Key takeaways

- The cash-to-accrual switch changes how every core metric looks: revenue, burn, margin, runway. Founders who don't re-baseline will make decisions on numbers that reflect accounting noise, not business performance.

- Revenue breaks first. A $24K annual contract that showed as $24K on day one under cash basis becomes $2K/month under accrual. Without a deferred revenue rollforward, the P&L looks like a revenue problem.

- Three reference points at cutover prevent the transition from degrading decision quality: a clean opening balance sheet, an MRR-to-revenue bridge, and a 60-day parallel read.

- If your metrics are shifting underneath you during or after a transition, book a working session to build the re-baselining framework before the next board meeting.

A $24K annual contract hits the books as $24K on day one under cash basis. Under accrual, that same contract becomes $2K per month across twelve periods. The P&L drops. The bank account hasn't changed. And hiring decisions stall while everyone tries to figure out whether the numbers are right.

Nothing is wrong with the numbers. But without a framework that explains the divergence between cash collected and revenue recognized, every metric downstream of revenue becomes a question instead of an answer. Margin shifts. Runway looks different. The board sees a company that appears to be regressing when it may be approaching breakeven.

This pattern shows up consistently in SaaS companies between $5M and $50M ARR making the cash-to-accrual switch. The transition itself is straightforward. What breaks is the founder's confidence in the numbers during the 60 to 90 days when the old view is going away and the new one hasn't earned trust yet.

Three reference points, established once at cutover, prevent every downstream decision error: a clean opening balance sheet, a one-page MRR-to-revenue bridge, and a 60-day parallel read.

This guide walks through why each metric breaks during the transition, how the distortion works, and how to build the re-baselining framework that keeps decisions grounded while the accounting method changes underneath you.

Where FP&A Fits: The Operating Layer Between Data and Decisions

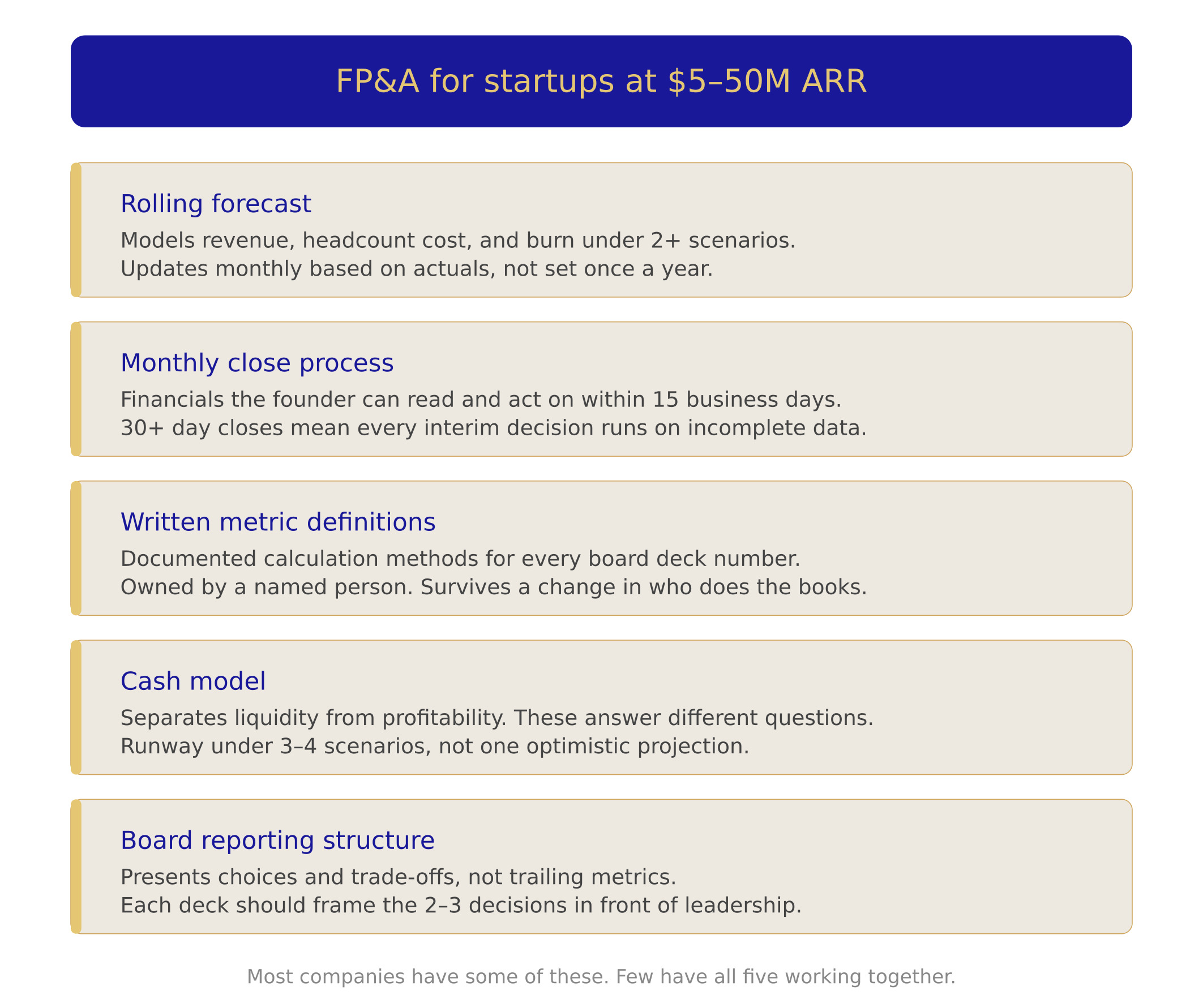

FP&A for startups is the operating layer between raw financial data and the decisions that data is supposed to inform. At companies between $5M and $50M ARR, it covers forecasting, monthly reporting, board packs, metric definitions, and cash management.

Most companies in this range have some of these. Few have all five working together, and the gap shows up as re-explained numbers in board meetings, debated metric definitions mid-quarter, and hiring decisions based on cash in the bank rather than revenue capacity under a defined accounting method.

The cash-to-accrual transition is the moment when that gap becomes impossible to ignore.

Why the Timing Makes the Distortion Expensive

Many SaaS companies in this range are within a few points of breakeven.

A 5 to 10 point margin distortion from the accounting transition, which is a normal and temporary effect, can make a company approaching profitability look like it's regressing. If no one explains the distortion, the board reacts to the wrong signal.

For example, a company at $18M ARR with a 68% gross margin that drops to 61% in the cut period isn't regressing, but recognizing costs correctly for the first time. The board doesn't know that unless someone tells them.

There is also a tax dimension most founders miss.

The IRS requires companies changing accounting methods to file Form 3115 and calculate a Section 481(a) adjustment, a cumulative recalculation of taxable income that may be spread over up to four years. The transition is a ledger change, but it also has formal regulatory requirements.

Revenue Breaks First Because Cash and Recognition Diverge

The first metric to break is revenue: specifically, the relationship between cash collected and revenue recognized.

Consider a $24K annual contract paid upfront. On cash basis, the full $24K hits the books as revenue on the day it lands. On accrual, that same contract becomes $2K per month across twelve periods. The remaining $22K sits on the balance sheet as deferred revenue, a liability, not income.

Here is what that looks like in the first three months:

The P&L under accrual shows $2,000 in Month 1. The bank account shows $24,000. The founder sees lower revenue than the cash position, and the first instinct is that something is wrong with the books. It isn’t, but without a deferred revenue rollforward showing exactly where the rest of that contract lives on the balance sheet, it can be hard to see that.

The faster the company is growing, the wider this gap gets. Each month, more cash comes in than gets recognized as revenue, and the deferred revenue balance on the balance sheet grows. Without a rollforward document tracking that balance, the P&L consistently understates how the business is actually performing.

The fix is not complicated, but it is specific. You need a deferred revenue rollforward that shows where every dollar of collected cash sits: how much has been recognized, how much remains deferred, and how the balance is moving month over month. This is the document that makes the P&L legible again.

If your CAC payback period calculation relies on revenue per customer, the same distortion affects that metric too. Any metric that takes revenue as an input will shift during the transition, and each one needs to be re-examined against the new recognition pattern.

Gross Margin Breaks Second, and the Distortion Is Structural

Revenue is not the only thing that changes timing. Costs shift simultaneously.

Prepaid vendor contracts that were expensed in full on cash basis now get spread across the service period. Annual SaaS tool subscriptions get amortized monthly. And sales commissions, which most cash-basis companies expense when paid, must now be capitalized and amortized over the expected customer life under ASC 606.

That last point is significant. KPMG’s 2025 Handbook confirms that incremental costs to obtain a customer contract, including sales commissions and associated fringe benefits like 401(k) match and payroll taxes, must be capitalized as contract cost assets if the expected amortization period exceeds 12 months. This requirement, which KPMG notes is “new to most software entities,” moves a meaningful cost line from the income statement to the balance sheet.

The effect: gross margin in the cut period can swing 5–10 points for reasons that have nothing to do with how the business is actually performing. Revenue recognition is spreading cash collections over time. Cost recognition is capitalizing and amortizing expenses that used to be recognized immediately. Both changes are happening at once, and the net effect on margin is unpredictable without understanding the mechanics.

Here is the decision that matters: if you adjust spend or headcount based on margin numbers in the first 60 days post-cutover, you are reacting to accounting noise.

Many companies are within a few points of breakeven. A temporary margin distortion during the transition can make a company that’s actually approaching profitability look like it’s moving backward.

That is a costly misread if it triggers a hiring freeze or a budget cut that the underlying business didn’t warrant.

Annotate anything cutover-related. Wait for three months of clean accrual data before making spend or headcount adjustments based on margin.

The distortion is real, temporary, and structural. You don’t have to act on it immediately. If you have a clear non-accounting explanation for a margin shift, act on it. The rule prevents reacting to noise, not reacting at all.

Three Reference Points at Cutover Prevent Every Downstream Decision Error

The mechanics of the transition are manageable. What makes or breaks the switch is whether the founder and the finance team have a shared reference frame during the 60–90 days when the old view is going away and the new one hasn’t earned trust yet.

Three reference points, established once at cutover and maintained each month, prevent the transition from degrading decision quality.

Reference Point 1: Clean Opening Balance Sheet

This is the single most important document in the transition and the one most teams skip.

The clean opening balance sheet is the starting point that both the cash-basis history and the new accrual ledger agree on. It establishes the deferred revenue balance, the prepaid expense balances, the accrued liabilities, and the opening equity position under the new method.

Without it, there is no shared foundation for reconciliation. Every question about “why does this number look different?” traces back to a missing or disputed opening balance sheet.

Build it at cutover. Have the founder and the bookkeeper or controller or fractional CFO sign off on it together. Do not proceed until both sides agree on the opening numbers.

Reference Point 2: One-Page MRR-to-Revenue Bridge

This document shows why recognized revenue differs from cash collected in any given month. It breaks the difference into components:

- Opening deferred revenue balance

- New bookings recognized this period

- Deferred revenue released from prior periods

- Prior-period adjustments

- Closing deferred revenue balance

- Total recognized revenue

Here is the MRR-to-revenue bridge for the $24K annual contract example, assuming the contract is booked in Month 1 with no additional bookings in Months 2 or 3:

In Month 1, the company collects $24K but recognizes only $2K. The remaining $22K sits on the balance sheet as deferred revenue and steps down by $2K each month as the service period progresses. A founder reading only the P&L sees $2K in revenue against a bank deposit of $24K.

The bridge shows exactly where the difference lives. It should take the founder less than five minutes to read and understand the full picture for any given month.

Reference Point 3: 60-Day Parallel Read

For the first 60 days after cutover, run both views side by side: cash and accrual. You need the parallel read so the founder can see the delta, build intuition for it, and develop confidence in the new view before the old one goes away.

The parallel read also serves as a sanity check. If the two views diverge in ways that can’t be explained by the known timing differences (deferred revenue, prepaid expenses, capitalized commissions), something in the setup needs to be investigated before you move forward.

After 60 days, the parallel read ends. The accrual view becomes the single source of truth. The cash-basis view is archived, not maintained.

Stop Comparing After the First Clean Month

After the first full clean month on accrual (typically 30 to 45 days post-cutover, once opening entries have settled and deferred revenue is flowing correctly through the P&L), stop comparing.

Before that point, comparison is useful. It catches setup errors. It helps build intuition for the size of the delta and where it comes from.

After that point, the comparison creates confusion. The two bases are measuring different things. The delta between them is transition noise, not a business signal. Continuing to reference cash-basis numbers alongside accrual numbers does not add information. It adds doubt.

The replacement view is a trailing 3-month accrual view with annotations on anything that looks unusual due to the cutover.

The one number to look at explicitly is the deferred revenue balance on the balance sheet. If it’s growing in line with bookings, the accrual P&L is working correctly, and that single check gives most founders the confidence to stop looking backward. And if the two diverge, investigate.

Five Mistakes Teams Make During Transition (And How to Fix Them)

The same mistakes show up across companies in this range. Each one has a straightforward replacement behavior.

This isn’t a first-year-only problem. Cohen & Company's January 2025 analysis found that even six years after ASC 606 took effect, SaaS companies still grapple with distinguishing implementation services from core subscriptions and determining whether professional services are distinct performance obligations.

Build the Framework Before the Transition Forces You To

The transition takes 60–90 days. The framework you build during it is permanent. Calculate the opening balance sheet. Build the bridge. Track deferred revenue from day one.

Most founders get through the transition. The ones who come out with their decision-making intact are the ones who built the re-baselining framework before or during the switch — not after, once two or three month-end closes have passed with numbers nobody fully trusts.

If you're heading into a cash-to-accrual transition, or you made the switch and your numbers still don't feel right, book a working session with us. We'll build the re-baselining framework for your specific model.