Most founders can tell you their net burn number. Far fewer can tell you which assumption is most likely to make it wrong next quarter - or what the number actually implies for their next hiring decision.

Net burn rate is not a reporting metric. It is a decision input. The moment it sits in a deck without an owner, a trend, and a modeled implication, it stops doing its job.

This guide covers the full picture: precise definition, the correct formula, common calculation errors, how to read movements in the number over time, and the exact actions that should follow each reading.

Key takeaways

- Net burn rate measures actual monthly cash consumed after revenue - not total spending. Using gross burn as a proxy overstates your problem and understates your revenue leverage.

- The number alone is not enough. Net burn only becomes decision-grade when paired with a runway calculation, a burn multiple, and trend direction over at least three months.

- Assumptions need owners. The most common reason net burn forecasts fail is not bad math - it is unowned inputs: headcount plans nobody confirmed, revenue projections nobody stress-tested, and COGS estimates that haven't been updated since the last raise.

Net burn rate is not what you spend - it is what you actually lose

Net burn rate is the amount of cash your company loses in a given month after accounting for all revenue collected. It is the real rate at which your bank balance is shrinking.

Formula:

Net burn rate = Total monthly cash outflows - Total monthly cash inflows (revenue)

Or equivalently, using your bank statements:

Net burn rate = Beginning cash balance - Ending cash balance

The second formula is the more reliable one because it captures timing - late payments, prepaid annual contracts hitting your account, delayed vendor invoices. If you're calculating from an income statement, you can miss these.

Here is how the two types of burn compare:

A company with $400K gross burn and $350K in monthly revenue has a $50K net burn - manageable. A company with $400K gross burn and $80K in revenue has $320K net burn - a different company entirely. Same cost base, entirely different situation. Presenting gross burn where net burn is expected creates a 2-4 month gap in your runway headline that nobody usually flags until an investor asks.

How to calculate net burn rate correctly

Step 1: Use cash basis, not accrual

Net burn is a cash metric. If your books are on accrual, your P&L will show revenue recognized before it's collected and expenses recorded before they're paid. Neither reflects your actual bank balance movement.

Use your bank statements or your cash flow statement - specifically cash from operating activities - not your income statement.

Step 2: Include all cash outflows

Gross burn should capture everything that leaves the account:

- Payroll and benefits (typically 60-75% of burn for SaaS companies at $5-50M ARR)

- Rent and facilities

- Cloud infrastructure and software subscriptions

- Marketing spend (paid channels, content, events)

- Contractors and agencies

- Debt service, if applicable

- Any one-time cash items (legal fees, severance, equipment)

As Aleksandar Stojanovic, CEO & Founder at Fiscallion, notes, "The problem when cloud or API costs scale faster than the associated MRR is that infrastructure is a variable cost that behaves like it's fixed until it suddenly doesn't — and if you react by freezing the roadmap, you damage the growth that's supposed to justify the spend. The right response is to model it, not freeze it, by turning infrastructure cost into a unit metric rather than a lump sum."

One-time items deserve a separate line. When you present burn to a board, label what is recurring versus non-recurring. Investors will ask. If you haven't already done it, you'll recalculate live - which is the wrong time to find a discrepancy.

Step 3: Use a rolling three-month average, not a single month

A single month of burn is noisy. One large severance payment, a semi-annual software contract, or a commission payout from a big Q4 close will distort the number.

Use the three-month rolling average for reporting and runway calculations:

Rolling net burn = Sum of net burn over 3 months / 3

Then run your runway off that:

Runway (months) = Current cash balance / Rolling 3-month average net burn

Worked example

A SaaS company at $8M ARR has the following in month:

- Gross cash outflows: $620,000

- Monthly cash revenue (collected): $280,000

- Net burn rate: $340,000

With $5.1M in the bank:

Runway = $5,100,000 / $340,000 = 15 months

If revenue grows to $320,000 next month with the same cost base, net burn drops to $300,000 and runway extends to 17 months - without cutting a single dollar of spend. That is why revenue trajectory belongs in every burn conversation. For a complete walkthrough of how to build the runway model correctly - including dynamic projections rather than static assumptions - the startup runway calculation guide covers the full methodology.

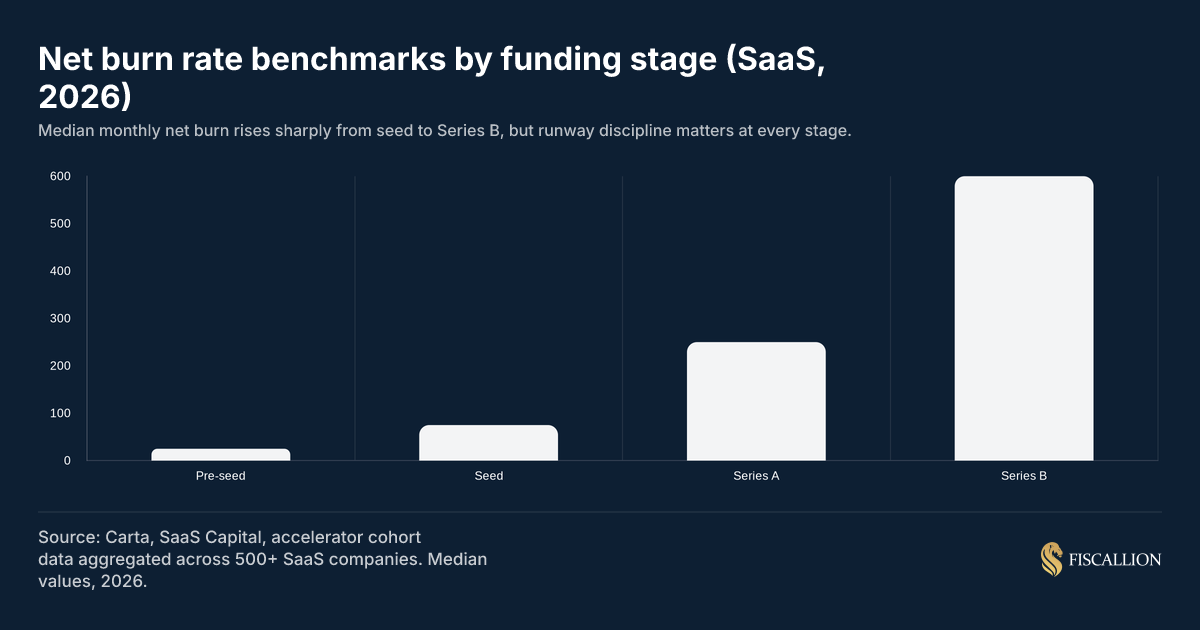

Net burn rate benchmarks by funding stage

Net burn does not have a universal "right" number. The relevant question is whether your burn rate is appropriate given your stage, growth rate, and capital position.

Here are reasonable reference ranges for SaaS companies in 2026:

For companies in the $5-50M ARR range, the relevant frame is not just absolute burn but burn relative to new ARR being added. That ratio is the burn multiple.

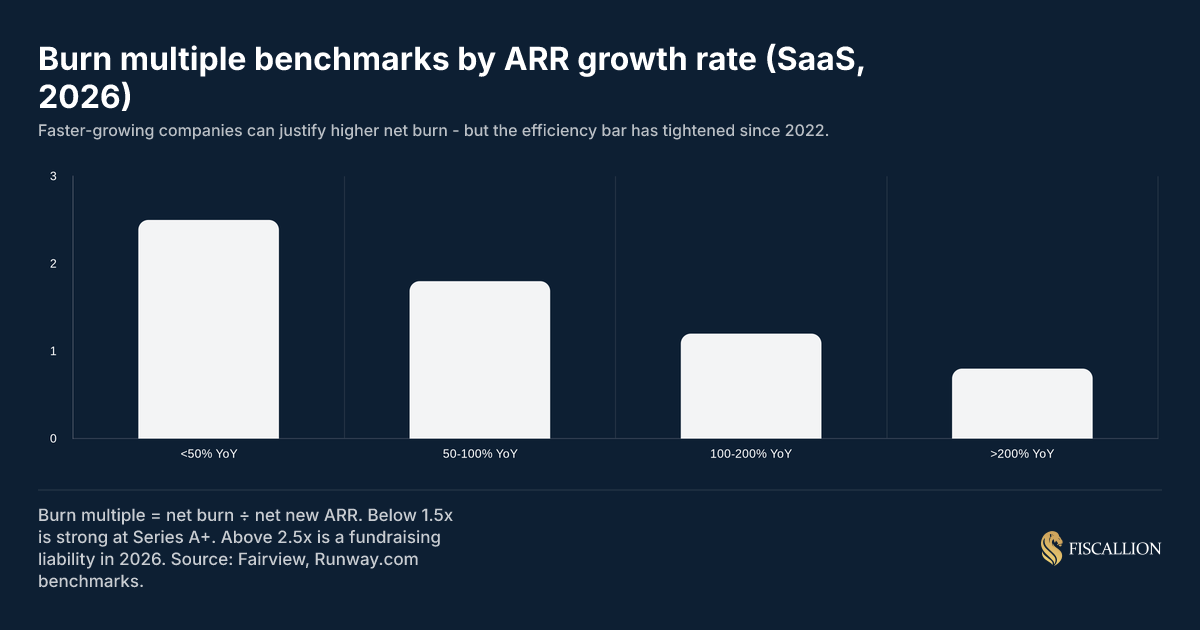

The burn multiple: net burn's most useful companion metric

The burn multiple was coined by David Sacks of Craft Ventures and is simple:

Burn multiple = Net burn / Net new ARR

It answers a question the raw burn number cannot: are you spending efficiently relative to the growth you're generating?

A Series A company adding $80K in net new ARR per month while burning $300K per month has a burn multiple of 3.75x. That is a serious efficiency problem regardless of how clean the burn number itself looks in isolation.

Reference ranges for burn multiple in 2026:

One important caveat: these benchmarks reflect 2026 market conditions. Investor expectations around burn efficiency have tightened materially since 2021-2022. A burn multiple that would have been described as "aggressive growth investment" in 2021 is now more likely described as "capital inefficiency" in a Series B process.

According to Scale Venture Partners' benchmarking analysis, burn multiples are size-dependent: companies in the $0-$1M ARR band average a burn multiple of 3.4x, while companies at $25-50M ARR average 1.4x. This is the natural improvement trajectory as fixed costs get leveraged against a growing revenue base - but it only holds if revenue is actually scaling.

How to read movements in your net burn rate

The direction of net burn over time matters as much as the level. Here is how to interpret each pattern:

Net burn rising with ARR growing faster than burn. This is the healthy pattern for a company investing ahead of revenue. Burn multiple is compressing. Acceptable if runway stays above 12 months.

Net burn rising while ARR growth is flat or decelerating. This is the warning signal most often missed until it becomes a crisis. The cost base is growing but revenue velocity is not keeping up. Burn multiple is expanding. This requires a direct conversation about which cost drivers are responsible and which can be slowed within 60-90 days.

Net burn flat month over month. Usually a sign that hiring has paused and growth investment is steady. Acceptable in the short term. Concerning if the business is supposed to be in a growth phase and revenue is not accelerating despite stable costs.

Net burn falling. Could mean revenue is growing (positive), cost cuts were implemented (context-dependent), or growth investment slowed materially (worth understanding why). Do not assume declining burn is always good - sometimes it means the company has stopped investing.

This last pattern showed up clearly in market-level data: Standard Metrics' Q4 2024 Startup Benchmarking Report found that median quarterly net burn for late-stage startups ($100M+ annualized revenue) had dropped dramatically from $10.6M in Q1 2022 to near cash-flow-positive levels by Q4 2024. The drop was driven by deliberate cost discipline, not revenue growth alone - which is why trend direction and what's driving it are both necessary context.

Five actions that should follow every burn review

Every monthly burn review should produce at least one concrete decision, not just an updated number. Here is the action sequence ordered by impact:

1. Confirm the runway number and who owns the revenue inputs.

Runway is only as reliable as the revenue forecast feeding it. Someone should be named as the owner of the MRR growth assumptions. If that person is not in the room when runway is discussed, the number is unreliable.

2. Stress-test at 70% of projected revenue growth.

Run the runway calculation assuming new ARR comes in at 70% of plan. If runway drops below 10 months under that scenario, that is a capital planning signal - not a worst case to dismiss.

3. Identify which cost drivers are within a 30-90 day control window.

Payroll is almost never adjustable within 30 days without significant disruption. Software subscriptions, contractor spend, and paid marketing often are. Knowing which levers are actually available is different from knowing the aggregate burn number.

While optimizing software subscriptions or tools is a standard lever for managing short-term spend, founders must be careful not to sacrifice structural agility for immediate optical improvements.

4. Map the next hiring decision against its burn multiple impact.

Before approving a new hire, model the incremental burn and the expected ARR contribution. A $180K fully-loaded sales hire who takes 6 months to ramp contributes roughly $90K to burn before generating a dollar of new ARR. That is not an argument against hiring - it is the information you need to sequence hires against runway.

5. Bring the burn multiple to your next board meeting, not just burn.

A board presentation that shows $340K net burn without the burn multiple and the revenue trend next to it is half a slide. Frame it as: here is what we are burning, here is what we are adding, here is the efficiency ratio, and here is what changes it over the next two quarters.

Fiscallion's framework for assumptions ownership

One of the first things we identify when building a cash flow model with a client is which assumptions have no owner. Those are the ones that will be wrong.

Net burn forecasts fail for predictable reasons:

- Headcount plans built in a spreadsheet that nobody in HR has confirmed

- Revenue projections from a pipeline model nobody stress-tested against conversion rates

- COGS estimates from the last raise that haven't been updated since infrastructure scaled

- Payroll assumptions that treat next year's team size as equal to today's

The fix is not a better model. It is assigning an owner to each material input line and setting a review cadence. Monthly for fast-moving assumptions (pipeline, paid marketing), quarterly for slower-moving ones (headcount, infrastructure costs).

This is exactly the kind of structural problem that looks like a reporting gap but is actually a decision-quality gap. Most companies at $5-50M ARR do not have a CFO problem. They have an FP&A problem - unowned assumptions, no formal review cadence, and burn numbers that can't be tied to a decision. For more on how this connects to the broader cash flow discipline, the cash flow forecasting guide for startups covers the full model structure, including how to connect burn rate assumptions to a dynamic runway forecast.

Common mistakes and what to do instead

Mistake 1: Reporting gross burn to a board that expects net burn

This is more common than it should be. If you're reporting gross burn basis to a board that assumes net burn, you will have a 2-4 month gap in your runway headline. No one will say so in the room. An investor will ask about it during diligence.

Replace with: Label every burn number explicitly - "gross" or "net" - in every deck and every model. Do not assume the audience is tracking the distinction.

Mistake 2: Using a single month of burn instead of a rolling average

One expensive month - a large legal bill, a conference, a severance payment - will make runway look shorter than it is. One light month has the opposite effect.

Replace with: Always report the 3-month rolling average for runway calculations. Show the trailing 6-month trend so movements have context.

Mistake 3: Counting revenue as ARR when calculating net burn

ARR is an annualized metric. Net burn is a cash metric. If you're using ARR/12 as your monthly revenue in the burn calculation, you will be wrong whenever there are payment timing differences - annual contracts paid upfront, quarterly billing cycles, delayed collections.

Replace with: Use actual cash received in the month, pulled from your bank statement or cash flow from operations. For annual contracts paid upfront, recognize the cash at the time it lands in the account for burn purposes.

Mistake 4: Running a flat burn assumption in your runway model

A static burn rate assumption - "we'll burn $300K per month for the next 18 months" - is almost never accurate because it ignores planned hiring, seasonal marketing spend, and revenue scaling effects.

Replace with: Build a month-by-month burn projection with the specific hiring plan and revenue ramp baked in. Your runway calculation should reflect what you plan to spend, not what you spent last month. The startup runway calculation guide covers this in detail.

Mistake 5: Treating net burn as a standalone number rather than a system

Net burn means almost nothing without runway, burn multiple, and trend direction alongside it. Presenting $300K net burn is not useful context. Presenting "$300K net burn, 18-month runway, 1.8x burn multiple, trending down as revenue scales" is decision-grade information.

Replace with: Build a three-number burn dashboard - net burn, runway, burn multiple - updated monthly. Add a fourth column for the trend direction over the trailing three months.

Burn review checklist: use this in your next monthly close

Copy this into your close checklist and assign an owner to each line.

Calculation checks (finance lead)

- Net burn calculated from cash basis, not accrual P&L

- All outflows captured including one-time items, labeled as such

- 3-month rolling average calculated and used for runway

- Revenue input cross-checked against bank receipts, not invoiced amount

Interpretation checks (CEO or CFO)

- Runway updated: current cash / rolling net burn

- Burn multiple calculated: net burn / net new ARR

- Trend annotated: is net burn rising, falling, or flat versus last month and 3 months ago?

- Stress scenario run at 70% revenue plan

Decision checks (leadership team)

- Any pending hires modeled against their burn impact and ramp period

- Next board meeting burn slide includes burn multiple and trend, not just the number

- If runway is below 12 months: fundraising or revenue acceleration options tabled for discussion

- Revenue assumption owner confirmed and signed off on the MRR inputs

Turning cash metrics into capital allocation signals

Net burn rate is one of the most cited numbers in SaaS finance and one of the most frequently misused. Reported without context, it tells you little. Reported without a calculation methodology, it is often wrong. Reported without an owner on the revenue inputs, it will be wrong in the direction you least expect.

The decision-grade version of net burn includes the number itself, the 3-month trend, the runway it implies, and the burn multiple that puts it in context against your ARR growth. That four-number view is what turns a monthly close metric into a capital allocation signal.

If your burn number lives in a deck but hasn't driven a hiring decision, a fundraising timing call, or a cost sequencing conversation in the last quarter, the problem isn't the number. It is the framework around it.

Audit your burn rate model and assumptions ownership. If you want a structured review of how your current burn calculation, runway model, and board reporting hold up, book a working session with Fiscallion - we'll identify where the gaps are and build the model to fix them.