Your books closing on day 14 of the new month is not a bookkeeping problem. It is a decision-latency problem. Every day between month-end and the moment you have accurate financials is a day you are running headcount, pricing, and capital allocation decisions on stale data.

The financial close process gets treated as an accounting task at most scaling startups. It is not. It is the operating mechanism that converts a month of activity into the numbers you use to manage the business, answer your board, and decide whether to hire, raise, or slow spend.

This article lays out how to build a financial close process that is fast, GAAP-accurate, and decision-ready - without requiring a full finance team to run it.

Key takeaways

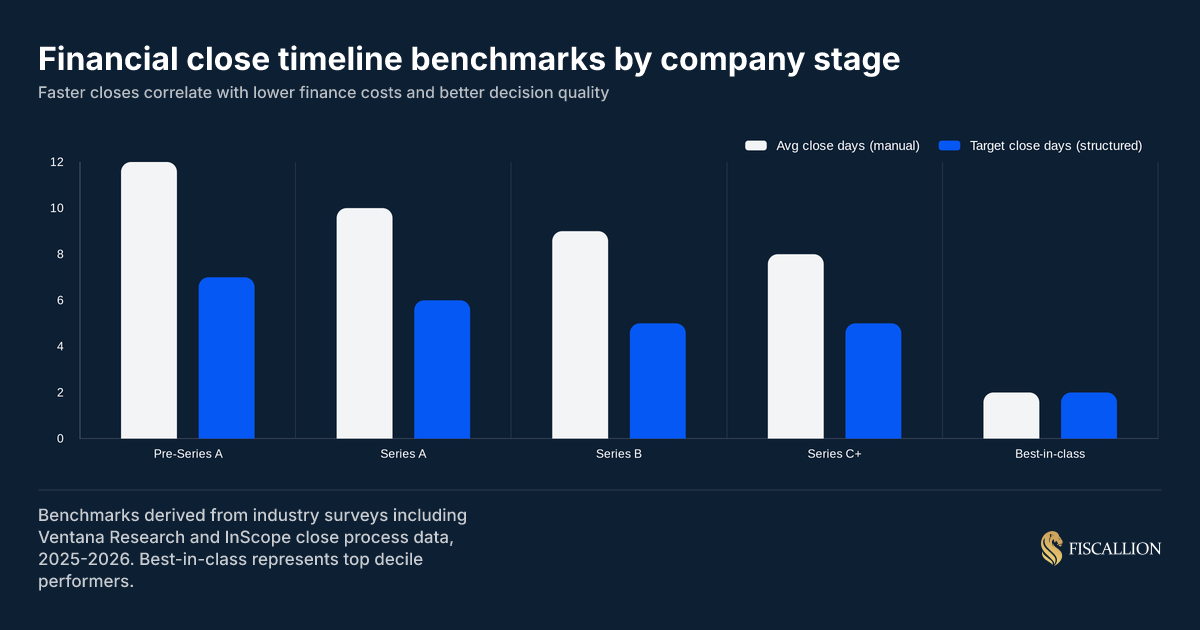

- A 5-to-7 business day close is achievable at most SaaS companies between $5M and $50M ARR. Companies still closing in 10+ days are paying a decision-latency cost they are not measuring.

- The close is not done when the P&L is produced. It is done when the balance sheet is supported, accruals are posted, deferred revenue reconciles, and a variance narrative is ready for leadership.

- Most close delays are sequencing failures, not capacity failures. The fix is workflow design, not headcount.

What the financial close process actually is

The financial close process is the sequence of steps that finalizes a company's financial activity for a given period and produces accurate, auditable financial statements.

At minimum, a completed close delivers:

- A finalized income statement (P&L)

- A supported balance sheet with reconciled accounts

- A cash flow statement or cash reporting package

- Supporting schedules for deferred revenue, prepaids, accrued expenses, and equity activity

- A variance narrative comparing actuals to budget or forecast

The word "finalized" is doing important work here. A P&L is not finalized if revenue recognition has not been applied correctly. A balance sheet is not supported if accruals were estimated and never substantiated. Numbers that are produced but not supported are not close outputs - they are drafts.

A slow close is a proxy for weak financial controls

If your books take more than 10 business days to close, the cause is almost always one of three things: unclear task ownership, a disconnected tech stack, or a revenue recognition process that depends on manual spreadsheets.

Each of those three causes has a fix. None of them require a new CFO hire.

Why close delays cost more than you are accounting for

The cost of a slow close is rarely calculated explicitly. It should be.

Stale numbers produce stale decisions. If your management team is reviewing financials on day 12 of the new month, every decision made in weeks one and two - hiring approvals, vendor commitments, pricing changes - happened without verified data from the prior period. That is not a small gap.

Board and investor reporting gets compressed. If your board meets on day 15 and your close finishes on day 12, your finance lead has three days to produce a board package, write variance commentary, and run scenario analysis. That timeline produces reporting that describes what happened, not what it means or what to do next.

Forecasts start from the wrong baseline. Every rolling forecast is anchored to the most recent actuals. If those actuals are late, every downstream projection inherits that lag. Runway estimates, hiring models, and customer-level economics all degrade when the input data is two weeks old.

The finance function stays reactive. A finance team that spends weeks 1 and 2 of each month closing last month cannot spend that time on forward-looking analysis. At $5M-$50M ARR, your fractional or early finance hire should be building models and stress-testing assumptions - not reconciling bank feeds on day 11.

According to Ledge's 2025 month-end close benchmarks, 50% of finance teams take six or more business days to close - and 27% still exceed seven days regularly. The same research found cash reconciliation alone consumes 20-50 hours per month at most organizations. That is not a staffing problem. It is a sequencing and system problem.

The three phases of a structured close

A well-designed close does not start on the first business day of the new month. It starts during the prior month. Breaking the work into three phases - pre-close, close execution, and post-close - removes most of the day-one pressure that causes close delays.

Phase 1: Pre-close (business days -3 to 0)

Pre-close is the work you do before the month ends. Most of it is continuity work, not month-end work.

- Reconcile bank accounts through at least day 25. Do not wait until month-end to reconcile the current month's transactions.

- Lock prior billing periods in your billing platform once you confirm transactions are complete.

- Run a pre-close trial balance to catch anomalies before the formal close starts.

- Validate CRM-to-billing alignment. Confirm that closed-won deals, renewals, upgrades, and churn events are reflected in your billing system before the month ends.

- Communicate the close calendar to any department head whose expense submissions affect the close - engineering, marketing, sales.

Pre-close is where you compress the formal close timeline. Every hour of work done before day 1 is two hours saved during the formal close.

Phase 2: Close execution (business days 1 to 5)

This is the formal close sequence. Five business days is achievable for most SaaS companies at $5M-$50M ARR if pre-close work is consistent.

If your current close is running 10+ days, the first fix is not automation - it is sequencing. Map what is happening on each day, find the bottlenecks, and identify work that can move to pre-close or run in parallel.

Phase 3: Post-close (business days 6 to 10)

Post-close is where the financial close process becomes a decision input rather than just an accounting output.

- Deliver the board or leadership reporting package with variance commentary.

- Review aging schedules: AR aging, AP aging, DSO trends.

- Update the rolling forecast with actual inputs.

- Document close improvements for the next cycle - what was late, what was unclear, what took longer than expected.

Post-close is also where Fiscallion's work with founders usually has the highest leverage. The numbers are clean. The question is what they mean and what to do next. That translation - from actuals to trade-offs to decisions - is where most lean finance teams stall.

SaaS-specific close requirements that generic checklists miss

A generic accounting checklist does not account for the complexity that comes with subscription revenue. The following items are specific to SaaS and recurring revenue businesses, and they are the most common sources of close delays and reporting errors.

Deferred revenue rollforward

Deferred revenue is the liability you carry for subscription revenue you have billed but not yet recognized. Every month, the rollforward must balance:

Opening deferred revenue + new billings - revenue recognized = closing deferred revenue

This rollforward must tie back to the general ledger. If it does not, either your revenue recognition is incorrect or your billing-to-GL sync has an error. Both of those are meaningful problems that compound over time.

For a complete treatment of how the deferred revenue balance builds, flows, and interacts with your cash position and runway forecasts, see Fiscallion's guide to deferred revenue in SaaS.

At most SaaS companies before Series B, this rollforward is managed in a spreadsheet. That works - until contract modifications, mid-term upgrades, and multi-year deals create enough complexity that the spreadsheet becomes the real accounting system rather than a supporting schedule.

Revenue recognition under ASC 606

Revenue is recognized when it is earned, not when cash is received. For SaaS companies, this is governed by ASC 606 - the FASB standard that replaced legacy software revenue guidance and established a single five-step recognition framework across all industries. For a 12-month subscription billed annually upfront, you recognize 1/12 of the contract value per month. For a 24-month deal with non-standard terms, the recognition schedule needs to follow the actual performance obligation timeline.

KPMG's Revenue for Software and SaaS handbook notes that applying ASC 606 to subscription arrangements is not a one-time exercise - it requires ongoing judgment, especially as contracts are modified, usage-based components are added, or multi-element arrangements evolve. EY's comprehensive ASC 606 guide similarly highlights that the FASB completed its post-implementation review in 2024 and found ongoing interpretation challenges in practice.

For a detailed breakdown of how the five-step model applies to SaaS contracts - including what drives recognition timing and how to reconcile your recognition schedule to your ARR bridge - see Fiscallion's revenue recognition in SaaS guide.

Inconsistent revenue recognition is the most common audit finding at Series B and C companies. It is also the most common source of balance sheet errors that surface during due diligence. Fixing it retroactively is expensive and distracting.

MRR and ARR reconciliation to accounting revenue

Your SaaS metrics (MRR, ARR, NRR) and your GAAP revenue are different numbers, and they should be. The problem is when they diverge without a clear explanation.

During close, reconcile your MRR/ARR metrics to your recognized revenue. The difference should be explainable by annual vs. monthly billing timing, deferred revenue movements, and any non-subscription revenue. If the gap is not clearly explained, it will create confusion in board reporting and become a due diligence question later.

Understanding how bookings, billings, and revenue differ - and how each maps to your close outputs - is the foundation of clean metric-to-accounting reconciliation. The bookings-to-revenue bridge is one of the first things investors and acquirers examine during diligence.

Gross margin by product or customer segment

Close is the right moment to update gross margin by product line, not just in aggregate. If you have multiple pricing tiers, multiple customer segments, or a services component alongside software, your blended gross margin hides the economics of individual revenue streams.

At the Fiscallion level of engagement, we typically find that founders know their blended gross margin but cannot tell you whether their enterprise customers are more or less profitable than SMB customers after factoring in implementation costs, support load, and payment terms. That gap limits pricing decisions and capital allocation precision.

A day-by-day close calendar for scaling SaaS companies

Here is a practical close calendar structured for a SaaS company with one finance lead or a fractional finance function. Adjust task owners based on whether you have a bookkeeper, controller, or fractional CFO running each layer.

Pre-close week (final week of the month)

- Reconcile bank accounts through day 25

- Review open AR and send collection nudges for overdue invoices

- Confirm all credit card transactions are imported and categorized

- Validate billing system: confirm all new contracts, renewals, upgrades, and cancellations are recorded

- Run a soft trial balance and flag material anomalies

- Communicate close deadline to department heads (expense submission cutoff)

- Lock prior billing periods once transaction completeness is confirmed

Day 1: Transaction completeness and period lock

- Confirm Stripe (or primary payment processor) is fully synced to the GL through month-end

- Reconcile billing system total to GL revenue accounts

- Record last-day transactions: payroll, vendor invoices, bank transactions

- Identify and document any transactions requiring judgment (disputed charges, intercompany flows)

- Lock the accounting period for all but controller-approved adjustments

Day 2: Revenue recognition and deferred revenue

- Calculate and post monthly subscription revenue recognition

- Complete the deferred revenue rollforward and tie it back to the GL

- Post accrued revenue for services delivered but not yet billed

- Review revenue cutoff: confirm no December revenue is sitting in January (or prior period)

- Identify and resolve any billing-to-recognition mismatches

Day 3: Accruals, prepaids, and balance sheet schedules

- Post all cost accruals: payroll accrual (if not already), contractor costs, software subscriptions billed but not yet invoiced

- Update prepaid expense schedule and post amortization entries

- Reverse prior-month accruals that have been replaced by actual invoices

- Update fixed asset and depreciation schedules

- Reconcile AP aging and AR aging to GL balances

Day 4: Trial balance lock and variance analysis

- Run full trial balance - confirm it balances

- Lock trial balance (controller sign-off required for any further adjustments)

- Produce preliminary P&L and balance sheet

- Run variance analysis: actuals vs. budget and vs. prior month

- Flag material variances (typically >5% or >$10K, whichever is relevant at your scale) for management commentary

Day 5: Final review and package delivery

- Finance lead or fractional CFO reviews full financials

- Finalize management commentary with variance explanations

- Confirm all supporting schedules are filed and audit-ready

- Deliver leadership reporting package: P&L, balance sheet, cash flow, KPI summary, variance narrative

- Update rolling forecast with actual inputs from the closed period

The six most common close failures - and how to replace them

Failure 1: Treating month-end close as a month-end task

The mistake: All close work starts on day 1 of the new month. Reconciliations, transaction review, and accrual estimation happen under pressure.

The replacement: Move all continuity work to the pre-close week. Reconcile bank accounts weekly. Review AP aging bi-weekly. Confirm billing platform completeness before the month ends.

Why it matters: 60-70% of close work is predictable and recurring. None of it needs to wait for the month to end. Consero's 2025 Finance Leaders Survey found that companies redesigning their close calendar - shifting work earlier and decoupling revenue recognition from invoicing - were able to cut close timelines by 70% without sacrificing accuracy.

Failure 2: No named owner for each close task

The mistake: The close "belongs" to the bookkeeper or controller. No one else knows what is supposed to happen or when.

The replacement: Document a close calendar with named owners for every task. Not a department - a person. Include a backup owner for every critical task. Review the calendar in a 15-minute standup on day 1 of the close.

Why it matters: When a bottleneck appears - an unanswered vendor invoice, a late expense submission, a system sync failure - there is no ambiguity about who resolves it and by when. CFO.com reported that cross-functional dependencies and unclear ownership are among the top reasons teams consistently miss close targets.

Failure 3: Revenue recognition managed in a standalone spreadsheet

The mistake: The deferred revenue rollforward and monthly recognition schedule live in an Excel file that only one person understands. When that person is out, the close stalls.

The replacement: Move revenue recognition into your accounting platform or a purpose-built revenue recognition tool. Ensure the rollforward is structured so that any competent finance team member can run it and validate it independently.

Why it matters: Spreadsheet-dependent revenue recognition is the single most common source of restatements and audit findings at growth-stage SaaS companies. PwC's Revenue from Contracts with Customers guide underscores that the judgment and estimation demands of ASC 606 require documented policies and repeatable processes - not ad-hoc spreadsheet logic. It is also the most common bottleneck that adds 2-3 days to a close timeline.

Failure 4: Producing a P&L without a supported balance sheet

The mistake: The close is declared "done" when the income statement is finalized. Balance sheet reconciliations are incomplete or deferred.

The replacement: Treat the balance sheet as the primary close artifact. The P&L is a derivative of balance sheet activity. If the balance sheet accounts are not reconciled, the P&L cannot be trusted.

Why it matters: Investors and acquirers examine balance sheet integrity during due diligence. Consero's research on audit readiness for SaaS companies found that unaudited deferred revenue schedules alone can trigger seven-figure working capital adjustments at close - reducing purchase price in ways that proactive balance sheet discipline would have prevented. Companies that have been declaring a close without balance sheet support routinely face restatements and extended diligence timelines.

Failure 5: No variance narrative in the reporting package

The mistake: The leadership reporting package contains financials but no explanation. The CEO reviews numbers and asks questions. The finance lead answers them in a Slack thread over the next three days.

The replacement: The day-5 package includes a written variance narrative: what was different from budget or prior month, why it was different, and what the business should watch next month as a result.

Why it matters: Variance explanation is where accounting becomes decision support. Without it, the close produces reporting that describes history but does not inform the next decision. This is a structural problem, not a communication problem - and it is one of the core reasons Fiscallion's financial planning and analysis work is structured around decision-grade reporting rather than just metric delivery.

Failure 6: Confusing cash movement with revenue recognition

The mistake: The team looks at the bank balance or Stripe dashboard to understand revenue performance. Cash in is treated as revenue earned.

The replacement: Build a clear separation between cash received (a balance sheet event) and revenue recognized (an income statement event). Include a cash-to-revenue bridge in the monthly reporting package showing how new billings, deferred revenue changes, and cash collections relate to recognized revenue.

Why it matters: Annual contracts billed upfront create a significant timing difference between cash and revenue. Misunderstanding this difference leads to overstated revenue perceptions in good months and confusion about why reported revenue is "low" in months where cash collection was strong but new bookings were flat. The deferred revenue in SaaS guide covers how to model the cash-to-revenue timing gap in your three-statement model and use it to build more accurate runway forecasts.

What a decision-ready close looks like in practice

A decision-ready close does not end when the books are locked. It ends when the leadership team has the numbers, the context, and the trade-off framing to make the next round of decisions confidently.

That means the post-close package answers the following questions, not just the historical ones:

This is the gap between a close that produces reporting and a close that drives decisions. The difference is not financial sophistication. It is framing.

At Fiscallion, the close process is designed to produce this output - not as a separate deliverable that finance creates for leadership, but as the natural output of a close structured around decisions from the start.

Close-readiness checklist for founders and finance leads

Use this to assess where your current close process stands. A "no" on any of these is a close risk.

Workflow and ownership

- Every close task has a named owner and a named backup

- A close calendar exists and is shared with all relevant departments

- Expense submission deadlines are communicated and enforced

Systems and data

- Your billing platform syncs to your accounting platform automatically (no manual exports)

- Bank feeds are connected and reconciled weekly, not monthly

- Your chart of accounts is stable - no ongoing restructuring during an active close

Revenue recognition

- Deferred revenue rollforward is documented and repeatable without the single person who built it

- Revenue recognition policy is written down and applied consistently under ASC 606

- MRR/ARR metrics reconcile to GAAP recognized revenue with a clear bridge

Balance sheet

- All balance sheet accounts are reconciled at close, not just reviewed

- Accruals are posted and reversed on a documented schedule

- Supporting schedules exist for prepaids, fixed assets, accrued expenses, and equity activity

Reporting output

- The close produces a variance narrative, not just financials

- The leadership reporting package is delivered by business day 7 or earlier

- The rolling forecast is updated with actual inputs within 48 hours of close completion

The 5-day close blueprint

A slow financial close is not evidence that your company is growing too fast for finance to keep up. It is evidence that the close has not been designed as a workflow.

The sequencing is what matters. Pre-close work, named ownership, a supported balance sheet, and a variance narrative that frames decisions - those four elements are what separate a close that produces useful reporting from one that produces stress and stale numbers.

At $5M-$50M ARR, you do not need a full-time CFO to run a clean, decision-ready close. You need a structured process, clear ownership, and CFO-level judgment applied to what the numbers mean after they are produced.

If your close is consistently late, your balance sheet is unsupported, or your monthly reporting answers historical questions but not forward-looking ones - those are solvable problems. Fiscallion works with SaaS founders at Series A through Series C to build close processes that are audit-ready, decision-grade, and sustainable without a large finance team. Book a working session to audit your current close process and identify the highest-leverage fixes.