If you know in advance that 2-3 companies out of a 20-company portfolio will account for the majority of your returns, your optimal strategy is to:

- Identify the winners early (easier said than done)

- Maintain or increase ownership in those companies through pro rata

- Not spend time or follow-on capital propping up the bottom half

The 80/20 framing also affects how founders should think about which investors matter most. An investor who owns 5% and consistently exercises pro rata in your up rounds is demonstrating conviction - which affects how future investors read the cap table. An investor who owns 5%, has pro rata rights, but consistently waives them is sending the opposite signal.

AngelList's data on seed investor follow-on behavior points to a nuanced conclusion on the exercise strategy itself: always following on produces higher average (mean) returns, but never following on produces higher typical (median) returns. The difference comes from variance - exercising pro rata concentrates more capital in a smaller number of outcomes, which produces bigger wins when right and worse results when wrong. This is consistent with the power law: more concentration, more skew.

Super pro rata rights: what they are and why you should push back

Super pro rata rights give an investor the option to increase their ownership stake in a future round - not just maintain it.

The structure comes in two forms:

- Residual rights: If any other investor declines to exercise their pro rata, the super pro rata holder can absorb the unused allocation

- Increase rights: The investor negotiates the explicit right to buy up to a defined higher percentage (e.g., increase from 25% to 30%)

Super pro rata is powerful for whoever holds it and a problem for everyone else. The incoming lead investor at your Series B may have a minimum ownership requirement of 15-20% to justify leading. If a super pro rata holder absorbs 30% of the round, the incoming lead may not be able to hit their threshold - and they walk.

The founder's position here is clear: push back hard. Super pro rata is appropriate only for exceptional investors with demonstrated value beyond capital, and even then it should be capped. A contractual right to increase ownership on every subsequent round is a structural impediment to future fundraising.

According to Aleksandar Stojanovic, CEO & Founder at Fiscallion, founders shouldn't view an aggressive opening ask as set in stone, noting that "super pro rata forever and uncapped" is rarely the only acceptable structure. "The compromises I've seen work: a cap, where the super pro rata is limited to a defined percentage of the future round... or a sunset, where the super pro rata right expires after a defined period or a defined number of rounds," Stojanovic shares. For example, a middle ground that successfully closed a highly competitive round involved capping the super pro rata to a locked percentage of the immediate next round, which then sunsetted and converted entirely back to standard pro rata thereafter.

Pro rata rights for founders: what they mean on your side of the table

Founders rarely think about pro rata rights from their own perspective. They are typically thought of as an investor protection mechanism. But there is a legitimate founder-side framing.

As a founder, your equity stake dilutes with each round regardless of pro rata. But the composition of your cap table - who holds what percentage - has real governance consequences. Pro rata rights affect that composition in two ways:

- Existing investors who exercise maintain their voting weight, board influence, and rights tied to ownership thresholds (information rights, protective provisions). This is generally neutral to positive if you want those investors active.

- Passive investors who don't exercise dilute away and eventually fall below the thresholds that give them governance rights. This can simplify your cap table over time.

The strategic question for founders: who do you want to remain meaningful stakeholders as you scale? Grant full pro rata to those investors. Use waiver provisions or below-threshold exclusions to let others dilute.

At the same time, pro rata rights granted today will constrain your options in future rounds. Three practical moves to preserve flexibility:

1. Set a major investor threshold explicitly. Define it in the IRA as a dollar amount or ownership percentage. Investors below the threshold get no contractual pro rata right. Do this at seed before you have too many investors to negotiate with.

2. Negotiate time or round limitations. Pro rata rights can expire after a set number of rounds (e.g., "through Series B") or after a certain date. This prevents a seed angel's pro rata from following you to Series D.

3. Include waiver mechanics. A majority-in-interest waiver allows the company to waive pro rata rights for a specific round with approval from investors collectively holding a majority of the shares subject to pro rata. This gives you a mechanism to clear the board when you need to bring in a specific new lead.

When pro rata rights get complicated: SPVs, transferability, and side letters

A growing number of seed investors - particularly emerging fund managers and solo GPs - negotiate for transferable pro rata rights. This allows them to syndicate their follow-on allocation to LPs via a special purpose vehicle (SPV) rather than deploying from their fund.

The structure: the seed fund has $3M in pro rata rights for your Series B but only $1M of dry powder. They raise a $3M SPV from their LP base specifically to exercise the full allocation. The cap table sees one new line item (the SPV entity) rather than multiple individual LPs.

Founders are often receptive because SPV follow-ons do not consume the fund's limited reserves and the cap table remains relatively clean. The complications:

- Transferable pro rata requires founder consent, typically specified in the IRA

- Institutional Series A or B leads sometimes push back on SPVs in their round, preferring a clean cap table without additional voice votes

- SPV mechanics add legal and administrative cost at each round

The practical guidance: allow SPV mechanics for transferable pro rata for verified major investors who have demonstrated value. Restrict it to affiliates only for minor investors, and exclude it entirely for angel checks under $100K.

The NVCA model Investors' Rights Agreement serves as the standard reference point for how these provisions are typically structured and where waivers can be introduced. If your legal counsel is not working from NVCA-aligned documents, ask why.

Common mistakes founders make with pro rata - and the corrections

Mistake: Granting pro rata to every investor in a seed round, regardless of check size.

The correction: Set a major investor threshold from day one. $100K angel checks with contractual pro rata rights become a cap table management burden by Series B. Define "major investor" as $250K+ at seed and make it explicit in the IRA. Courtesy allocations are appropriate for smaller checks - contractual rights are not.

Mistake: Ignoring pro rata overhang when modeling your Series A raise.

The correction: Before your next round, model how much of the round your existing investors could consume if they all exercise. If the answer is 40%+, you need to either negotiate waivers in advance or design the round size to accommodate both exercise and a meaningful new lead allocation. Build this into your fundraising model, not your post-term-sheet diligence. Your cap table management process should surface this number at least six months before you open a raise.

Mistake: Treating pro rata as a binary - either grant it fully or not at all.

The correction: Pro rata rights have several adjustable dimensions: threshold for eligibility, scope of securities covered, time or round limitations, and waiver mechanics. You can grant robust pro rata rights to your lead investor while including sunset provisions that limit rights for smaller investors after Series B. Negotiate each investor's rights separately in side letters when the IRA allows flexibility.

Mistake: Assuming that waiving pro rata rights signals confidence.

The correction: When an existing investor waives their pro rata in a follow-on round, the market interprets it as a negative signal. It raises the question: does this insider know something we don't? If your lead investor is waiving pro rata at Series B, incoming investors will ask. Have a clear and credible explanation if this happens - fund deployment constraints, portfolio concentration limits, or a deliberate reserve strategy are acceptable. Radio silence is not.

Mistake: Granting super pro rata rights to get the deal done quickly.

The correction: Super pro rata is a long-tail liability. It costs you nothing at seed but constrains your ability to bring in competitive leads at Series B and C. If an investor is demanding super pro rata as a deal condition, negotiate hard. If they will not move, model the impact on future rounds before accepting. Understanding how these terms interact with liquidation preferences and other protective provisions is precisely what our term sheet guide for startups walks through. The short-term deal convenience rarely justifies the long-term structural cost.

A practical checklist for founders negotiating pro rata terms

Before you sign any term sheet that includes pro rata provisions, run through this checklist:

- Have you defined "major investor" with a specific dollar or ownership threshold in the IRA?

- Have you included time or round limitations on pro rata rights for minor investors?

- Have you modeled how much of your next round existing investors could consume if all exercise?

- Do you have a majority-in-interest waiver mechanism for future rounds?

- Have you restricted super pro rata rights or excluded them entirely?

- If transferability is granted, is it limited to affiliates or SPVs with founder consent?

- Do you know which investors add genuine value beyond capital - and have their rights been structured accordingly?

This checklist does not replace legal counsel. But it frames the decisions you need to make before entering a negotiation where the other side has done this many times before.

If your cap table is already complex - multiple seed investors with broad pro rata rights, side letters without uniform language, or super pro rata provisions buried in an older IRA - the time to audit that is well before your next raise. A cap table review six months out is a manageable exercise. The same review three weeks before a term sheet creates avoidable friction in a process where every delay costs momentum.

Build long-term ownership through pro rata architecture

Pro rata rights sit at the intersection of ownership mechanics, power law math, and negotiating dynamics. They are simple in structure - maintain your stake by buying your share of new issuances - and complex in their compounding effects on cap tables, fundraising flexibility, and investor signaling.

For founders, the decisions you make on pro rata at seed and Series A lock in structural conditions that play out over four to six years of subsequent fundraising. The mistakes are predictable: granting broad rights to everyone, ignoring overhang when modeling raises, accepting super pro rata to close a deal faster, and skipping the audit until it becomes urgent.

The framework is straightforward: set a clear major investor threshold, build time and round limitations into the IRA, model the overhang before every raise, and treat pro rata as a tool for curating the investor composition of your cap table - not as a standard boilerplate concession.

If your current cap table has pro rata provisions you haven't fully mapped against your next round's dynamics, that is the right place to start. A working session to audit your metrics definitions, cap table structure, and fundraising model is exactly the kind of decision-grade clarity that prevents a term sheet surprise from becoming a board problem.

Book a working session with Fiscallion to map your cap table pro rata exposure and model the impact on your next round.