When a month-end close takes three weeks and still contains errors, you don’t have a bandwidth problem—you have a control problem. For SaaS companies scaling between $5M and $50M ARR, informal founder oversight quickly breaks down into fragmented workflows, unauthorized vendor spend, and revenue recognition drift.

Here is the stage-by-stage roadmap to shifting your financial controls from reactive firefighting to proactive governance.

Key takeaways

- Financial controls are governance structures, not accounting tasks. The distinction matters because it determines who owns them and when to build them.

- The four control types - preventive, detective, corrective, and directive - each address a different point in the failure chain. Most early-stage companies only have the first one by accident.

- The 80/20 rule applies directly to control prioritization: roughly 20% of your controls will prevent 80% of your financial risk. Identifying and building those first is the correct sequencing.

- Waiting until Series B to formalize controls is a common trap. Investors at that stage expect controls to already be in place - not on a roadmap.

What this article covers

- The four types of financial controls and what each one actually does

- Why most startups fail due to financial mismanagement (and what the data shows)

- How to apply the 80/20 rule to control prioritization at your stage

- The 5 P's of finance applied to a scaling SaaS context

- A stage-by-stage control-building roadmap from seed through Series C

- Common mistakes and the replacement moves that fix them

- A practical controls checklist you can use immediately

What financial controls actually are (and what they are not)

Financial controls are the policies, processes, approval structures, and system configurations that ensure your financial data is accurate, your cash is protected, and your reporting is reliable enough to make decisions with confidence.

They are not the same as accounting practices. Accounting tells you what happened. Controls determine whether what happened was authorized, accurately recorded, and within the boundaries your organization set.

The clearest way to understand this distinction is to ask: who would catch it if something went wrong? If your answer is "we'd see it in the month-end numbers," you have accounting. If your answer is "the payment requires two approvals and trips a flag above $10,000," you have a control.

The COSO Internal Control — Integrated Framework, the definitive reference standard used by auditors and public company finance teams, defines internal control across five components: control environment, risk assessment, control activities, information and communication, and monitoring. While a SaaS company between $5M and $50M ARR doesn't need to implement all five COSO components in full, fragmented controls remain the single most common root cause of executive-level financial headaches.

Controls are a leadership problem, not a finance team problem

At pre-Series A, the founder typically sees every transaction. That informal oversight acts as a de facto control. Once you cross $5M ARR and the team grows past 15 people, that oversight breaks down. Expenses get approved in Slack threads. Vendors get added without a formal process. Revenue gets recognized at the wrong time because no one owns the ASC 606 policy.

The gap between "founder oversight" and "formal control structure" is where most financial control failures originate. Building that bridge is a leadership decision, not a finance department task.

According to Aleksandar Stojanovic, CEO & Founder at Fiscallion, managing the cultural pushback from early employees during this transition requires reframing the shift entirely. "We're adding these thresholds because we've grown past the point where I can personally see every decision, not because I've stopped trusting you to make them," Stojanovic suggests CEOs tell their teams.

He emphasizes that a formalized approval matrix is actually a shield for the team—protecting employees from being second-guessed on individual judgment calls later—while establishing the exact operational baseline that institutional investors will look for during the next raise.

The four types of financial controls

Every financial control falls into one of four categories. Understanding which type you are building determines when it applies in the failure chain and who owns it.

1. Preventive controls

Preventive controls stop errors and fraud before they occur. They are the most valuable type because they eliminate clean-up cost entirely.

Examples in a SaaS company context:

- Role-based access to your accounting system (only the CFO or controller can post journal entries)

- A purchase order requirement before any vendor can be onboarded

- Hard approval thresholds in your expense system (any spend above $5,000 routes to the CEO or CFO)

- Two-factor authentication on your banking portals

- Segregation of duties between the person who requests a payment and the person who approves it

The design principle: a preventive control should make unauthorized action structurally impossible, not just policy-discouraged.

2. Detective controls

Detective controls catch errors and irregularities after they happen, but before they compound. They are the "second line" when preventive controls are incomplete.

Examples:

- Monthly bank reconciliations that flag any unexplained variance

- Automated spend alerts when a cost category exceeds budget by more than 10%

- Revenue reconciliation between your CRM, billing system, and general ledger

- Expense report audits on a random-sample basis

- Variance analysis on the monthly P&L comparing actual to forecast

The design principle: detective controls need a clear owner, a defined frequency, and a documented escalation path when they surface an issue. A control that finds a problem and goes nowhere is decorative.

3. Corrective controls

Corrective controls address the damage after a problem is detected. They reduce the financial and reputational impact of an error and prevent recurrence.

Examples:

- A documented process for reversing and reposting misclassified journal entries

- A vendor off-boarding checklist that cancels subscriptions and access when a contract ends

- A revenue restatement procedure that defines who reviews, who approves, and how investors are notified

- An accounts payable review that identifies and recovers duplicate payments

The design principle: most early-stage companies have no corrective controls at all. They fix problems ad hoc, which means the same problem recurs and the fix is never institutionalized.

4. Directive controls

Directive controls guide behavior proactively. They set the expectations before someone makes a financial decision, rather than reacting to what they did.

Examples:

- A written expense policy that defines what is reimbursable, at what amounts, and with what documentation

- A financial authority matrix that specifies who can commit spend at what levels without further approval

- A capitalization policy that tells engineers and product managers which costs are to be expensed versus capitalized as intangible assets

- A revenue recognition policy tied to your contract structure

The design principle: directive controls reduce decision ambiguity at the point where the decision is made. The goal is not to restrict people - it is to give them a clear answer before they ask.

Why 90% of startups fail (and what financial controls have to do with it)

The "90% of startups fail" figure is widely cited and mostly misleading in isolation. The more instructive question is: what actually causes the failure?

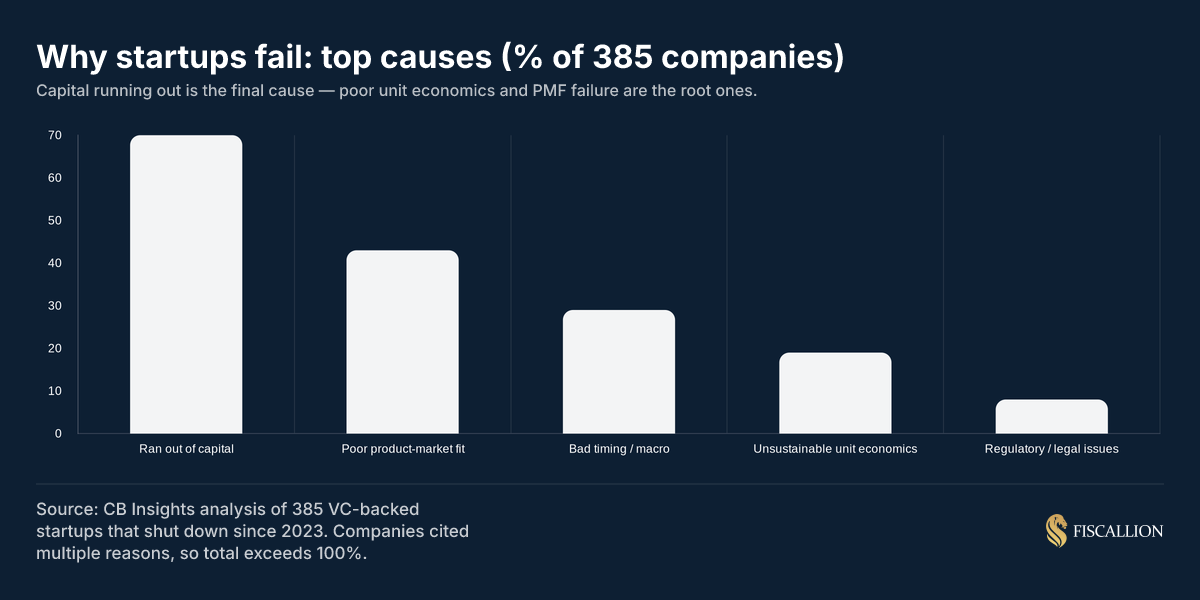

CB Insights analyzed 385 VC-backed companies that shut down since 2023. The data is instructive:

- 70% ran out of capital (the final cause, not the root one)

- 43% cited poor product-market fit

- 29% cited bad timing or macro conditions

- 19% cited unsustainable unit economics

- The median company raised $11M before dying, with a median of 22 months between last fundraise and shutdown

The important pattern: "ran out of capital" is where the story ends. Unsustainable unit economics is where it begins. And unsustainable unit economics is almost always a financial control and visibility problem before it becomes a business model problem.

Here is how that chain works in practice at a scaling SaaS company:

- No one owns the definition of CAC in the model. Sales, marketing, and finance all use different numbers.

- The CAC-to-LTV ratio looks acceptable on the summary slide but the underlying cohort data shows the most recent cohorts are underperforming.

- Hiring decisions are made based on the optimistic CAC assumption, not the cohort-adjusted one.

- Cash depletes faster than the forecast predicted.

- The company raises a bridge at a discount or shuts down.

Financial controls - specifically, having owned assumptions, a defined calculation methodology, and a monthly reconciliation between the model and actuals - break this chain at step one.

The Association of Certified Fraud Examiners' 2024 Report to the Nations found that nearly 33% of fraud can be directly attributed to a lack of internal controls, and that 86% of fraud cases involve asset misappropriation that goes undetected for an average of 14 months. For a company with 18 months of runway, that detection window is existential.

The specific failure modes most common at $5–50M ARR

- Cash flow blindness: No single source of truth across the billing system, bank account, payroll tool, and expense platform. The "cash balance" in the board deck is a snapshot, not a forecast.

- Revenue recognition drift: ARR gets reported from the CRM, but the general ledger uses a different methodology. Investors see the gap during diligence.

- Unapproved spend growth: Vendor spend compounds quietly. SaaS subscriptions auto-renew. Headcount costs expand with informal hires. No one audits the vendor list quarterly.

- No approval matrix: The founder approves everything informally. When they stop doing that (which happens around Series A), there is no documented authority structure to replace it.

The 80/20 rule for startup financial controls

The 80/20 rule - formally the Pareto principle - holds that roughly 20% of inputs drive 80% of outcomes. Applied to financial controls, it means: a small set of well-designed controls will prevent the vast majority of your financial risk.

This matters because founders and small finance teams consistently make one of two mistakes:

- They build too few controls (usually nothing beyond bank access and a basic expense policy).

- They try to build everything at once after a scare, creating bureaucratic overhead that slows the business down without targeting the highest-risk areas.

The 80/20 framing gives you a sequencing principle.

The 20% of controls that prevent 80% of risk

Based on the failure patterns above, here is where to focus first:

These seven controls are not everything. They are the starting point that prevents the most common, most costly failures. Everything else is built on top of this base.

Case Study: The $47,000 offboarding blindspot

A Series B company with 45 employees and $18M ARR discovered during investor due diligence that three former employees still had active software subscriptions billed to the company card - two years after their departure. Total cost: $47,000. That is not a CFO problem. That is an offboarding checklist problem. One control, documented and owned, prevents it entirely.

Even when a founder believes their hands-on approach keeps things airtight, institutional auditors evaluate system architecture rather than personal integrity. Relying on centralized, undocumented authority is one of the fastest ways to stall an upcoming round.

The 5 P's of finance applied to a scaling SaaS context

The 5 P's framework - Planning, Position, Protection, Performance, and Perspective - is typically applied to personal finance. Translated into a SaaS FP&A context at $5–50M ARR, each P maps to a specific control category:

Planning - forecasting controls

Planning means having a financial model that is connected to actual assumptions, owned by someone, and updated on a defined cadence.

The control here is not the model itself - it is the process that governs the model. Who updates it? What triggers a revision? How are new hiring decisions reflected in the runway projection before a headcount request is approved?

At Fiscallion, we see the planning failure most often as: "We have a model, but nobody trusts it because it hasn't been reconciled to actuals in four months." A planning control fixes that by defining a monthly model-to-actuals reconciliation process with a named owner.

Position - balance sheet and cash controls

Position means knowing your current financial state accurately: cash balance, outstanding receivables, deferred revenue, capitalized software costs, outstanding payables.

The control here is a monthly balance sheet review that someone actually does, with documented sign-off. Most early-stage companies produce an income statement and ignore the balance sheet until fundraising prep. That is a mistake. Deferred revenue errors, misclassified liabilities, and understated accruals all live on the balance sheet - and they matter enormously during due diligence.

Protection - preventive and corrective controls

Protection maps directly to the preventive and corrective control categories above. The goal is to ensure that cash and assets are safeguarded against both error and intentional misappropriation.

The specific controls that matter most here at Series A and B stage:

- Dual-approval for ACH transfers above your defined threshold

- A monthly vendor audit against your bank statements and AP ledger

- Password manager and access review for all financial system logins

- A documented process for handling employee terminations (benefits, system access, expense card cancellation)

Performance - reporting controls

Performance means having financial reports that are accurate, timely, and decision-relevant.

The control here is your month-end close process. It should have a defined close calendar (day 1: bank recs; day 3: AR/AP cutoff; day 5: payroll accruals; day 8: management accounts distributed). It should have a named owner for each step. And it should produce a P&L, balance sheet, and cash flow statement that can be shared with the board without manual editing in Excel the night before.

Month-end close taking longer than 10 business days is a control problem, not a bandwidth problem. According to finance operations benchmarks, top-performing SaaS finance teams target a 5-day close — anything beyond 10 days is a signal of missing upstream controls, not headcount.

Perspective - strategic FP&A controls

Perspective means maintaining a view of the business that connects current financial performance to future capital needs and trade-off decisions.

This is where most $5–50M ARR companies have the sharpest gap. The tactical controls are (eventually) built. But the question "what does our current burn rate imply for the raise we need to do in 14 months, given this hiring plan?" rarely gets answered before the board meeting.

The control here is a quarterly capital allocation review: a structured conversation between the founder and the CFO (or fractional CFO) that explicitly maps spend commitments to runway milestones, and surfaces the trade-offs before they become emergencies.

Stage-by-stage control-building roadmap

The right set of controls depends on your stage, team size, and investor profile. Over-engineering controls at seed stage creates friction that slows you down. Under-building them at Series B creates the investor scrutiny problem described earlier.

Pre-seed to seed

Focus: cash protection and basic hygiene.

At this stage, controls are mostly about not creating problems you will have to clean up later.

- Separate business and personal accounts (no exceptions)

- A named person who owns the bank account and reconciles it monthly

- Basic expense policy: what is reimbursable, what requires a receipt, what requires approval

- No equity issued without signed documentation and vesting terms

- All contractors signed on paper before work begins

What you do not need yet: a formal approval matrix, a vendor management system, or a full close calendar. Founder oversight is sufficient if the team is under 10 people and you have less than $2M in cash.

Series A ($5–15M ARR)

Focus: segregation of duties, revenue recognition, and reporting infrastructure.

This is the most important stage to build controls. You are too big for founder oversight to be reliable, and you are about to face institutional investor scrutiny for the first time.

- Define and document your revenue recognition policy aligned to ASC 606 — KPMG's SaaS revenue handbook is a practical reference for how the standard applies to subscription arrangements

- Implement an expense approval matrix with hard thresholds by role

- Add a second approver for all payments above $10,000

- Move from cash-basis to accrual accounting if you have not already

- Build a three-statement model that reconciles to actuals monthly

- Run bank reconciliations on a weekly basis for operating accounts

- Document the month-end close calendar with named owners for each step

- Conduct a quarterly vendor audit

Trigger to add: the first time a new hire approves a payment without founder review, the control infrastructure needs to be in place.

Series B ($15–30M ARR)

Focus: formal governance, department-level budget controls, and audit readiness.

- Formalize the financial authority matrix (documented, signed, distributed to all department heads)

- Implement department-level budget vs. actuals reporting with monthly owner review

- Add a formal variance analysis process: any variance above 10% of budget requires a written explanation

- Engage an external auditor annually (even before it is legally required)

- Implement a formal capitalization policy for software development costs

- Build a rolling 13-week cash flow forecast

- Add an internal controls questionnaire to your annual finance review

At this stage, "we have a control for that" needs to be true and documented, not just verbally asserted. Investors will ask. Acquirers will ask. The answer needs to come with evidence.

Series C ($30–50M ARR)

Focus: audit trail quality, ERP-level system controls, and SOX readiness preparation.

- Evaluate whether you need an ERP upgrade (NetSuite, Sage Intacct) to support the transaction volume and reporting requirements

- Implement formal change management for financial systems (no one modifies the chart of accounts without a documented approval)

- Add an internal audit function or engage an outsourced internal audit firm

- Begin SOX-like documentation for key financial processes even if you are not yet public

- Establish a formal disclosure committee for investor reporting

- Separate the treasury function from accounts payable

Most Series C companies attempting an IPO in 12–24 months will face a comment letter from auditors about controls maturity. EY's analysis of IPO readiness shows that SOX preparation is one of the most common points of delay in the pre-IPO timeline — and that companies starting the process at Series B, rather than at the S-1 filing date, complete it in roughly half the time.

How to build a financial authority matrix

The financial authority matrix (FAM) is the single most underbuilt control at Series A and B companies. It is also one of the highest-leverage items in the 80/20 stack.

A FAM answers one question for every financial commitment your company makes: who is authorized to approve this, and at what dollar amount?

What a basic FAM covers

The thresholds above are illustrative and should be calibrated to your company size. A $20M ARR company might set the CEO approval threshold at $25,000 rather than $10,001. The important thing is that thresholds exist, are documented, and are enforced by your expense system - not just by policy.

The most common FAM gap: multi-year contracts

Founders often set dollar thresholds on one-time or annual spend but overlook multi-year contract commitments. A $12,000/year SaaS contract with a three-year term is a $36,000 commitment. If the policy threshold for CEO approval is $25,000, this contract should require CEO sign-off - but it often goes through as a $12,000/year line item without the full term value disclosed.

Add a rule: any contract with a term longer than 12 months requires approval at the level of the total contract value, not the annual value.

Common mistakes and the replacement moves

Mistake 1: building controls only after a problem

The pattern: an expense gets miscategorized, a vendor overcharges, or an employee makes an unauthorized purchase. The company adds a control in response.

The problem: reactive control-building addresses the last problem, not the next one. You end up with a patchwork of policies that each address a specific incident rather than a coherent control framework.

Replacement move: use the stage-by-stage roadmap above to build controls on a defined cadence, not in response to failures. The trigger should be your revenue milestone, not your last bad experience.

Mistake 2: confusing documentation with the control

The pattern: a policy document exists. It lives in a folder. No one enforces it or reviews it.

A written expense policy is not a control. An expense system that enforces the policy with hard approval routing is a control. The documentation describes the intent. The system or process creates the enforcement.

Replacement move: for every policy document you have, ask: "What would happen if someone violated this right now?" If the answer is "they probably could and we would not notice for a month," you have documentation, not a control.

Mistake 3: assigning control ownership to finance only

Financial controls require input and enforcement from non-finance teams. Department heads need to own their budget variances. HR needs to execute the termination checklist. Legal needs to route contracts to finance before signing.

When finance owns everything, controls become a bottleneck. When cross-functional owners are defined, controls become governance.

Replacement move: for each control in your framework, name a primary owner and a secondary reviewer. The primary owner does not have to be in finance.

Mistake 4: treating the month-end close as a reporting exercise

The month-end close is the point at which all control failures become visible. If your close is late, messy, or requires heroic effort, that is diagnostic information about which upstream controls are missing.

A 15-day close is almost always the symptom of three or four missing controls upstream: no cut-off policy for expense reports, no automated AP accruals, no standard reconciliation format.

Replacement move: run a close postmortem every quarter. Document the three things that caused the most delay. Fix one of them each quarter.

Mistake 5: deferring controls because you plan to hire a CFO

"We'll fix this when we have a full-time CFO" is a reasonable-sounding deferral that usually costs more than the CFO hire itself.

A CFO hired into a company with no controls will spend the first six to nine months building infrastructure that should have existed at Series A. That is not CFO work - it is finance hygiene work. And it means the CFO's strategic capacity is consumed by remediation rather than decision support.

Replacement move: fractional CFO engagement between Series A and Series B to build the control infrastructure before the full-time hire. The full-time CFO then inherits a clean foundation and can focus immediately on capital strategy, board reporting, and the next raise.

The startup financial controls checklist

Use this as a staged implementation guide, not a one-time audit.

Stage 1: Series A baseline (must-have)

- Separate business and personal bank accounts, with named account owner

- Written expense policy distributed to all employees and contractors

- Expense approval routing enforced in your expense management system

- Financial authority matrix documented and distributed to department heads

- Second approval required for all payments above defined threshold

- Monthly bank reconciliation with documented sign-off

- Revenue recognition policy written and aligned to ASC 606

- Accrual-basis accounting (not cash basis)

- Three-statement model reconciled to actuals monthly

- Vendor onboarding and offboarding checklist

- Month-end close calendar with named owner for each step

Stage 2: Series B additions

- Department-level budget vs. actuals with monthly owner review

- Variance analysis: written explanation required for variances above 10% of budget

- Formal capitalization policy for software development costs

- Rolling 13-week cash flow forecast

- Quarterly vendor audit (compare active vendor list to bank statements)

- Annual external audit engagement

- Internal controls documentation as a standalone document

- Quarterly capital allocation review between CEO and CFO

Stage 3: Series C additions

- ERP evaluation against current transaction volume and reporting requirements

- Change management process for financial system modifications

- Internal audit function or outsourced internal audit engagement

- SOX-adjacent documentation for high-risk financial processes

- Formal disclosure committee for investor reporting

- Treasury function separated from accounts payable

Building the foundation for your next raise

Financial controls at a $5–50M ARR company are not about compliance or bureaucracy. They are about having financial data you can actually use to make decisions - about hiring, capital allocation, the next raise, and the trade-offs the board needs to see clearly.

The companies that build controls reactively spend their Series B year cleaning up the infrastructure that should have been in place at Series A. The ones that build proactively arrive at each stage with investor-ready financials, accurate forecasts, and a team that knows exactly who approves what and why.

The 80/20 principle applies directly: start with the seven to ten controls that prevent the most common failure modes. Build the rest on a stage-matched roadmap. Name an owner for every control, not just the output it produces.

If your current close takes longer than 10 days, your revenue recognition is not reconciled between your CRM and your general ledger, or your approval structure lives in your head rather than in a documented policy, those are the three places to start.

Fiscallion works with SaaS founders at Series A through Series C to build the FP&A infrastructure and control environment that makes financial data decision-grade - without hiring a full finance team before you are ready for one. If you want to assess where your current controls stand and what to build next, book a working session with our team.